THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - August 26, 2011

Both the US and the UK will remind the world what modern day Jobless Stagflation looks like this morning. This is not 2008. It’s 2011. The UK printed their Q211 GDP at 0.7% y/y this morning and the US should come in wherever they make up the number (subject to 81% downside revision); headline inflation in both the US and UK will continue to run 5-10x real-GDP growth; markets have paid (and are paying) lower multiples for GDP slowing down hard (stag) and sticky/lagging/higher costs (flation)

As we look at today’s set up for the S&P 500, the range is 75 points or -4.51% downside to 1107 and 1.96% upside to 1182.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1584 (-2757)

- VOLUME: NYSE 1209.19 (+8.99%)

- VIX: 39.76 +10.75% YTD PERFORMANCE: +124.00%

- SPX PUT/CALL RATIO: 1.72 from 1.73 -0.12%

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 32.41

- 3-MONTH T-BILL YIELD: 0.01% -0.01%

- 10-Year: 2.23 from 2.29

- YIELD CURVE: 2.01 from 2.06

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30 a.m.: GDP, QoQ Annualized: est. 1.1%, prior 1.3%

- 8:30 a.m.: Personal consumption, est. 0.2%, prior 0.1%

- 9:55 a.m.: UMich Confidence, Aug. final, est. 55.8, prior 54.9

- 2 p.m.: USDA cattle, hog slaughter

WHAT TO WATCH:

- Bernanke speaks at 10 a.m. in Jackson Hole, Wyoming

- Short-selling bans extended in France, Spain, Italy amid stock volatility

- Japan Prime Minister Naoto Kan’s terms for resignation met with passage of bills

- General Electric (GE); expects Latin America sales to double in next 3 or 4 years

- Goldman Starts Internal Probe on Twitter Leaks: N.Y. Post

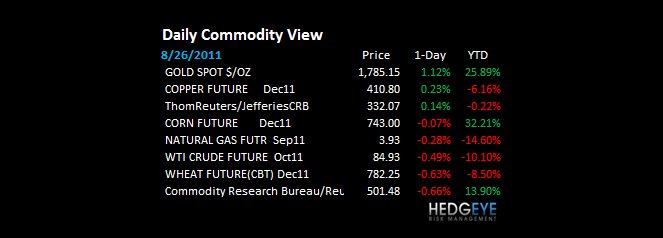

COMMODITY/GROWTH EXPECTATION

- COMMODITIES: Gold holds the Hedgeye TRADE lines of support (1705) like a champ - new trading range is now 1.

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- U.S. Northeast Braces for Worst Hurricane Threat Since 1985

- Glencore, Rio Speed Partner Deals After Stock Declines

- German Nuclear Exit May End French Power Premium: Energy Marke

- Gold Gain Cuts Weekly Drop as Stocks Fall Before Bernanke Speech

- Oil Trims Weekly Gain on Concern of Slower U.S. Economic Growth

- Gold May Slump 30% as Dollar ‘Outperforms,’ Aegis Capital Says

- Crises Send U.S. Wheat Exports to 18-Year High: Chart of the Day

- Copper Trims First Weekly Gain in Four Ahead of Bernanke Speech

- Iron Ore Climbs to Three-Month High as China Boosts Stockpiles

- Societe Generale Hires Haigh as Head of Commodities Research

- Oil May Fall as Libya Rebels Move to Resume Output, Survey Show

CURRENCIES

EUROPEAN MARKETS

- The EUROPEAN train wreck continues!

- Greece is gone!

- GERMANY – Germany leading Europe on the down days now and that’s just not good; down another -1.7% here this morn and crashing (down -27% since May) to lower-lows; there is no catalyst (and it’s probably a bearish one) until mid-late SEP in Europe when 27 political countries arm wrestle on the EFSF

- Germany Jul import prices +7.5% y/y vs consensus +7.0%, priior +6.5%

- UK Q2 GDP +0.7% y/y vs preliminary +0.7%; +0.2% q/q vs preliminary +0.2%

ASIAN MARKETS

- ASIA: very much mixed overnight with China down 12bps, Singapore -0.6%, India -1.4%, KOSPI +0.8% and Thailand +0.87%.

- Japan July core CPI +0.1% y/y vs cons (0.1%). Tokyo August core CPI (0.2%) y/y vs cons (0.1%).

MIDDLE EAST

Howard Penney

Managing Director