THE HEDGEYE BREAKFAST MENU

Notable macro data points, news items, and price action pertaining to the restaurant space.

MACRO

For the week ending August 19, MBA mortgage applications composite index declined 2.4% WoW, driven by a fall in purchase applications. The purchase index fell by 5.7% WoW; the most recent data on new and existing home sales indicates that homebuyer demand remains weak. The refinance index inched down 1.7%.

SUB-SECTOR PERFORMANCE

Yesterday, the QSR space outperformed driven by the high beta coffee stocks and CMG (with the exception of DNKN), which I think is extremely overvalued.

QUICK SERVICE

- The +3.43% move in the S&P yesterday was associated with a positive volume studies of +4%. The only QSR names to move higher on accelerating volume were SBUX, PZZA and DPX.

- Dunkin' Donuts has signed a multi-unit store development agreement with the Robinson Family and Southern Food Services Inc. for four new restaurants in Northern Huntsville, Ala. The first restaurant is slated to open in 2012 and the remainder by 2016.

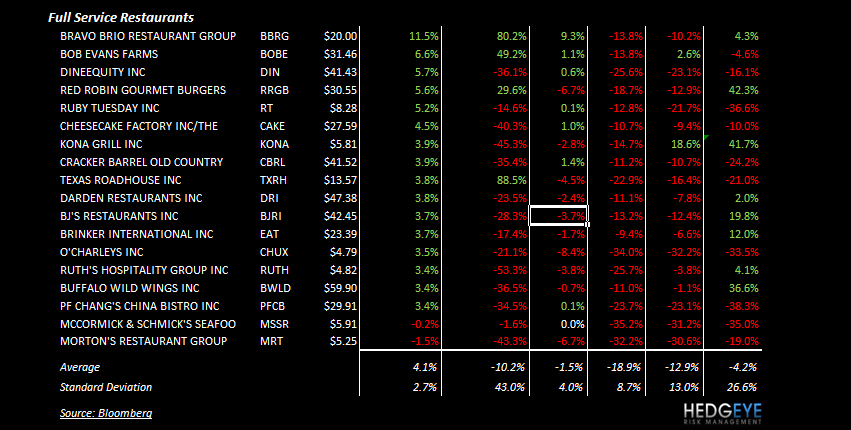

FULL SERVICE

- In the FSR space, the names that moved higher on accelerating volume were BBRG, BOBE, RRGB and TXRH.

Howard Penney

Managing Director

Rory Green

Analyst