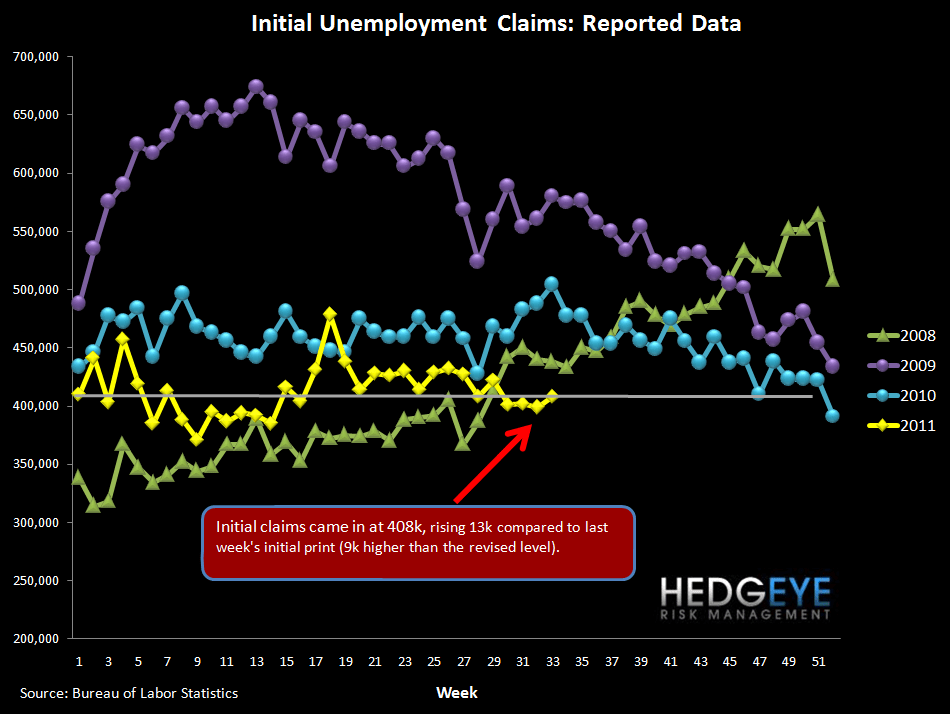

Initial claims climbed 13k from the prior week (9k after the revision to the prior week's print), bringing the headline number back to 408k. Last week, we noted a divergence in the usually-tight correlation between the S&P and initial claims, suggesting that claims would move higher, the S&P would snap back, or some combination. We continue to expect claims to back up further to close this gap. If all the mean reversion comes on the claims side claims will rise to ~475k. This would be reflect/cause a significant slowdown in US economic growth expectations consistent with our Macro team's call.

Challenger Announced Job Cuts rose 60% YoY in July, a leading indicator for initial claims. While still well below 2008-2009 levels, this is a substantial acceleration from recent months.

Margins under Pressure

We track the 2-10 spread as a proxy for bank margins. With the long end of the curve continuing to come down even as the short end is fixed close to zero, margins are under assault. The 2-10 spread of 197 bps compares to an average for the 3Q of 240 bps and an average for 2Q of 264 bps.

The chart below shows performance by subsector. With the market coming up for air in the last week, Title Insurers and Payment Processors have both broken back above positive YTD territory.

Joshua Steiner, CFA

Allison Kaptur