TODAY’S S&P 500 SET-UP - August 17, 2011

A “V-bottom” and low volume follow for 3 days does not a bottom make. Bear market bottoms are processes, not points – and as long as the math in my multi-factor, multi-duration, model says sell, I’ll keep saying sell. The number one question Keith has been getting is “when do you buy.” I think the Pain Trade has shifted to DOWN (as opposed to UP) and until the questions are ‘where do we stop selling’, Growth Slowing and Stagflation won’t be fully priced in. As we look at today’s set up for the S&P 500, the range is 41 points or -1.66% downside to 1173 and 1.78% upside to 1214.

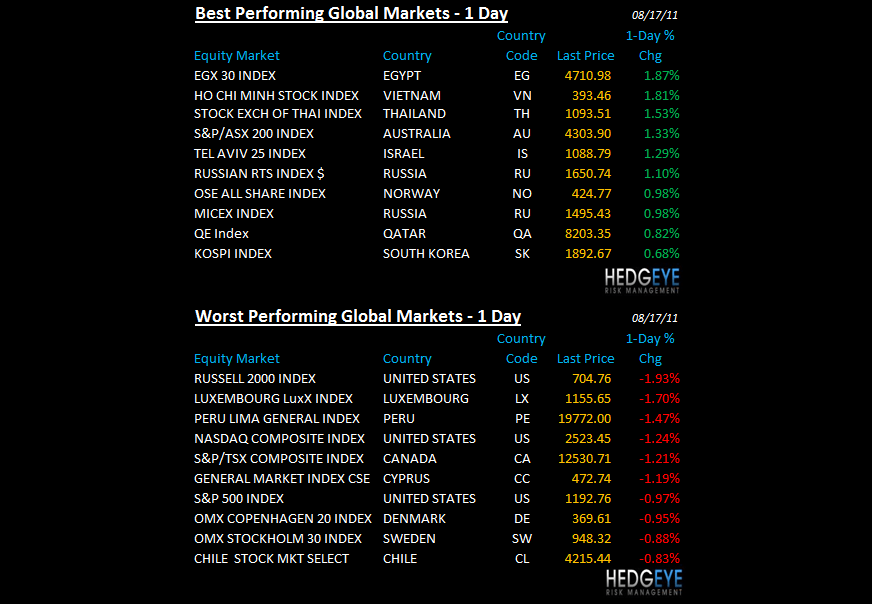

SECTOR AND GLOBAL PERFORMANCE

Yesterday was the 10th consecutive day where all 9 Sectors in the S&P Sector Model flashed bearish on both TRADE and TREND durations. Remember, the S&P500 rallied off oversold lows last week but was still down week-over-week for the 3rd consecutive week. The 3 Sectors that continue to look the most bearish are the ones that fit our Macro Themes of Growth Slowing and Stagflation like a glove:

- Financials (XLF) – led yesterday’s decline (as they have since April) = down -18.9% YTD (we’re short XLF)

- Basic Materials (XLB) – look as bad as Dr. Copper is starting to look = down -10.4% YTD

- Industrials (XLI) – down another -1.4% today; buying cyclicals at a cyclical top has risk = down -9.9% YTD

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1525 (-4073)

- VOLUME: NYSE 1132.58 (+2.46%)

- VIX: 32.85 +3.07% YTD PERFORMANCE: +85.07%

- SPX PUT/CALL RATIO: 1.40 from 2.10 (-33.15%)

CREDIT/ECONOMIC MARKET LOOK:

FIXED INCOME: Yield Spread (UST) continues to compress this morn (10s-2s = 204bps) = explicit signal that US Growth is still slowing.

- TED SPREAD: 27.75

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 2.23 from 2.29

- YIELD CURVE: 2.03 from 2.10

MACRO DATA POINTS (Bloomberg Estimates):

- 7 a.m.: MBA Mortgage Applications

- 8:30 a.m.: Producer Price (MoM), Jul, est. 0.1%; prior -0.4%

- 10:30 a.m.: DoE inventories

- 11:30 a.m.: U.S. to sell $20b 12-day cash mgmt bills

- 1:20 p.m.: Fed’s Fisher (Dallas) speaks in Texas

WHAT TO WATCH:

- Dell said on call last night it saw some consumer demand weakness in June, moving into 3Q; cut year sales forecast. Watch Intel, Seagate, H-P stocks in supply chain

- Merkel, Sarkozy rebuffed calls for joint euro borrowing to end debt crisis, saying greater economic integration needed first

- President Obama continues his bus tour with town halls in Atkinson and Alpha, Illinois

- Vice President Biden in Asia, stops in Beijing first

COMMODITY/GROWTH EXPECTATION

COMMODITIES: Dr. Copper remains broken from a Hedgeye TAIL perspective and we remain long Silver.

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- No Double-Dip Yet With U.S. Economy Punching Up Growth Figures

- Singh Targets China’s 7 Days With $60 Billion: Freight Markets

- Oil Climbs From Two-Day Low as U.S. Gasoline Inventories Decline

- Record LNG Imports by India Signal Rising Prices: Energy Markets

- Barclays’s Todd Edgar Said to Leave After 2 Years to Start Fund

- Gold Gains for Third Day in London as Debt Concerns Spur Demand

- Copper Rises as Chinese Buying Draws Down LME Inventories

- Some Rare Earth Prices Will ’Collapse’ on Oversupply, Miner Says

- Rio Tinto Halts 2 Pilbara Iron Ore Mines After Fatality

- Woodside Profit Beats Analysts’ Estimates on Lower Oil Tax Bill

- ENRC First-Half Profit Rises 29% on Higher Commodity Prices

- Commodity Prices Being Driven by Supply Scarcity, Barclays Says

- Wheat Rises for Third Day as Dryness May Reduce U.S. Seeding

- Peppers Wilt as Barley Drowns for Farmers Who Can’t Tap Tax Aid

- Copper Gains as Stockpiles Decline on China Buying: LME Preview

- Milk-Powder Prices Tumble to 12-Month Low as Demand Ebbs

- Commodity Traders’ $1 Million Bonus as Oil Doubles

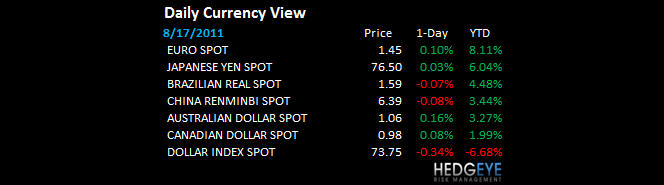

CURRENCIES

EUROPEAN MARKETS

- EUROPE: crashes in European Equities from YTD peaks: Italy -32%, France -28%, Spain -23%, Germany -21%

- UK Jun ILO unemployment rate +7.9% vs consensus 7.7% and prior 7.7%

- UK Jul claimant count unemployment change 37.1k vs consensus 20.0k and prior revised to 31.3k from 24.5k

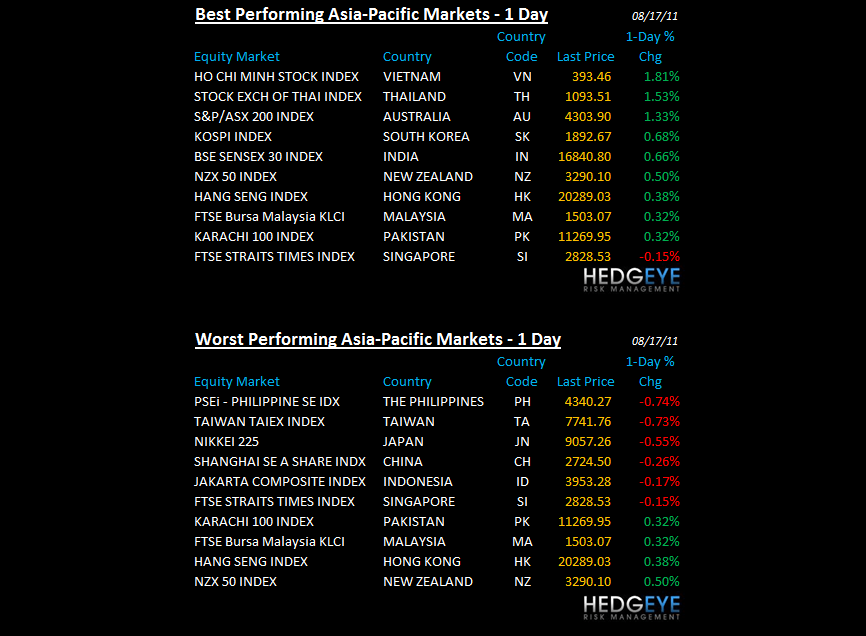

ASIAN MARKETS

- ASIA: could have been worse overnight, but my signals say it will get a lot worse; particularly in Japanese and Korean stocks

MIDDLE EAST

Howard Penney

Managing Director