THE HEDGEYE BREAKFAST MENU

MACRO

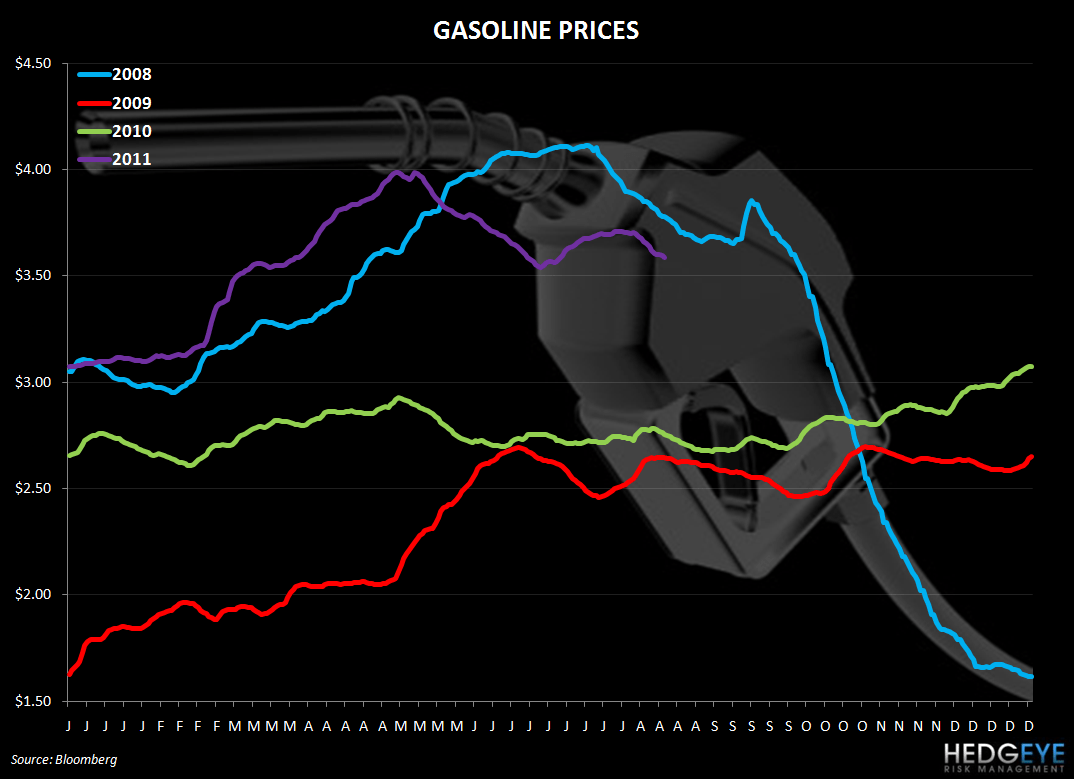

Consumer

The ICSC chain store sales index posted its third straight decline, falling 1.5% in the latest week. Year-over-year growth slowed to 3.5%, its lowest level in six weeks. Its becoming more apparent that the stock market volatility may be impacting consumer behavior more than the potential benefit from lower gasoline prices.

Gasoline prices have slumped in August to-date after gaining 4.4% in July. Concerns surrounding slowing economic growth are likely weighing on oil prices.

Subsectors

We’ve been highlighting the Food Processors group as a beaten-down category that will benefit as commodity inflation becomes less of a headwind. Over the past day and week, the subsector has outperformed other food, beverage, and restaurant peers.

QUICK SERVICE

- SBUX Via ready brew has been expanded to six additional countries, according to a press release out this morning. The product is now available to all Starbucks locations in Asia.

- MCD is rated as more healthful than Subway by its most influential, social-media-connected patrons, according to Nations Restaurant News.

CASUAL DINING

- Bar and Grill led the way yesterday. DIN outperformed, gaining 7.4% on steady volume.

Howard Penney

Managing Director

Rory Green

Analyst