Fed Data Points To An Overall Improved Lending Environment

Yesterday afternoon the quarterly Federal Reserve Senior Loan Officer Survey was released. Across all asset classes banks are now more willing to make loans. This is evident both in the net percentage of banks easing/relaxing standards and in the net percentage of banks increasing/reducing spreads on loans.

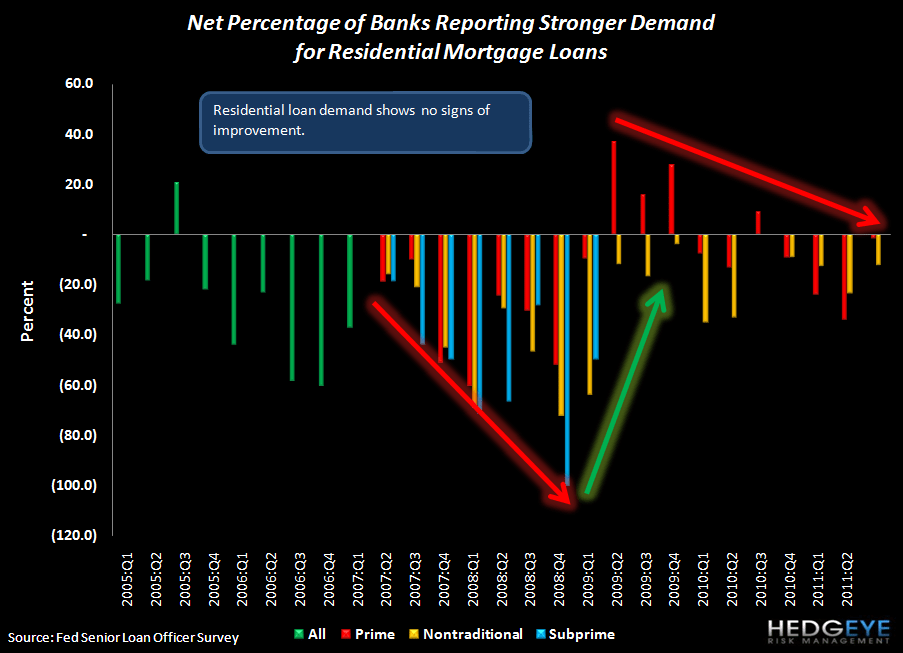

Borrowers are also emerging from the woodwork as demand for all loan types, save one, rose in the most recent survey. The sole exception being residential mortgage, where banks reported that demand fell yet again this quarter. Roughly 75% of the bankers surveyed predicted that 2H11 mortgage origination volume would be flat with volume seen in 1H11. The remaining 25% was split between expecting it to be up or down.

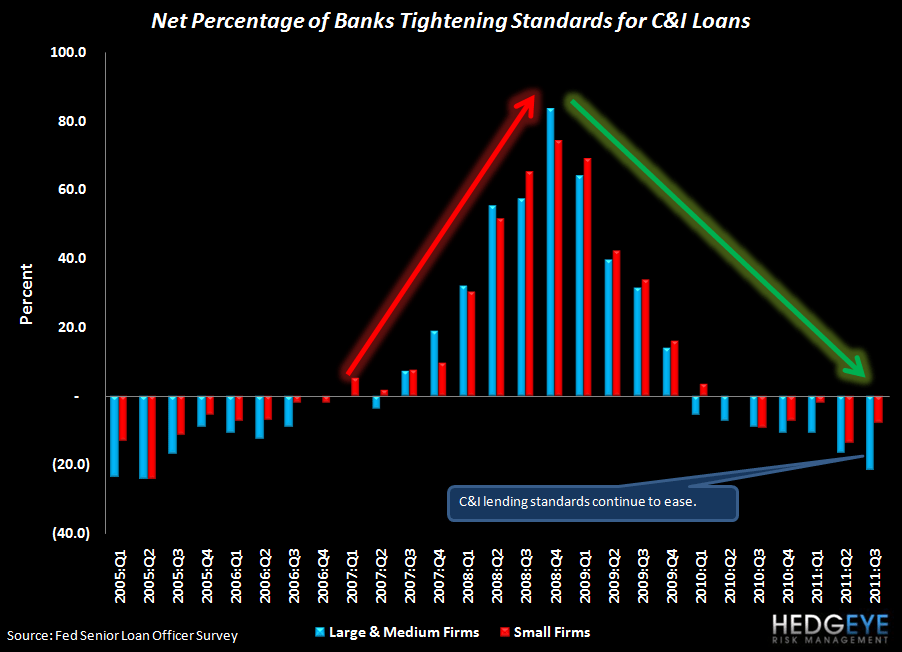

C&I Loans Continue to Move in the Right Direction

All trends are positive in C&I lending. More banks reported strengthening C&I loan demand again in 3Q. Lending standards are easing and spreads are contracting in C&I loans.

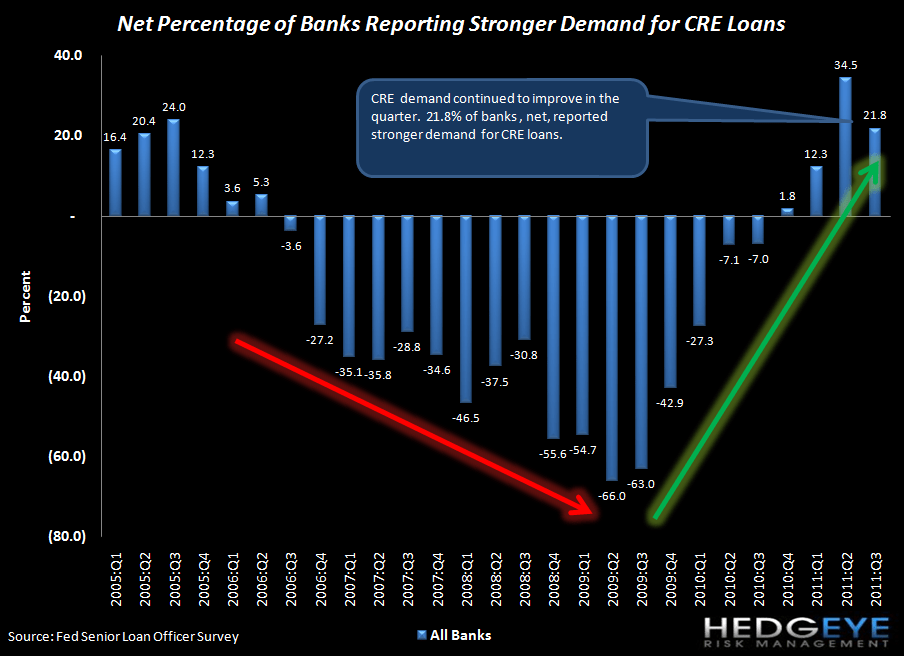

CRE Loans Also Now Moving in the Right Direction

CRE loan demand rose again in the 3Q survey coming on the heels of last quarter's strongest advance in years. Meanwhile, lending standards eased again this quarter - the second month in a row.

Residential Real Estate - Standards Finally Ease (Slightly) but Demand Continues to Fall

The residential real estate segment finally caught a break this quarter as banks reported a net easing of standards in 3Q11 for both prime and nontraditional loans. That said, the net easing was minimal with just 1.9% (net) of respondents easing standards on prime residential real estate loans and 4.2% (net) easing standards on nontraditional residential loans.

Also of interest is the fact that in spite of the modest easing of standards, demand continued to decline. Bankers reported lower demand (-1.9%) for prime residential real estate loans and home equity lines of credit. Nontraditional loan demand fell at 12.5% of banks surveyed (net).

Consumer Loans Show Improvement

On the non-mortgage consumer side, the percentage of banks expressing increased willingness to lend increased from Q2. Beyond this, the demand for these loans rose while lending standards eased.

Joshua Steiner, CFA

Allison Kaptur