THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - August 11, 2011

The French governments (and their bankers) now, allegedly, have an edge on what independent rating agencies are going to do with their sovereign ratings. Nice! The most important thing central planners have missed in 2011 are growth estimates – that won’t change gravity. As we look at today’s set up for the S&P 500, the range is 50 points or -3.01% downside to 1087 and 1.45% upside to 1137.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1500 (-4151)

- VOLUME: NYSE 2147.22 (-10.89%)

- VIX: 42.99 +22.62% YTD PERFORMANCE: +142.20%

- SPX PUT/CALL RATIO: 1.74 from 2.64 (-34.11%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 27.09

- 3-MONTH T-BILL YIELD: 0.02% -0.01%

- 10-Year: 2.17 from 2.20

- YIELD CURVE: 1.98 from 2.01

MACRO DATA POINTS:

- 8:30 a.m.: Trade Balance, est. (-$48.0b), prior (-$50.2b)

- 8:30 a.m.: Initial jobless claims, est. 405k, prior 400k

- 8:30 a.m.: WASDE (corn, soybean, cotton, wheat)

- 8:30 a.m.: Net export sales (commodities)

- 9:45 a.m.: Bloomberg consumer comfort: est. (-48.7), prior (-47.6)

- 10 a.m.: Freddie Mac mortgage rates

- 10:30 a.m.: EIA Natural Gas

- 1 p.m.: U.S. to sell $16b 30-yr bonds

WHAT TO WATCH:

- U.S. trade deficit probably narrowed in June from the highest level in almost 3 years, helped by cheaper imported crude oil, economists said before a report today

- Fed officials are drawing up rules for the largest U.S. banks that won’t be more stringent than global capital standards agreed to in Basel, people familiar said

COMMODITY/GROWTH EXPECTATION

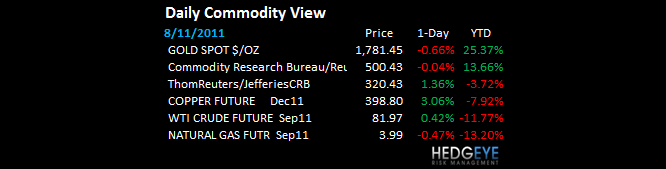

COMMODITY HEADLINES FROM BLOOMBERG:

- Gold Falls From Record as Rising Equities Curb Investor Demand

- CME Increases Gold Margins as Investors Drive Record Rally

- Rice Is Next Japan Food Risk From Fukushima Nuclear Meltdown

- Power Trading Set for Record on Europe Sun, Wind: Energy Markets

- Copper Climbs Most in Two Months on Chinese Demand Speculation

- Standard Chartered Recommends Buying Brent Oil Below $100

- Aussie, Kiwi Rise as U.S. Stock Futures, Commodities Advance

- Palm Oil Climbs as Malaysian Stockpiles Drop on Record Exports

- Metals Lead Commodity Gains as Yuan Strength Buoys China Demand

- Copper Climbs Most in Four Months, Lifted by Chinese Purchases

- Commodities Rise for Second Day, Led by Metals on China’s Demand

- Spot Gold Falls 0.6% After Rallying to Record Above $1,800

- Palm Oil Imports by India Seen at Record May Halt Price Decline

- Nestle Pakistan to Fend Off Engro by Doubling Dairy Output

- Being Like Soros in Buying Farmland Reaps Annual Gains of 16%

- Gold May Extend Record Rally Above $1,800 as Global Stocks Drop

- Thai Sugar Exports May Increase to Record, Cane Board Forecasts

- Oil Gains Most in Three Months as Supplies Fall, Demand Rises

CURRENCIES

EUR/USD – remains the most critical FX pair in all of global macro and this is really where the rubber meets the road on which European politician is telling you the truth; TREND line is now 1.44 and its bearish/broken - no bid this morn

EUROPEAN MARKETS

- EUROPE: another low quality short squeeze to lower-highs in the lowest quality country markets (Italy/Spain); not good

- FRANCE – important to acknowledge what real-time prices have been signaling in French Equities since February of 2011 when they put in another lower-long-term high – including this morning’s rally, the CAC40 has crashed (down -27% since FEB2011)

ASIAN MARKETS

- ASIA: not as bad as I thought it would act = constructive; China leads gainers (we're long) up +1.3%; Singapore day2 of neg divergence $CAF

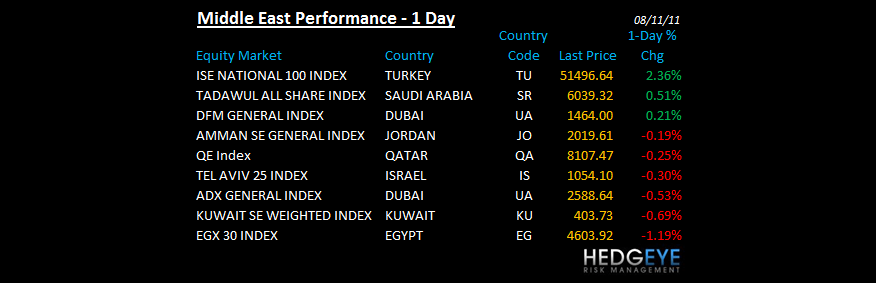

MIDDLE EAST

Howard Penney

Managing Director