Positions in Europe: Short EUR-USD (FXE); European Financials (EUFN)

As Keith wrote today in this morning notes: “From a research/risk management perspective, yesterday was one of the best days we’ve had versus our sell-side competition since ‘08. It was also the biggest down day for stocks since ‘08, so that makes sense. Having 0% asset allocation to US/European Equities helps.

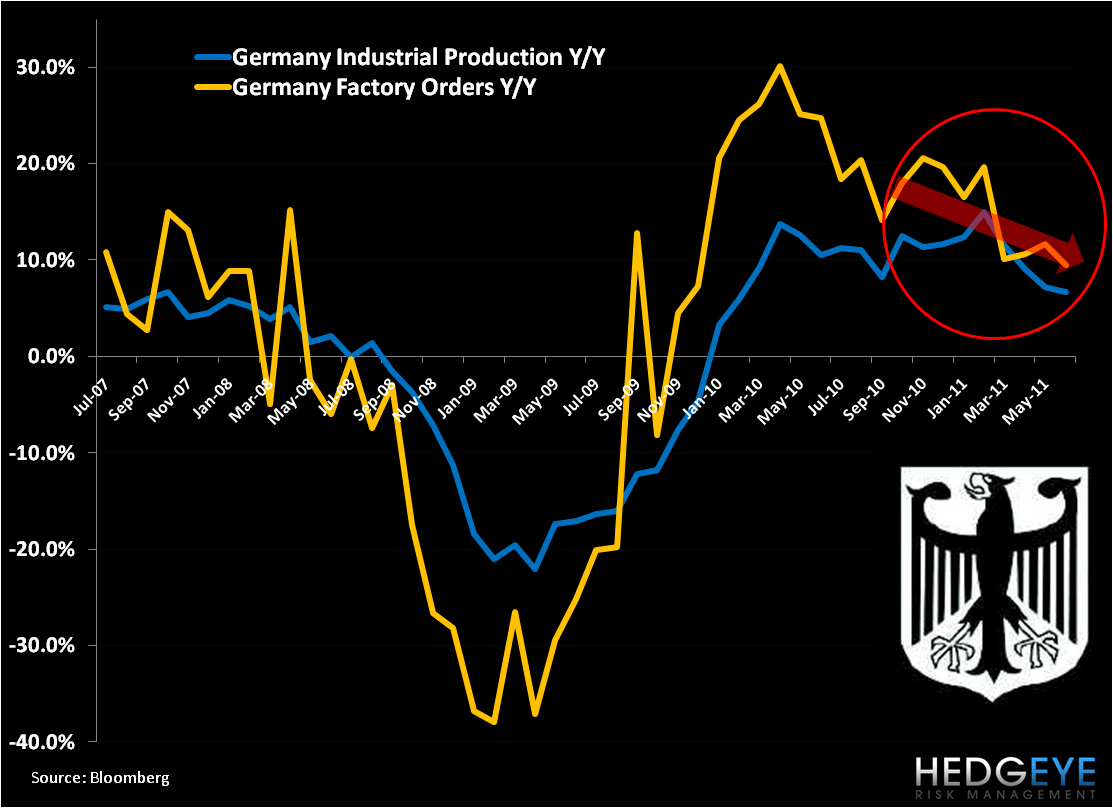

- GROWTH – is slowing… Period. The #1 headline in Europe this morning isn’t about a lying politician, it’s all about GROWTH. Slowing growth makes any leverage problem worse at an accelerating rate. IP growth down 2% y/y in Spain in June.

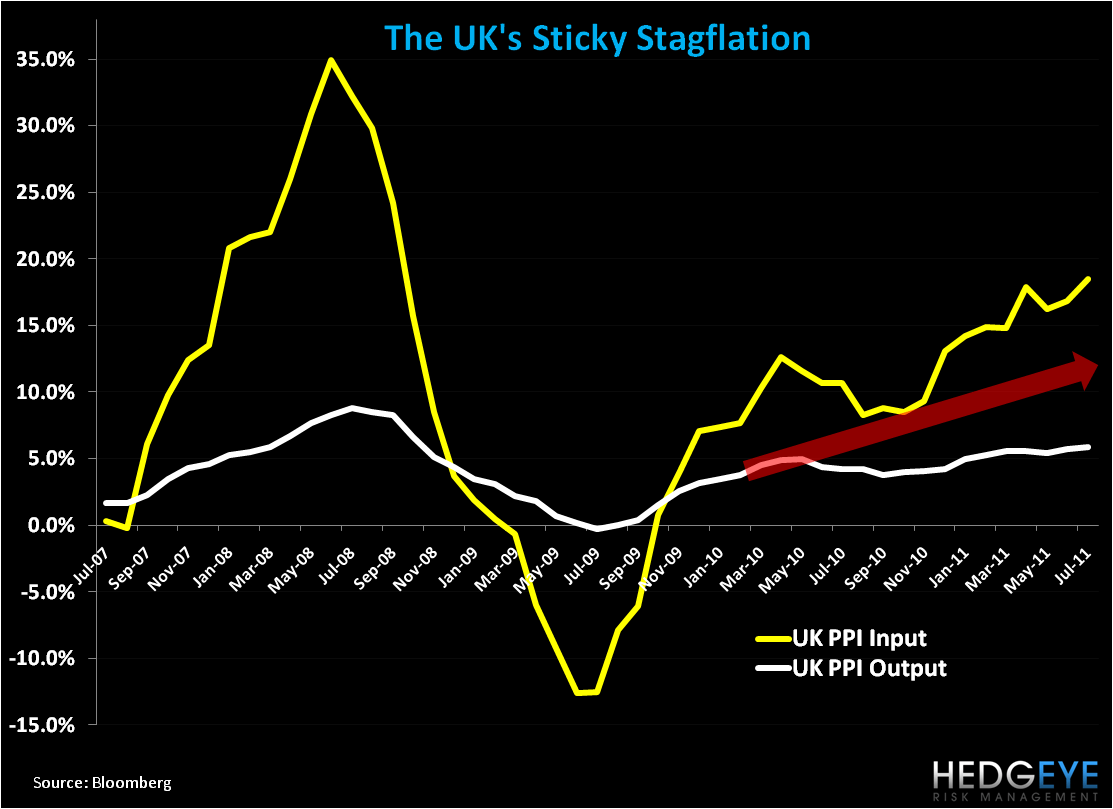

- STAGFLATION – stocks pay a lower multiple for that… Period. The #2 headline in Europe this morning isn’t about Europigs, it’s about UK input prices ripping higher to +18.5% Y/Y in July vs +17% in June. That will come down in AUG, but that’s bad for margins.

- LEVELS – bearish and broken… Period. Every Global Equity market in the world (other than Venezuela) is now officially broken on both my TRADE and TREND durations. In commodities, both Copper and WTIC Oil snapped TRADE and TREND lines this week. And in Fixed Income, UST bonds are hitting new highs as Growth Slowing + Deflating The Inflation is bullish for UST bonds.

Every bear market gets immediate-term TRADE oversold, and that’s what I see this morning. That said, I want to be crystal clear on this, sell all rallies in Equities/Commodities because the Street is still too long and needs to take down gross and net exposures.”

As it relates specifically to Europe, European equities took it on the chin this week. On a one week performance basis: Finland’s OMX -14.0%; Italy’s MIB -12.1%; Greece’s ATHEX -11.8%;Germany’s DAX -11.7%; Ireland’s Overall Index -10.1%; France’s CAC -9.4%; and Portugal’s PSI20 -7.9%, to name a few indices. Neither the periphery nor the heart of Europe was immune to the decline.

The EUR-USD saw substantial day-over-day gains this week, but traded within our range of $1.40 to $1.43. Importantly, we want to stress that if both our TREND level of $1.43 and TRADE level of $1.40 on the EUR-USD pair break, we don’t see downside support until $1.28.

This week our Financials team had a call with Peter Atwater, and among his many astute comments I agree with his assessment that France is one key country to monitor as it relates to sovereign debt contagion. In particular, Atwater notes there’s a real threat that France could lose its AAA credit rating. This point is critical for the AAA rated bonds issued by the EFSF can only maintain this rating so long as the countries backing the facility maintain their AAA status. And France, behind Germany, has the second largest collateral guarantee on the facility—therefore a downgrade of France would be a huge impairment on the facility, which already looks significantly underfunded should Italy and Spain require assistance.

This leaves us increasingly comfortable to short France and Germany on a bounce. Below we show CDS spreads as one indicator of the building risk premium for the two countries commonly understood as Europe’s backbone. While both are far from CDS levels reached by the PIIGS, or even the 300bp line that we’ve noted as an important breakout line, both countries will be front and center on our screens.

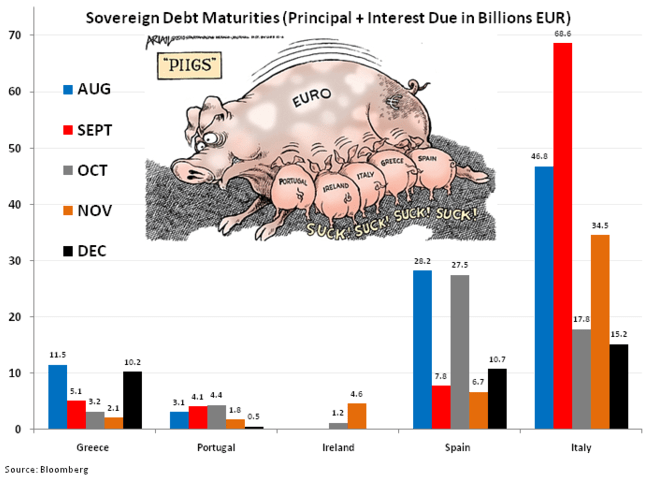

Given that the EU parliament doesn’t return to session until mid September to vote on the terms of the newly crafted EFSF, we have a number of weeks of indecision ahead of us – we think this bodes poorly for a region that has struggled over the last two years to present credible plans to arrest sovereign debt contagion. Further, comments yesterday from ECB President Trichet that the Securities Markets Program (SMP) to buy up sovereign bonds would partially resume indicates that the Bank will need to continue to support demand for future PIIGS auctions, especially until the terms of the EFSF are finalized in September. On this score, we’re particularly worried about Italy and Spain, given their steep maturity schedules into year-end and rising bond yields.

Sentiment shock waves also came in the form of an announcement yesterday from Spain’s Treasury that it has suspended a bond auction originally planned for August 18th, but noted the cancellation of the auction was not a response to market turbulence (throat clear).

Below we show two charts that stood out in today’s data—UK input cost inflation, which highlights our call on the stagflation component of our sticky stagflation thesis in the UK; and slowing high frequency German data, including Industrial Production and Factory Orders.

Matthew Hedrick

Senior Analyst