Positions in Europe: Short EUR-USD (FXE); EU Financials (EUFN); Covered Italy (EWI) and UK (EWU) on 8/1

Eurozone PMI Services Fall

In line with our call for growth slowing across Europe, Eurozone Services PMI for the month of July came in lower, confirming a downward trend over the last 3-4 months that we also saw with July Manufacturing PMI figures (see chart below). With the 50 line marking expansion (above the line) and contraction (below), Manufacturing across Europe has taken a larger hit than Services over the intermediate term, and the results show that even Europe’s economic stalwarts were not immune to the downtrend: German and French Services fell to 52.9 and 54.2, respectively.

While Italy improved month-over-month to 48.6, the country remains grounded under the 50 line; risks to Italy’s economy remain its (in)ability to finance its sovereign debt; its banking industry’s leverage to the periphery; and political indecision (including the terms of its austerity package) of the Berlusconi government. We covered our position in Italy via the etf EWI on 8/1 for a +7% gain. We continue to believe that the region’s sovereign debt contagion will remain a significant drag on consumer and business optimism and impair growth into year-end across much of the region.

Shifty Swissy

Today the Swiss National Bank (SNB) unexpectedly cut the 3M Libor Target Rate to 0.00% from 0.25% (a level it had been at since March 2009) and said it will "significantly increase the supply of liquidity to the Swiss franc money market, including by expand banks' sight deposits at the SNB from currently around 30 billion CHF ($39.35 billion) to 80 billion CHF."

Unknown is the extent to which the SNB sells the CHF from its reserves. 2009 and 2010 showed that the SNB’s intervention was largely unsuccessful in depreciating the CHF against major currencies, and we think this time around is no different. Today’s cut did push the CHF down against major currencies in the intraday morning session by 1-3%, however we think that CHF strength will resume as a safe haven from the volatility in the Eurozone and its common currency over the intermediate term.

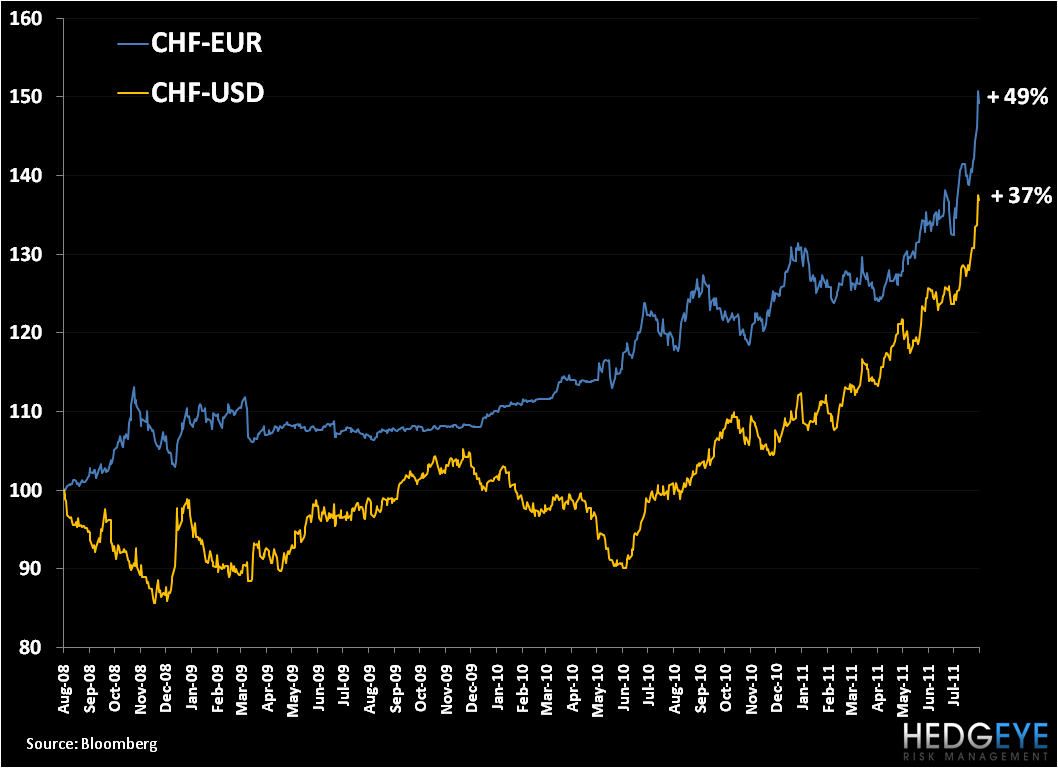

For reference, over the last 3 months, the CHF-EUR is up +14% and the CHF-USD pair gained +11%. As we show in the chart below, over a three year period, the CHF-EUR is up +49% and CHF-USD has gained +37%! Sooner or later this strong CHF vs the EUR and USD will erode exports. While we’ve yet to see this ytd, it’s a risk that must be weighing on SNB President Philipp Hildebrand in today’s move. Unfortunately, given the larger macro forces in the region, we think Hildebrand and the bank are largely handcuffed to use monetary policy as a tool to influence the direction of the CHF.

Levels on EUR-USD

The EUR-USD has whipped around in the last weeks on the US debt ceiling debate. We continue to highlight that the EUR-USD will see immediate term support in a band of 1.41- $1.45 as EU officials support the region’s fiscal imbalances with bailout band-aids at every step. However, should we break through our intermediate term TREND level of $1.43 and immediate term TRADE support level of $1.41, we see long term TAIL support all the way down at $1.28, or -9.2% from $1.41. Be aware of this quantitative set-up as sovereign debt contagion risk looms with the larger players of Italy and Spain moving to the forefront.

Matthew Hedrick

Analyst