THE HEDGEYE BREAKFAST MENU

Notable news items, macro data points, and price action pertaining to the restaurant space.

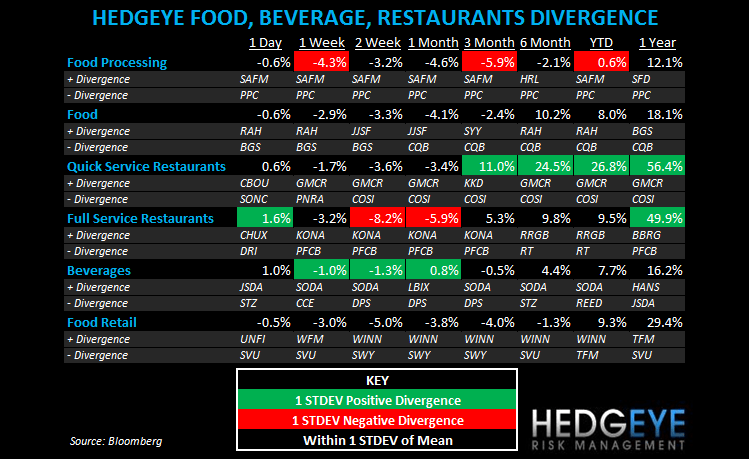

MACRO

Consumer

News hitting the tape this morning that consumer spending unexpectedly dropped in June for the first time in almost two years. A slump in hiring, according to Bloomberg, caused households to retrench.

The ICSC chain store sales index ended its string of gains with a 0.3% decline last week. Year-over-year growth moderated slightly but remained robust at 4%. The ICSC reported improved customer traffic at discounters.

U.S. comparable sales rose 4.5% in week ended July 30 year-over-year, according to Johnson/Redbook. Month sales through July 30th were up 4.3% year-over-year, down -0.5% month-over-month. Redbook sees August comparable sales up 4.6% year-over-year.

Subsectors

Full service restaurant stocks traded well yesterday ahead of TXRH earnings post-close and DIN earnings this morning. Both earnings reports were a disappointment, however.

QUICK SERVICE

- DNKN’s growth strategy has been questioned by Irwin Barkan, author of “Dunk’d, A True Story of How Big Money is Corrupting the Franchising Industry”. Barkan rubbishes the “white space opportunities” that the company executives like to highlight, saying that “they’ve been trying to fill up that white space for 30 years”.

- The coffee names traded strongly yesterday with the exception of SBUX.

- MCD has entered a five-year IT support deal with Fujitsu. The IT services provider will roll out “user-exchangeable parts” to McDonald’s 1,200 branches throughout the UK and Ireland.

- MCD franchisee ARCO reported EPS yesterday. MCD Brazil SSS +10.2%; NOLAD's (Mexico, Panama and Costa Rica) SSS +9.7%; SLAD's (Argentina, Venezuela, Colombia, Chile, Peru, Ecuador, and Uruguay) SSS +33.1%; the Caribbean division (Puerto Rico, Martinique, Guadeloupe, Aruba, Curacao, F. Guiana, US Virgin Islands of St. Thomas and St. Croix) SSS -0.3%.

CASUAL DINING

- TXRH posted 2Q earnings last night. EPS came in at $0.22 versus $0.23 consensus. Sales were in line but the company guided down on full year EPS. Inflation continues to be a concern. See our note from this morning for more details.

- DIN reported 2Q EPS of $0.90 versus consensus $1.02. Same-restaurant sales for the Applebee’s system were +3.1%. Two-year average trends were flat on a sequential basis.

Howard Penney

Managing Director

Rory Green

Analyst