Higher estimates should continue the positive momentum in the stock.

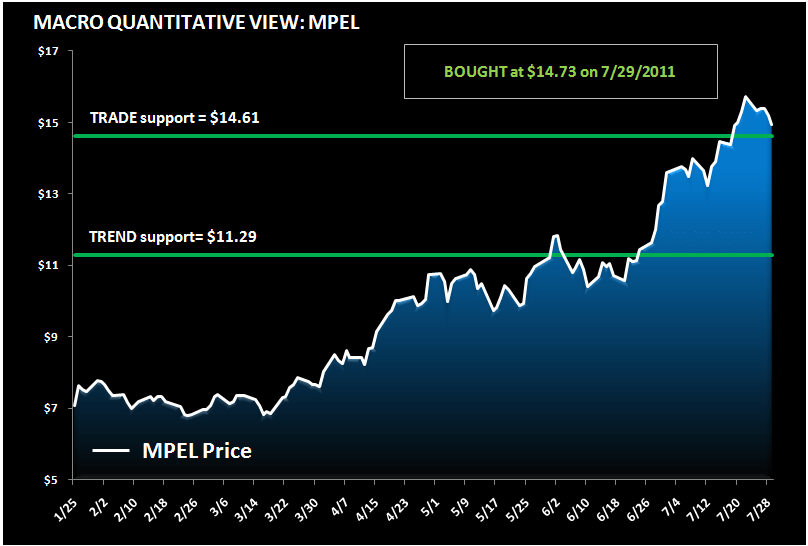

Keith bought MPEL in the Hedgeye Virtual Portfolio today at $14.73 ahead of its upcoming Q2 earnings report. The stock is trading close to a key TRADE support level. MPEL has been our top idea for almost a year due to our projections of consistenly better than expected earnings. The Q2 earnings release should be the best of the bunch and will likely be the next catalyst. The company has gained market share YoY, despite Galaxy Macau opening on Cotai, and July share has been trending higher for MPEL so Q3 also looks like a big beat. At 12x 2012 EBITDA, MPEL is still trading at a discount to most of the Macau players despite the huge outperformance of the stock. Layering in the future development of the best site in all of Macau - Macau Studio City - completes the MPEL growth story.