THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - July 29, 2011

As we see it the Debt Ceiling Debate = political drama; that’s it – it’s not being priced into either A) a US currency crash or B) US Treasury Yield credit risk. Sure, it’s being priced into US stocks, but I think what people are missing is that so are A) Europig problems and B) EPS expectations. As we look at today’s set up for the S&P 500, the range is 24 points or -0.67% downside to 1292 and 1.18% upside to 1316.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -725 (+1836)

- VOLUME: NYSE 986.85 (-10.22%)

- VIX: 23.74 +3.31% YTD PERFORMANCE: +33.75%

- SPX PUT/CALL RATIO: 1.60 from 2.92 (-45.29%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 18.28

- 3-MONTH T-BILL YIELD: 0.07% -0.01%

- 10-Year: 2.98 from 3.01

- YIELD CURVE: 2.56 from 2.57

MACRO DATA POINTS:

- 8:30 a.m.: GDP, QoQ Annualized: est. 1.8%, prior 1.9%

- 8:30 a.m.: Personal consumption, est. 0.8%, prior 2.2%

- 9:45 a.m.: Chicago Purchasing Manager, est. 60.0, prior 61.1

- 9:55 a.m.: UMich Confidence, July final, est. 64.0, prior 63.8

- 10 a.m.: NAPM Milwaukee, est. 56.9, prior 59.3

- 1 p.m.: Baker Hughes rig count

- 3:15 p.m.: Fed’s Bullard, Lockhart discuss monetary policy in Wyoming

WHAT TO WATCH:

- Treasury contingency plan on debt is said to give priority to bondholders. Obama officials said to release plan no earlier than after the close of markets today.

- Spain faces Moody’s rating reduction from Aa2

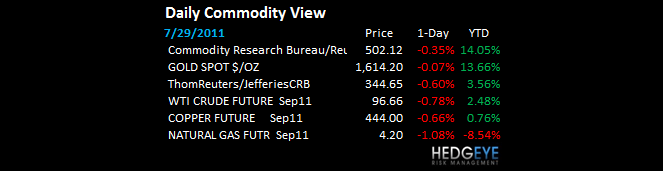

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Sugar Exports From India at Four-Year High May Cool Prices

- Sugar Falls as Surplus May Become Available; Coffee Advances

- Gold May Fall in London as Rally to Record Spurs Investor Sales

- Copper May Fall on Concern About Potential U.S. Debt Default

- Nickel Surplus to Narrow on China’s Demand, Sumitomo Says

- Gold May Repeat 1970-80 Bull Market on Europe Debt, U.S : Citi

- China May Boost Corn Imports to Record on Re-Stocking, Hog Herds

- Coffee May Decline 15% to Fibonacci Level: Technical Analysis

- BHP Chile Workers Vow to Prolong Strike at Biggest Copper Mine

- Gasoline Profit Doubling Cuts Naphtha to Asia: Energy Markets

- Vale Plans $3 Billion Dividend as Net Income Misses Estimates

- Gold May Decline as Rally to Record Spurs Sales, Survey Shows

- China Gold Demand May Surpass India This Year, Goldcorp Says

- Radiation-Free Food Bolsters South Korea’s Exports to Japan

CURRENCIES

EUROPEAN MARKETS

- EUROPE: ring the gong; this Europig mess has nothing to do w/ Congress; straight down this wk across Europe b/c debt maturities ramp in AUG

- UK Jul house prices (0.4%) y/y vs consensus (0.9%) andn prior (1.1%)

- Germany June retail sales (1.0%) y/y vs consensus (1.8%), prior revised +3.1% from +2.2%

- France June consumer spending +1.2% vs consensus +0.5%, prior revised (0.3%) from (0.8%)

- France June producer prices (0.1%) vs consensus +0.1%and prior (0.5%)

- UK Jun mortgage approvals 48.4k vs consensus 46.0K

- EuroZone July flash CPI +2.5% vs consensus +2.7%

ASIAN MARKETS

- ASIA ugly overnight with Taiwan down the most on a slowing economy and the TSMC miss

- Japan June core CPI +0.4% y/y vs cons +0.5%; overall household spending (4.2%) y/y vs cons (2.3%).

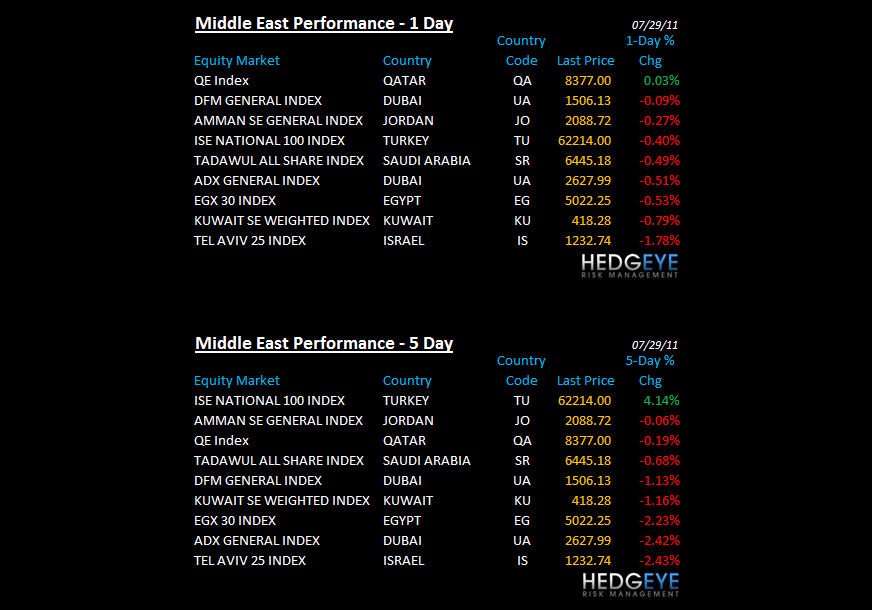

MIDDLE EAST

Howard Penney

Managing Director