THE HEDGEYE BREAKFAST MENU

Notable news items and price action from the restaurant space as well as our fundamental view on select names.

MACRO

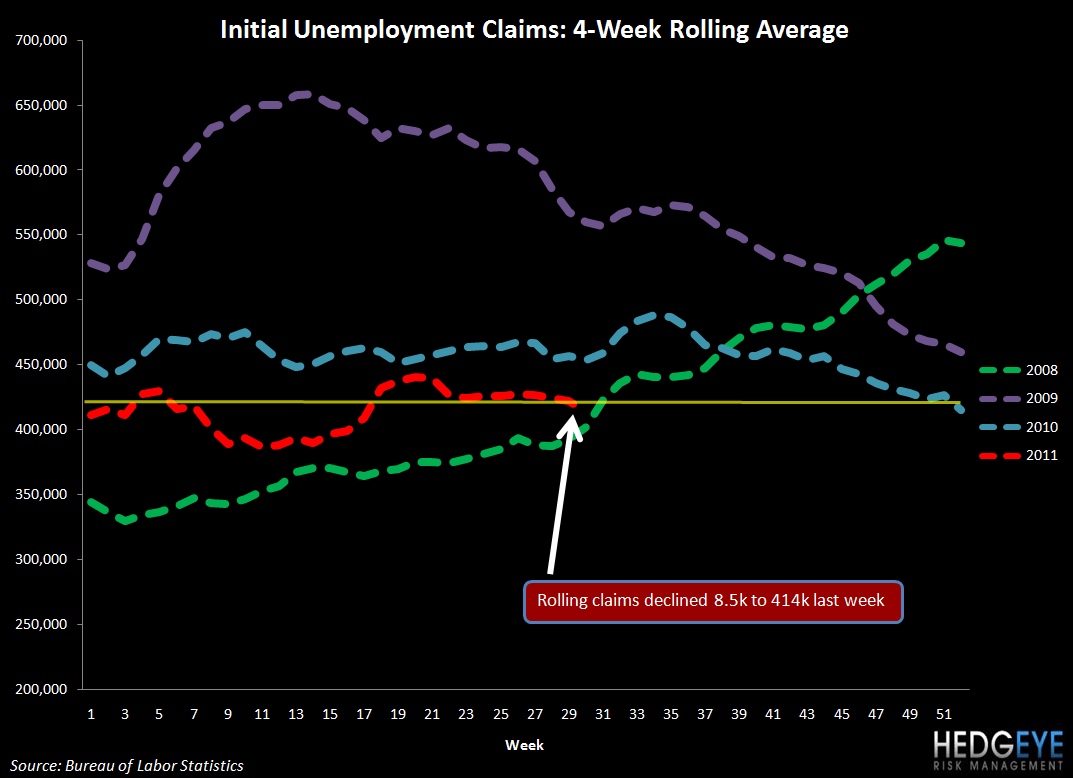

Unemployment

Initial jobless claims came in at 398k for the week ended 7/23, down 24k from the previous week’s revised number of 422k. The four-week rolling number declined by 8.5k to 414k.

Commodities

Coffee was weighed down by growing inventories at European ports and assessments of crop positions in top producer Brazil improved.

Europe

Eurozone economic sentiment worsened more than expected this month. Optimism faded in all sectors, according to the data collected by the European Commission. The European Commission Economic Sentiment Indicator has been declining since February. The monthly index, based on a survey of businessmen and consumers across the 17-nation euro zone, fell to 103.2 in July from 105.4 in June.

Subsectors

Restaurants continue to underperform, confirming further a change in how these sectors trade. For much of the past year, restaurants have been outperforming; now it seems that the space is underperforming food and beverage categories.

QUICK SERVICE

- WEN rated “New Buy” at Janney on accelerating same-store sales. We wonder if the QSR industry is doing that well; MCD is also seeing strong SSS.

- GMCR reported after the close yesterday and blew away expectations. We expect some positive flow through for the coffee space today.

CASUAL DINING

- EAT was upgraded to “Buy” from “Hold” at Miller Tabak. This stock has been a Hedgeye favorite for some time.

- PFCB was cut to sector perform at RBC Capital after it put up a terrible quarter and guidance yesterday.

- KONA is the Teflon Don of the space, at least for now. KONA gained 7.5% on accelerating volume in a horrible tape. We believe that there is more to come from this company in 2011 and that their remodel program will support improved trends.

Howard Penney

Managing Director

Rory Green

Analyst