TODAY’S S&P 500 SET-UP - July 28, 2011

In a market like this, where Institutional performance chasing is one of the most misunderstood long-term TAIL risks we’re observing, price levels matter – big time. So does considering them on a multi-factor, multi-duration basis. As we look at today’s set up for the S&P 500, the range is 18 points or -0.53% downside to 1298 and 0.85% upside to 1316.

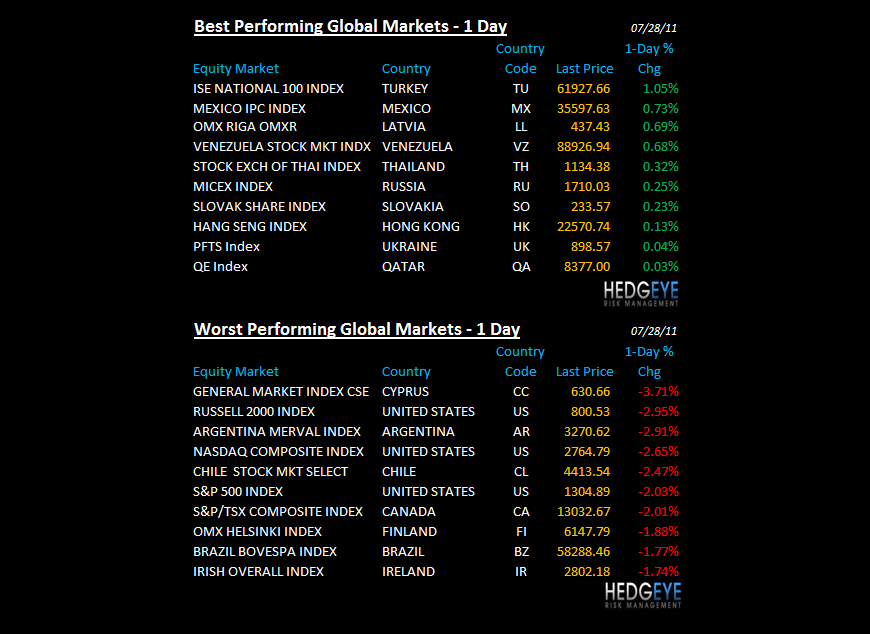

SECTOR AND GLOBAL PERFORMANCE

- The Industrials (XLI) really signaled this Tuesday; yesterday decline was a broad based confirmation that the biggest problem the US stock market faces are forward earnings expectations - not a US debt default (which didn’t move US Treasury credit risk more than a basis point all day). From Healthcare (which we are long) to Tech yesterday, the earnings guidance was just not good - growth is slowing. The Hedgeye models now have 5 of 9 Sectors are now Bearish TRADE and TREND (XLF, XLI, XLB, XLP, and XLV) and only 3 of 9 Sectors are bullish TRADE (XLE, XLK, XLU).

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2561 (-1587)

- VOLUME: NYSE 1099.23 (+31.33%)

- VIX: 22.98 +13.59% YTD PERFORMANCE: +29.46%

- SPX PUT/CALL RATIO: 2.92 from 1.99 (+46.90%)

CREDIT/ECONOMIC MARKET LOOK:

UST Yields – market morons in Washington have finally busted the 2-year yield above my TRADE line of resistance (0.41% on 2s) this morning. Will it hold? Its anybody’s guess - what I do know is that I trust the market price is going to lead us more than a compromised politician

- TED SPREAD: 18.17

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 3.01 from 2.99

- YIELD CURVE: 2.58 from 2.61

MACRO DATA POINTS:

- 8:30 a.m.: Initial jobless claims, est. 415k, prior 418k

- 9:45 a.m.: Bloomberg Consumer Comfort, est. (-44.9), prior (-43.3)

- 10 a.m.: Pending home sales M/m: est. -2.0%, prior 8.2%

- 10:30 a.m.: EIA Natural Gas

- 12:45 p.m.: Richmond Fed’s Lacker speaks in Virginia

- 1 p.m.: U.S. to sell $29b 7-yr notes

- 2:30 p.m.: San Francisco Fed’s Williams speaks in Utah

WHAT TO WATCH:

- House plans to vote today on a debt-limit increase proposal that confronts unified Democratic opposition in the Senate

- House Speaker John Boehner to hold news conference at 1:30 p.m.

- Health-care spending to make up 20% of U.S. GDP by end of decade, up 2+ pct pts from 2009 as subsidies expand, federal auditors said.

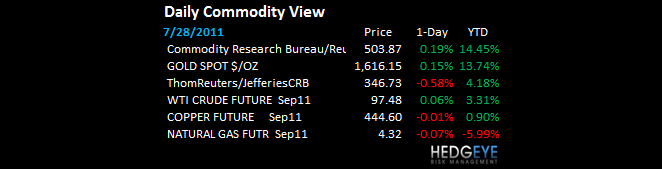

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Record Low Rubber Stocks-to-Use Ratio May Lift Prices, RCMA Says

- Copper May Rise as Strike, Lower Production Fuel Supply Concern

- Wheat Advances Third Day on Speculation U.S. Yields May Decline

- Coffee Falls on Rising Inventories in Europe; Sugar Retreats

- Soybeans to Gain 9.2%, Trading Central Says: Technical Analysis

- BHP’s Chile Copper Mine Declares Force Majeure Amid Strike

- Brazil Coffee Output to Surge After Prices Rise, Rabobank Says

- Container-Ship Plunge Signals U.S. Slowdown: Freight Markets

- Radiation Concern Prompts Aeon to Test Beef for Cesium Level

- India’s BJP Asks Karnataka Chief to Resign Over Mining Scam

- LNG Heads for Three-Year High on Japan, Libya: Energy Markets

- China Shipping Companies Lobby to Foil Vale’s Iron Ore Fleet

- African Farmers Challenge ADM for Bigger Share of U.S. Food Aid

CURRENCIES

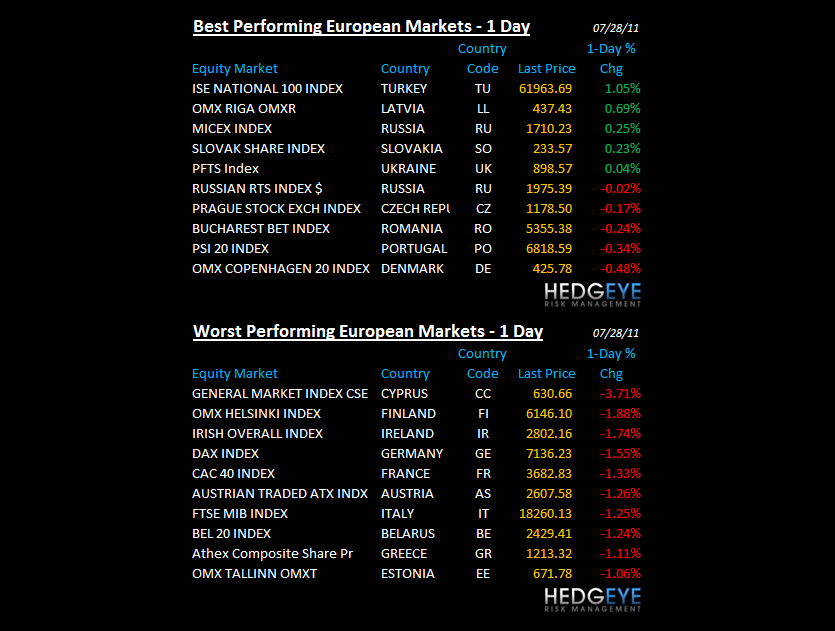

EUROPEAN MARKETS

- EUROPE – both Equities and Bonds are turning into proactively predictable trains wrecks. The catalysts are crystal clear (accelerating debt maturities for the majors through September), and all TREND lines have been broken/confirmed by volume/volatility studies.

- EUROPE: Just awful. Period. With Italy crashing, Germany leads to the downside this morn and thats a very unhealthy signal; DAX = bearish TREND

- Germany July unemployment rate +7.0% vs consensus +7.0% and prior +7.0%

ASIAN MARKETS

- ASIA: acts nothing like USA or Europe, because they have nothing that resembles A) Congress or B) Europig Debt - selloff was controlled

MIDDLE EAST

Howard Penney

Managing Director