Below is an excerpt from the Dunkin' Donuts Black Book that we published today.

With valuations for the DNKN peer group having increased 56% over the past 12-months, the aggregated market caps of the few largest publicly traded coffee-centric companies almost equals the entire US coffee market’s annual revenues.

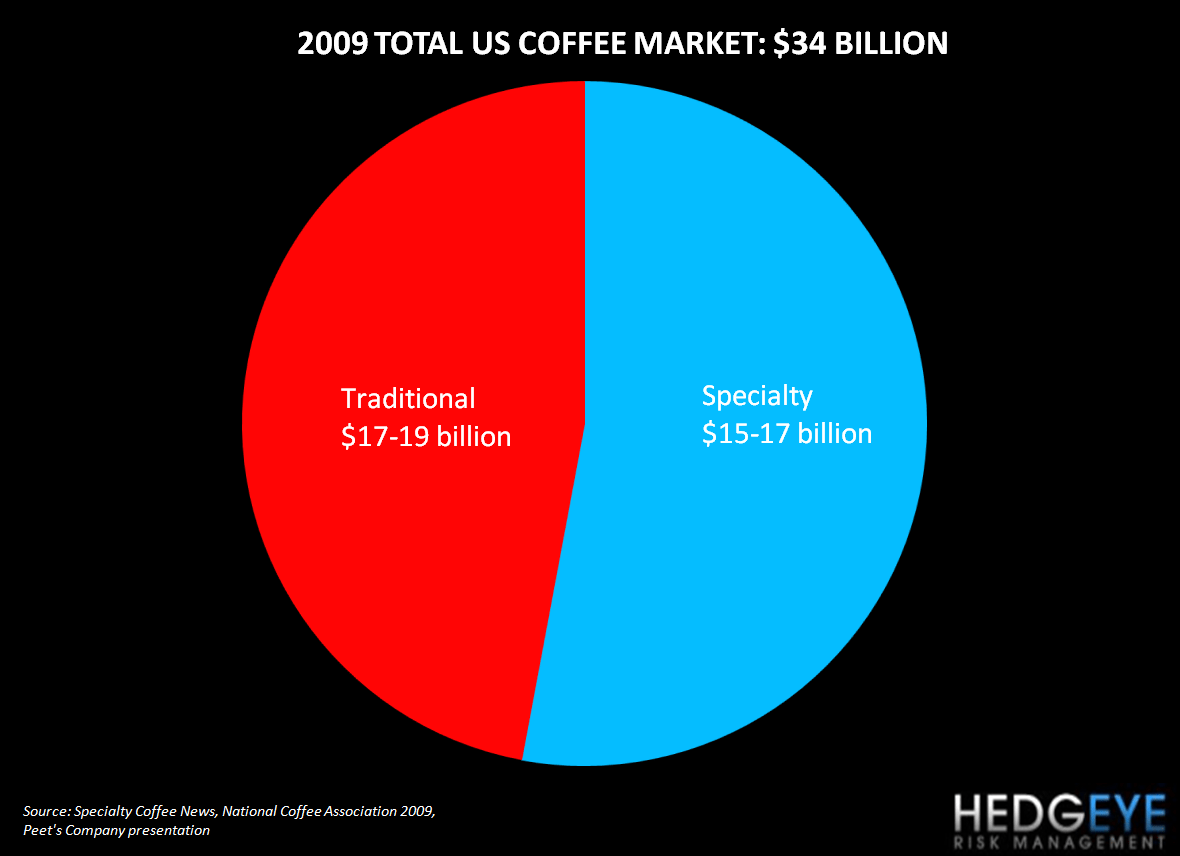

According to the National Coffee Association, the US coffee market represented $34 billion in 2009; the specialty coffee category generated $15-17 billion in annual revenues and the traditional category brought in $17-19 billion. It would be a conservative measure to assume the high end of these ranges to estimate the present size of the market, bringing the current size of the market to $36 billion. The coffee space is partly comprised of some very sizable companies with significant capital reserves that compete fiercely with one another for market share. A front-runner in the corporate coffee war thus far is Green Mountain. The company’s domination of the “at-home” coffee industry through Keurig machines and K-Cups has generated handsome returns. The growth prospects for GMCR remain vast, at least if you share the view of investors; the stock currently trades at 29x EV/EBITDA and has a market capitalization of approximately $14 billion. Green Mountain’s market cap equals roughly 40% of the estimated $36 billion US coffee market’s revenues or 117% of the “at-home” US coffee market’s $12 billion in annual sales. While GMCR has recently expanded into Canada, the company is close to a pure play on the US market.

Turning to Starbucks, if we apply a 7x multiple to the company’s US EBITDA, the business would be valued between $10-11 Billion. This hypothetical value, added to the Green Mountain market cap, implies that the cumulative market caps of the two companies equals roughly 70% of the entire US coffee markets annual revenues. Lastly, MCD on Friday became the first restaurant company to grow its market cap north of $100 billion largely due to strong 2Q earnings results that were driven by success in selling coffee and other beverages. Could coffee stocks be in a bubble at the moment? We certainly think so.

Howard Penney

Managing Director

Rory Green

Analyst