This P&L is jacked up like the love child of Conseco and Bonds. The margin and capital deployment story over our TAIL duration is in the top 10% of retailers. But there are still a few near-term questions around our TREND duration that we need answered before getting involved.

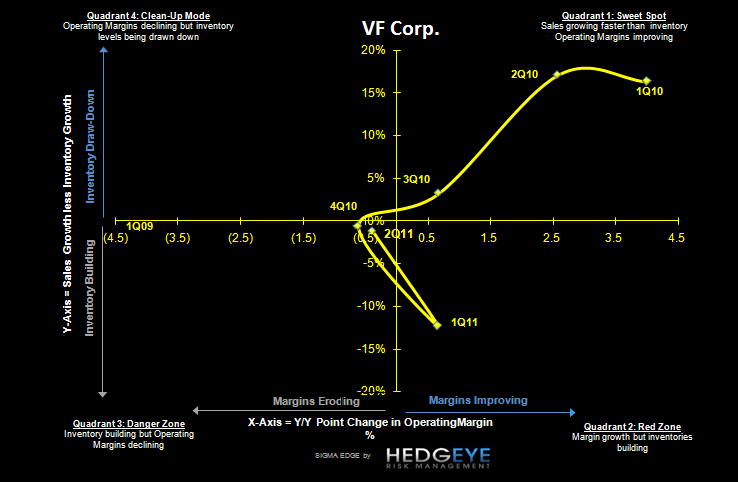

This VFC model is simply humming. It feels so odd for us to say that. After all, VFC is a portfolio of brands, and therefore should – in theory – not be able to meaningfully outperform the space as a whole. But low and behold, the company puts up 15% top line growth, and takes up guidance by 56% more than the 2Q beat, which is a bold move in this environment, And that’s before accounting for the addition of Timberland late in 3Q once that acquisition is completed. Furthermore, VFC is one of the few companies this quarter to show a significantly positive SIGMA swing – whereby the sales/inventory spread is compressing at the same time margin compares are looking more favorable. This is core to our TREND duration (three months or more).

We took our model out to 2015 (our TAIL duration = 3-years or less), as we think it’s warranted given the timeframe needed to most appropriately assess the potential for value creation at TBL. In doing so, VFC is one of the few companies that we have accelerating its operating profit margins with disproportionately less capital. Yes, some of this is driven from optimizing what has been a pathetically inefficiently-managed Timberland. But in the end, numbers don’t care about rationale. They are what they are.

Then why are we not more constructive on TBL? We’re asking ourselves the same thing. The crux of it is that we’re modeling slightly lower core earnings in the back half than VFC is guiding. In the end, we think that they’ll hit aggregate estimates, but it will be because of opacity around the Timberland acquisition. Don’t get us wrong – we’re not suggesting numbers games here (as we often do with companies in this space). VFC has been so good with disclosure around the drivers in each of their businesses. But we think that the pricing trends in the denim business in particular are not sustainable. Note that Levi’s reported 7% domestic revenue growth in Q2 with more than half from pricing (VFC is planning for pricing to be up 8% for the year) and it’s launching its lower price point ($20-$30) Denizen brand in Q3. Moreover, it’s unlikely that competitors such as Gap and Rustler (WMT) are going to roll over and play dead. This is by no means the end of the world for VFC. They’ll manage through it.

This is a name that has certainly surprised us – both in growth, profitability and ultimately the stock price. We’ve been covering it long enough to ‘get it’ that the management team is artful in beating expectations, and yet we still have been positively surprised. The model today is telling us that 2013 earnings power is approaching $10. Does the stock look expensive now? Actually, the answer is No. Trading at about 13.5x next year's earnings and 8.5x EBITDA, which is fair for a name that has so many operating levers and drivers.

Would we classify this as a freight train like Nike that is plowing through anything in its path? Not really. But it is akin to one of those steel roller coasters that is locked so tightly onto the tracks such that it can do all the loops and inversions without whiplashing its paying customers.

The bottom line is that there is much to like here for someone who invests according to our TAIL duration. But before getting involved, we need more certainty around the TREND, and the stock price to go with it.

Here are some noteworthy comments from the call on the current pricing environment:

Pricing:

- Expect pricing to contribute 3-4% to full-year top-line growth, 2/3 of which will come from Jeanswear

- “we are seeing a little less impact from pricing than initially anticipated.”

- “Additional prices the increases will take place in the second half as planned.”

- “Of course, this is great news to us, but it too early to predict the impact on 2012. I will tell you this.”

- “our decisions around pricing , particularly for our US jeans businesses, have been good ones…we never contemplated fully offsetting cost with pricing.”

- “Our initial price increases in both the mid-tier and mass channels have been successfully executed and as Eric noted earlier, we are encouraged by the results to date with first and second half unit volumes above last year's levels.”

- “we're seeing some reduction in our fourth-quarter denim buys versus our costs in the third quarter, so that means in the first quarter of 2012, our cost our denim costs will begin to come down”

- Q: Given price increases realized thus far, do you expect those to hold, or are you working with retailers to reduce prices as you look out (to 2012)?

- A: “Again bear in mind that we did not take in our increases up all the way to cover our production costs so we think that was the prudent approach for all of the year and then going to next year we think that puts us in a good spot with our retailer community.” (i.e. No, we are not planning to lower prices)

- Q: Any surprises in the pricing environment?

- A: “No. So far the price increases that we expect to see, we're seeing.”

- Could we be positive in terms of units?

- “We're not anticipating that as we said very early in the year, that particularly in the second half in the first half units as we've said, it's been very positive for us. First half units in our US jeans business are up a couple percentage points over the first half of the 2010, so again, really like to see that. And that's great news.

- But we still have a second half plan down in terms of second half units for the year, we were looking at a mid-single digit percentage decline in our US jeans business on those ongoing programs and we're still planning something more like that.

- If the consumer response a little differently, could be a little better than that?

- Sure.

- But that's not how we have the numbers forecasted.

- “In terms of jeanswear, we are having the unit increase in the first six months of the year a little bit better than we hope to given the price increase that we took and for the year, we're calling for a mid-single digit decrease in units. So we have a lot of erosion that happens in the back half of the year to get to the mid-single-digit unit decrease from where we started and from where we're starting with positive trends coming in. We have a lot of experience in price changing and all of our channels of distribution, and have a pretty good feel for what it might be like.”