This note was originally published at 8am on July 15, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Observe due measure, for right timing is in all things the most important factor.”

-Hesiod

On Monday I titled my Early Look “Timing Matters.” It still does.

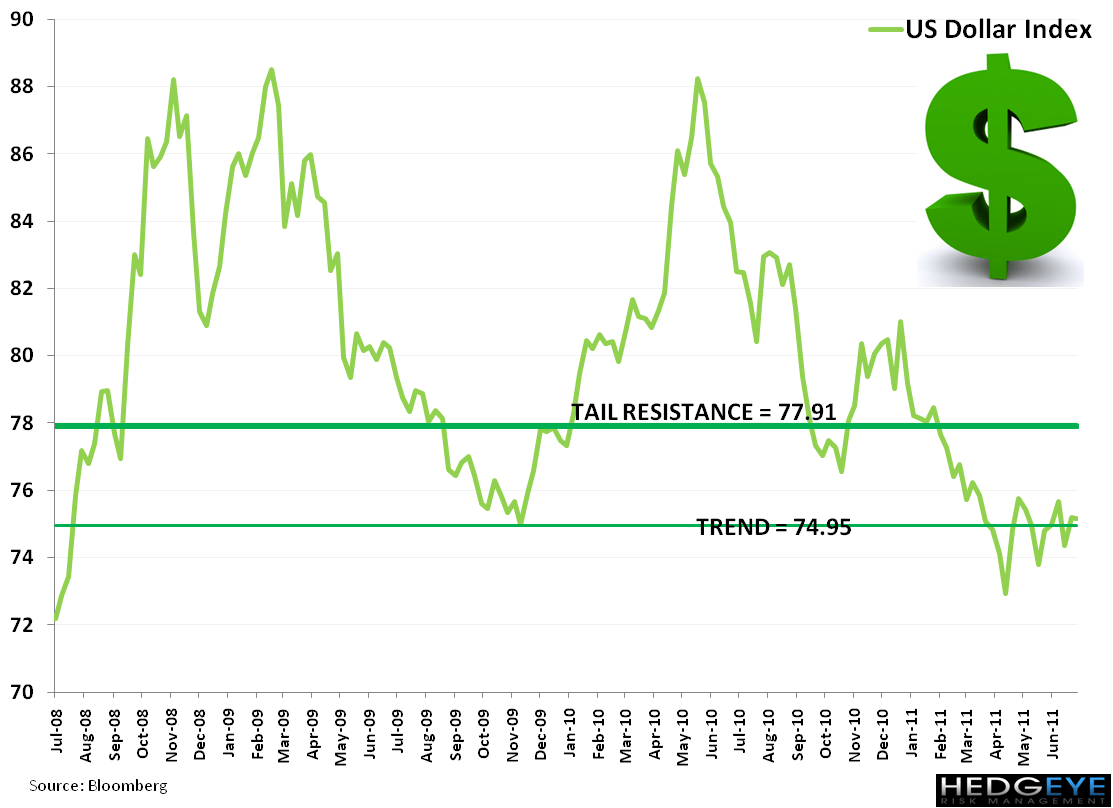

If you are proactively prepared to play this game, you will capitalize on opportunities while your competition freaks out. Yesterday was a good example of that. If you were watching La Bernank back-pedal on QG3 (Quantitative Guessing III) real-time, you knew exactly what to do. Buy US Dollars, Short Euros, and cut your gross (and/or net) exposure to US and European Equities.

Or at least that’s what I did.

No, that’s not being overly “confident.” It’s called seeing the play develop and capitalizing on it. I’m not sure if it’s this industry’s very low expectations of sell side research or whether it’s just easier to universally accept mediocrity in “not being able to time markets”, but whatever it is, I like it. Championship teams have championship processes. They make calls when calls need to be made.

That’s just modern day risk management with a Global Macro overlay. Measuring political timing, as Canadian Prime Minister Elliott Trudeau once said, “is the essential ingredient of politics.”

Timmy Geithner’s message on timing yesterday was that there is “no way to give Congress more time.” Really Timmy? Thanks – we appreciate the fear-mongering about a debt position you’ve spent 47% of your born life helping create.

Assuming America’s political panderers abide by Geithner’s timing signal, you can bet your Madoff that this weekend sees an acute level of Congressional respect paid toward their own career risk management.

Rather than waking up to these embarrassingly timed notes out of Moody’s and S&P on US credit risk, what if you wake up on Monday to the thundering Squirrel taking a victory lap on a debt-ceiling compromise?

Perversely, that could be bad for stocks – in the very immediate-term. Why? Because that’s both US Dollar and US Treasury Bond bullish! In the long-run, that’s what America needs – a strong US Dollar, as opposed to a debauched one; a confident leadership-line drawn in the sand, as opposed to a politically obfuscated one; and a progressive American resolve, as opposed to a backward looking one.

Back to the Global Macro Grind…

- I am long the US Dollar (UUP)

- I am short the Euro (FXE)

- I am Canadian

If you can’t have any fun with this game, don’t play it. Or at least we recommend not playing it against us. Hedgeye likes to stir the pot. And in case you missed our notes earlier this week on China – Big Alberta and his Chinese Cowboys in the Haven have brought out the mandarin ladle.

Despite La Bernank sending US stocks lower for the 4th day in the last 5, Chinese stocks closed up another 0.35% last night (they were UP for the 4th day out of the last 5). Good timing.

Meanwhile, European stocks are sucking on a Europig’s nipple this morning hoping that the rest of the real-time risk managing world doesn’t realize that the European Bank “Stress Test” Part Deux isn’t a joke. Hope, and “stress testing” banks using their 2010 numbers, is not a risk management process.

In terms of European positioning:

- I sold my Sweden (EWD) yesterday because we don’t like/trust their banks’ exposures

- I am long Germany (EWG), and I’m worried about it

- I am short Italy (EWI), and I like it

Conan O’Brian said that “early on, they were timing my contract with an egg timer.” And that sounds just about right in terms of the shortest of short-term durations that we’re talking about when we consider these Eurocrat and Congress market catalysts…

But, when Measuring Time in macro market moves, you have to be Duration Agnostic. Market catalysts can be short and/or long term in nature. Mr Macro Market doesn’t particularly care about our individual investment styles or durations.

I’ll walk through how we Measure Time with our all-star Global Macro team of analysts on a conference call at 11AM EST this morning. This is our Q3 Macro Themes call, and we’re right fired up to grind through it and get to the best part of the game – your Q&A session. Please send an email to our Sales Deck (sales@hedgeye.com) if you need call-in info.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1542-1606, $94.68-97.34, and 1299-1318, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer