Buying PENN for a TRADE in the Hedgeye virtual portfolio.

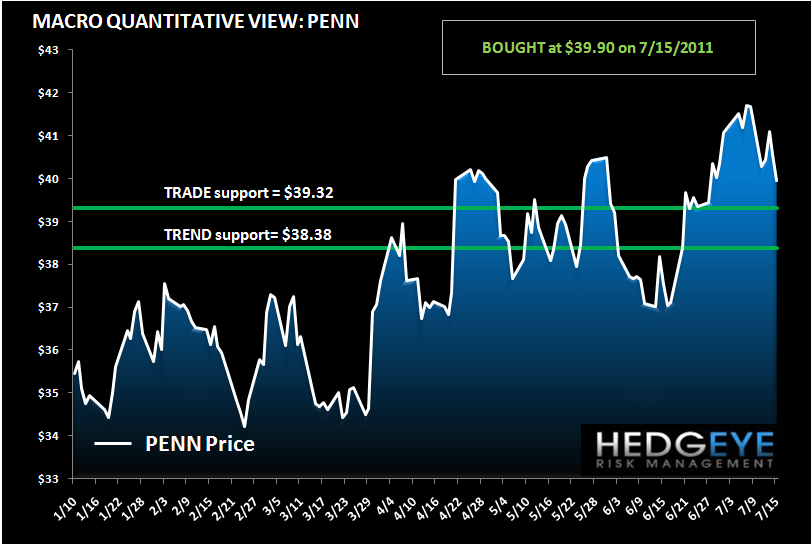

Keith bought PENN in the virtual portfolio ahead of its earnings report this coming Thursday. According to his model, there is good support around $38-39 level. As we wrote in “PENN: 5X WOULD BE A TREND” (7/14/2011), we believe PENN will come in ahead of the street on Q2 EBITDA, revenues, and EPS. Market share gains, outstanding WV table revenues, and property-level margin improvements should drive a Q2 beat.

Friday’s price weakness can be attributed to an analyst downgrade. The gist of the downgrade was concerns of tougher comps in the 2H of 2011 when the onset of table games in WV and PA anniversaries. Not exactly groundbreaking analysis. Here is the chart.