TODAY’S S&P 500 SET-UP - July 15, 2011

Our Q3 Macro Themes call is at 11AM EST today – ping me if you still need the dial in info. Our presentation of European debt maturities might grab your attention. As we look at today’s set up for the S&P 500, the range is 19 points or -0.75% downside to 1318 and 0.70% upside to 1318.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1732 (-2696)

- VOLUME: NYSE 925.21 (4.71%)

- VIX: 20.80 +4.47% YTD PERFORMANCE: +17.18%

- SPX PUT/CALL RATIO: 2.0 from 1.86 (7.89%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 24.47

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.98 from 2.92

- YIELD CURVE: 2.60 from 2.55

MACRO DATA POINTS:

- 8:30 a.m.: Consumer Price Index, M/m est. (-0.1%), prior 0.2%

- 8:30 a.m.: Empire Manufacturing, est. 5, prior (-7.79)

- 9:15 a.m.: Industrial production, est. 0.3%, prior 0.1%

- 9:15 a.m.: Capacity utilization, est. 76.9%, prior 76.7%

- 9:55 a.m.: UMich Confidence, est. 72.0, priopr 71.5

- 1 p.m.: Baker Hughes Rig Count

WHAT TO WATCH:

- President Barack Obama told congressional leaders to report to him within two days on what debt-limit options members can support after yesterday’s talks

- Treasury Secretary Timothy Geithner warned there’s no possible extension to time limit to raise debt ceiling as S&P joined Moody’s in reviewing U.S.’s top credit rating

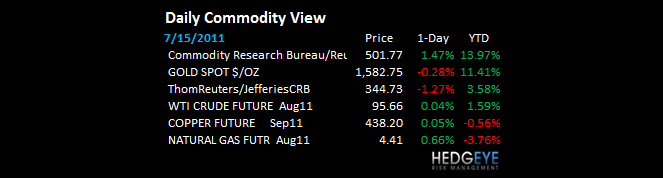

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Pizza Demand in Asia Boosts U.S. Cheese Exports to Record, Kraft’s Costs

- BHP Agrees to Buy Petrohawk for $12.1 Billion in Cash to Add Natural Gas

- Crude Heads for First Weekly Decline in Three Weeks on U.S. Debt Concern

- Gold Falls, Paring Weekly Advance, as Rally to Record Price Spurs Selling

- Wheat Slides for a Second Day as Importers May Favor Russia Over U.S., EU

- LME Doubles Minimum Delivery Rates for Warehouses Holding the Most Metal

- Rice Exports From Vietnam May Beat Target on Bigger Harvests, New Markets

- Copper May Gain on Reports Predicted to Show Stronger U.S. Manufacturing

- Sugar Drops as Banking Stress Tests Weigh on Commodities; Cocoa Declines

- China Is Tightening Rare-Earth Access Even as Sale Quotas Climb, EU Says

- Glut of Natural Gas Produces Record U.S. Exports to Mexico: Energy Markets

- Beef Contamination Spreads in Japan as Fukushima Radiation Taints Straw

- Wheat Exports From Australia Climb as China Boosts Purchases After Drought

- Oil May Advance Next Week on Speculation About Fed Stimulus, Survey Shows

CURRENCIES

EUROPEAN MARKETS

- EUROPE: plain ugly TRENDs continue to develop with Italy in crash mode (down -20% since February) and Greece is gone (down -31% since February)

ASIAN MARKETS

- ASIA: solid is as solid does; China up for the 4th day in 5 (were long $CAF) and the rest of region continues to shape up (Korea, Indonesia)

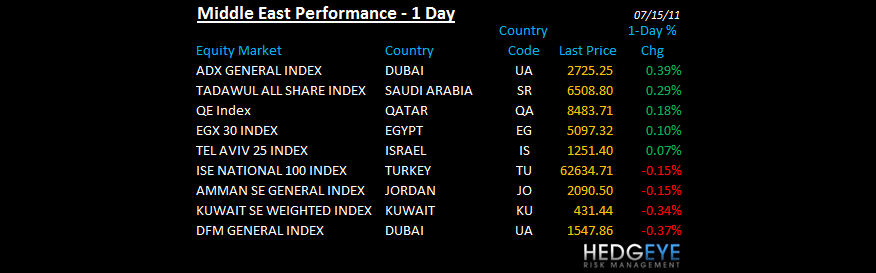

MIDDLE EAST

Howard Penney

Managing Director