TODAY’S S&P 500 SET-UP - July 12, 2011

If there's going to be a capitulation day this week, this should be it. Alternatively, if Global Equity markets and European CDS don't arrest these abrupt moves soon, world markets are going to have a big problem. As we look at today’s set up for the S&P 500, the range is 39 points or -1.70% downside to 1297 and 0.64% upside to 1328.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -2168 (-996)

- VOLUME: NYSE 829.43 (+7.56%)

- VIX: 18.39 +15.30 YTD PERFORMANCE: +3.61%

- SPX PUT/CALL RATIO: 2.88 from 1.65 (+74.71%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.57

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 2.94 from 3.03

- YIELD CURVE: 2.57 from 2.63

MACRO DATA POINTS:

- 7:30 a.m.: NFIB Small Business Optimism, est. 91.2, prior 90.9

- 8:30 a.m.: Trade balance, est. (-$44.1b)

- 8:30 a.m.: USDA WASDE report

- 10 a.m.: IBD/TIPP economic optimism, est. 43.9, prior 44.6

- 10 a.m.: JOLTs job openings

- 11:30 a.m.: U.S. to sell $28b in 4-wk bills

- 12 p.m.: EIA short-term energy outlook

- 1 p.m.: U.S. to sell $32b in 3-yr notes

- 2 p.m.: Fed releases minutes from June 21-22 FOMC meeting

- 4:30 p.m.: API weekly inventories

WHAT TO WATCH:

- The Fed is scheduled to release minutes from the June 21-22 FOMC meeting at 2 p.m.

- European finance ministers meet again today with plans to respond to release of bank stress tests later this week

- Italian 10-yr yield rises above 6% for first time since 1997

- President Barack Obama said to reject Republicans scaled- down deficit deal yesterday; talks continue today

- Alcoa (AA) 2Q EPS cont ops 32c vs est. 33c

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Crude Oil Falls for a Third Day on European Debt Concern, U.S. Stockpiles

- Gold Declines for First Day in Seven as Europe’s Debt Crisis Lifts Dollar

- Copper Drops for a Third Day as Europe’s Sovereign-Debt Crisis May Broaden

- ‘Double Eagle’ Gold Coin Dispute Harkens Back to Last U.S. Default in 1933

- Cotton Falls to Nine-Month Low on China Demand Concern, Dollar’s Advance

- Coffee Declines Amid European Sovereign-Debt Crisis Concern; Sugar Falls

- Wheat Falls for a Second Day as ‘Risk-off Mood’ Engulfs Financial Markets

- Rubber Drops for Fourth Day as European Debt Crisis Escalates, Oil Slumps

- Cocoa Seen Advancing to New Highs on Africa-Indonesia Fix: Freight Markets

- Oil Rebound Pushes Yields Lower Ahead of Record Debt Sale: Russia Credit

- Zambia’s Copper Poised for Global Top 5 as Government Lures Vale, Vedanta

- Corn, Soybean Cash Premiums Advance on Reduced U.S. Sales, Hot Weathert

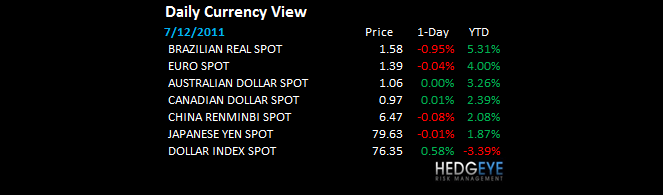

CURRENCIES

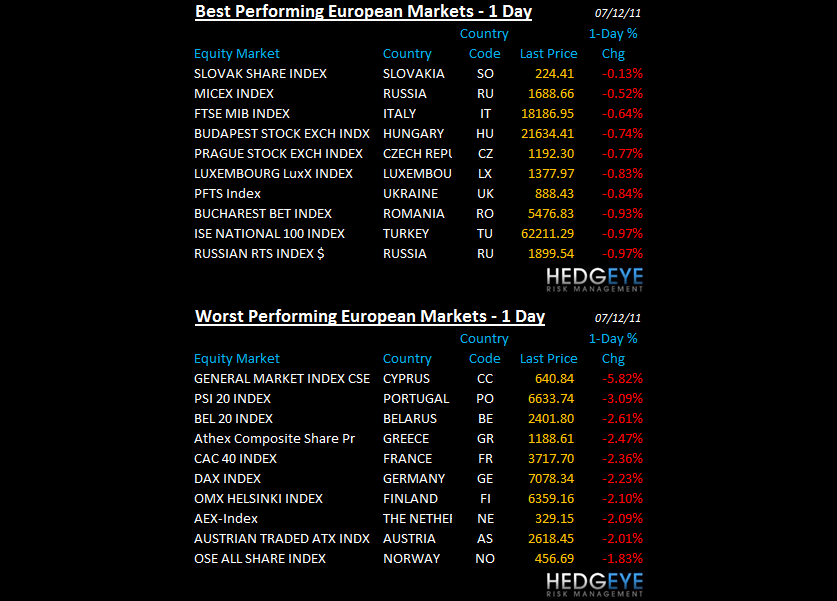

EUROPEAN MARKETS

- EUROPE: oversold, but this is a bloody mess; Greece is crashing (down 31% since FEB making new YTD lows); Italians just making stuff up

ASIAN MARKETS

- ASIA: worst day in 3 weeks; every market that matters = straight down; HK -3.1%, KOSPI -2.2%, India -1.8%, China -1.7%, Japan -1.4%

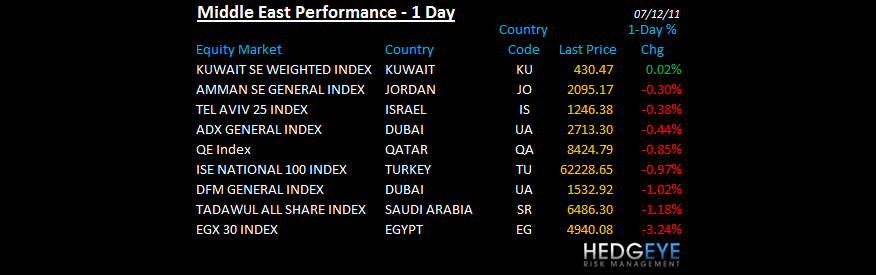

MIDDLE EAST

Howard Penney

Managing Director