“Yet for all its conflict and complexity, there has often been a “oneness” to the story of oil, a contemporary feel even to events that happened long ago and, simultaneously, profound echoes of the past in current and recent events.”

- Daniel Yergin, The Prize

Post World War II, global production of oil surged from 9 million barrels per day in 1945 to 40 million barrels per day in 1970. Saudi Arabia and Iran were eager to monetize their vast resource potential – “Nobody could have lifted enough crude to satisfy all the governments in the Persian Gulf during this period,” said George Parkhurst of Standard Oil of California. A wave of Soviet Union exports flooded the market; US Senator Kenneth Keating remarked, “It is now becoming increasingly evident that [Khrushchev] would also like to drown us in a sea of oil if we let him get away with it.” In 1956, major oil companies struck oil in Algeria and Nigeria. And in 1959 Standard Oil of New Jersey “hit the jack-pot” at the Zelten field in Libya.

Consequently, the real price of oil sank 40 percent between 1960 and 1969. Howard Page, Middle East Coordinator for Standard New Jersey said of the glut, “Oil was available for anybody, anytime, any place and always at a price as low as you were charging for it.”

In the late 1950s, President Eisenhower found himself in a precarious position. Though the US was still the world’s largest oil producer, the plethora of cheap, foreign barrels encroached on the competitiveness of domestic, independent producers. Oil imports rose from 15 percent of the domestic production equivalent to 19 percent between 1954 and 1957 alone.

Congress urged Eisenhower, who morally opposed protectionism, to curb imports. One geologist wrote to then-Senator Lyndon Johnson, “no sense in bankrupting every independent oil man in Texas for a few Arabian princes.” Eisenhower resisted and criticized the “tendencies of special interests in the United States” that were “in conflict with the basic requirement on the United States to promote increased trade around the world.” Begrudgingly, however, Ike caved, and on March 10, 1959 he signed into law a mandatory quota on imported oil equal to 9 percent of domestic consumption.

Eighteen months later, representatives from Saudi Arabia, Venezuela, Kuwait, Iraq, and Iran gathered in Baghdad. The Organization of Petroleum Exporting Countries – OPEC – was established. Market intervention certainly has its unintended consequences. While I don’t assert that Eisenhower’s import quota was the sole motivating factor for OPEC’s birth or that OPEC would not exist absent the policy, it was of considerable influence. In fact, Daniel Yergin, Pulitzer Prize winning author of The Prize: the Epic Quest for Oil, Money, and Power, called Eisenhower’s import controls “the single most important and influential American energy policy in the postwar years.”

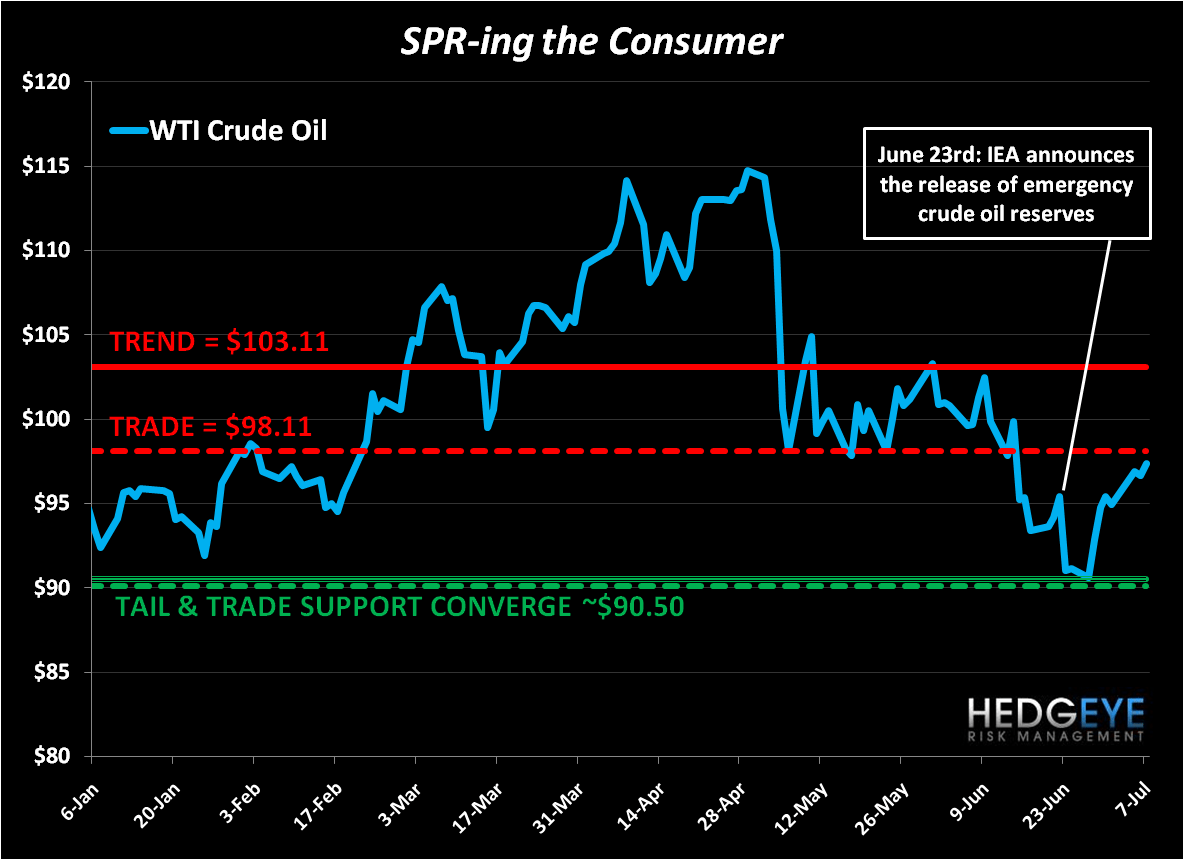

“Profound echoes of the past” resonate in President Obama’s June 23rd decision to release 30 million barrels from the US’s Strategic Petroleum Reserve (SPR). The attempted market intervention was (allegedly) prompted by the loss of Libyan supply and OPEC’s failure to officially raise production quotas in its most recent meeting. Even though the contentious OPEC meeting failed to quell the IEA’s supply concerns, the Saudis were explicit in their intention to raise production by 1.5 million barrels per day regardless of the Iranian-lead OPEC decision – more than enough to replace the lost Libyan output.

Market participants quickly called out the IEA action for what it was: a haphazard attempt at price manipulation as global growth slows; after all, the agency’s press release stated: “Greater tightness in the oil market threatens to undermine the fragile global economic recovery.” Thus, while Eisenhower sought higher oil prices to protect US producers from the actions of oil exporters, Obama seeks lower oil prices to shield US consumers from the same foes.

Geopolitical tensions in the Middle East have, of course, put a premium on crude oil; Brent – the world’s light, sweet benchmark grade – rallied from $102 per barrel to $114 per barrel in February alone. But mention of US monetary policy is warranted in the oil price discussion. After the Fed announced QE2 in late August 2010, oil prices moved 20% higher before you ever “Googled” a map of Tunisia. The excessive liquidity injected into financial markets via the Fed’s bond-buying programs spurred investment into real assets, particularly across the commodity complex.

And while Fed Chairman Ben Bernanke often cites stock market appreciation as evidence of QE’s success, he attributes commodity price inflation merely to “transitory” supply and demand fundamentals. It would take a previously unforeseen level of accountability for Bernanke to admit that his policies are in part responsible for higher food and energy costs, while wages and employment are “frustratingly” stagnant.

In his semiannual report to Congress on monetary policy earlier this year, Bernanke commented on rising oil prices: “We will continue to monitor these developments closely and are prepared to respond as necessary to best support the ongoing recovery in a context of price stability." The traditional tools of monetary policy are interest rates, the monetary base, and reserve requirements; but does the Fed now sell oil too? While Bernanke was likely consulted, no, he didn’t make that call. Still, the Fed’s bond-buying program ended on June 30th and the US Department of Energy (DOE) was auctioning off emergency crude reserves the very next day. Next up: the USDA will be planting corn in our national parks…

But what has been the impact of the SPR release thus far? Well, Brent plummeted from $114 to $105 within two days of the announcement, though quickly recovered all of that loss. The Brent futures curve went into contango for the blink of an eye before returning to backwardation. The RBOB gasoline futures curve never budged and the front-month contract is now trading above its pre-SPR release price. In the immediate-term, the oil market intervention did very little; on a longer duration, the IEA may have sparked the next leg up in the commodity.

Most notably, the IEA’s decision to release reserves after the Saudis announced their intention to fill the Libyan supply shortfall calls into serious question Saudi Arabia’s spare capacity and oil quality. Not only that, but eventually the IEA will have to enter the market as a buyer to refill the reserves; oil is not as easily produced as fiat currencies. And the fact that the SPR auction was “substantially oversubscribed,” according to the DOE, does not suggest that the world’s largest energy companies believe oil prices are heading lower.

Government intervention in free markets often has unintended consequences, and, as a result, in the long-run consumers will realize an undesired outcome: higher oil prices. For the only lasting impact that the IEA’s reserve release will have is that the agency’s greatest worry – inadequate supply – is more of a reality than the market previously thought.

The chart below outlines our TRADE (3 weeks or less), TREND (3 months or more), and TAIL (3 years or less) quantitative setup for WTI crude oil. We will manage risk around these levels as government intervention inspires increased price volatility. We are currently short oil in our Virtual Portfolio as it is immediate-term TRADE overbought.

Our immediate-term support and resistance levels for oil, gold, and the SP500 are now $90.51-98.11, $1, and 1, respectively.

Kevin Kaiser

Analyst