At the beginning of the year, I laid out my coffee strategy: long SBUX and PEET; short GMCR. OK, so I’m 2 for 3, but the miss on GMCR was a big miss.

Back on 2/15/11, I posted a note titled “WHY SBUX SHOULD BUY PEET”. I said that “PEET’s is one of the best positioned, small-cap growth names in the restaurants/coffee space. Unfortunately, the surge in coffee prices is an overhang, but not a deal-breaker to the growth story. We would use any commodity concern-induced dips as an entry point.”

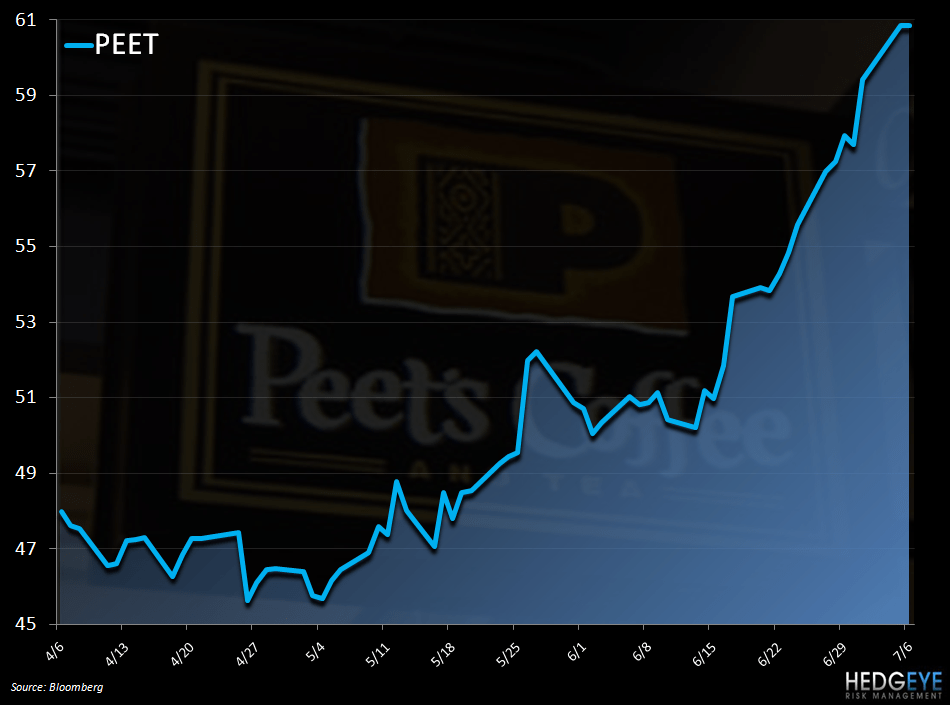

Year-to date PEET’s is up 45.3% and now trades at 15.6x EV/EBITDA, which represents a nice premium to the QSR group at 13.3x. At best there is $3 or 6% up side from here. There is some logic that now suggests that suggests that KFT is perhaps best-suited to acquire PEET, although SBUX remains a potential candidate.

Here is the Mosaic theory behind the rational for KFT to buy PEET’s:

1. The coffee category is a very important for KFT and losing the SBUX business is big blow. To date, KFT has yet to articulate a strategy to replace the lost SBUX business. Late last month, KFT said it would delay the launch of Gevalia coffee in U.S. retail stores by five months until January citing “robust demand that raised supply concerns.”

Hedgeye - What if they are rethinking the coffee strategy and questioning what might be the best solution? Gevalia could be great brand but, the Peet’s brand has real appeal on the West Coast and a growing presence in the East.

2. Shareholders of KFT don’t like the idea of the plan to replace Starbucks with Gevalia. In short, it’s too costly and risky. The analyst community has already factored in a loss of the SBUX business and upfront costs behind the investments in Gevalia.

Hedgeye - the unwinding of the investment in Gevalia in favor of an accretive acquisition of a strong brand and could add between $0.05-0.10 to KFT EPS.

3. Perhaps not coincidentally, the Gevalia delay comes days after Trian (Nelson Peltz) announced a stake in KFT. Also, Trian is a top ten shareholder in PEET and has history of buying KFT and strong arming buys of existing holdings. Think Cadbury!

Hedgeye - no comment.

4. KFT wants to reinvest the $750mm from SBUX in the coffee category.

Hedgeye - Trading out the Starbucks brand for Peet’s is the best use of cash for KFT shareholders.

PEET is great company with one of the better secular growth stories I am aware of. I would not be surprised if the company gets bought out, but current prices suggest that much of that thesis may already be in the stock.

One last thought: the best thing that could happen for the DNKN IPO is a deal in the coffee space!

Howard Penney

Managing Director

Rory Green

Analyst