This note was originally published at 8am on June 30, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“A pessimist sees the difficulty in every opportunity; an optimist sees the opportunity in every difficulty.”

-Winston Churchill

Earlier this week, I appeared on BNN, which is the Canadian equivalent of CNBC to discuss some of our key recent macro thoughts (the clip can be found here: http://watch.bnn.ca/#clip491722 ). Shortly after the appearance, our COO Michael Blum emailed and said I need to smile more. I then was told by one of our top Canadian subscribers that I could use some rose colored glasses. These comments made me wonder: am I too pessimistic? Further, is Hedgeye too pessimistic?

Admittedly, our morning missives at times can come across with a pessimistic tone. This is a function of the early mornings, our legitimate concerns regarding the global economic outlook, and, candidly, some disdain for the decision making and leadership currently coming out of Washington, DC. Now some might argue we could simply ignore Washington, DC, but the reality is that we are in an economic and market environment in which Washington decision making is critical to investment decision making.

Despite our tone in the Early Look some mornings, as a firm I can ensure you we are incredibly optimistic. The simple fact that we started this firm in the middle of 2008 shortly ahead of one of the most dramatic equity sell-offs in our lifetimes is probably the best validation of our optimism. We continue to be optimistic about the future of our business, the businesses of our subscribers, and our collective ability to continue to find interesting and alpha generating investment opportunities. Moreover, we are also optimistic about our ability to help shape and inform economic policy.

We currently share our thoughts and research with decision makers within the Obama administration, with certain Presidential hopefuls, and with members of Congress on both sides of the aisle. Our goal is not to someday become rich selling research to the government, but rather to do our part to get this fine country to a better fiscal, monetary, and economic place by providing input and ideas where we can. While there are certainly economic storm clouds on the horizon, as Churchill said long ago there is “opportunity in every difficulty.”

Currently, the Hedgeye research team sees a number of interesting opportunities on the long side. Below I’ve outlined a number of our team’s top investment ideas that were circulated in May’s version of the Hedgeye Edge on May 27th 2011:

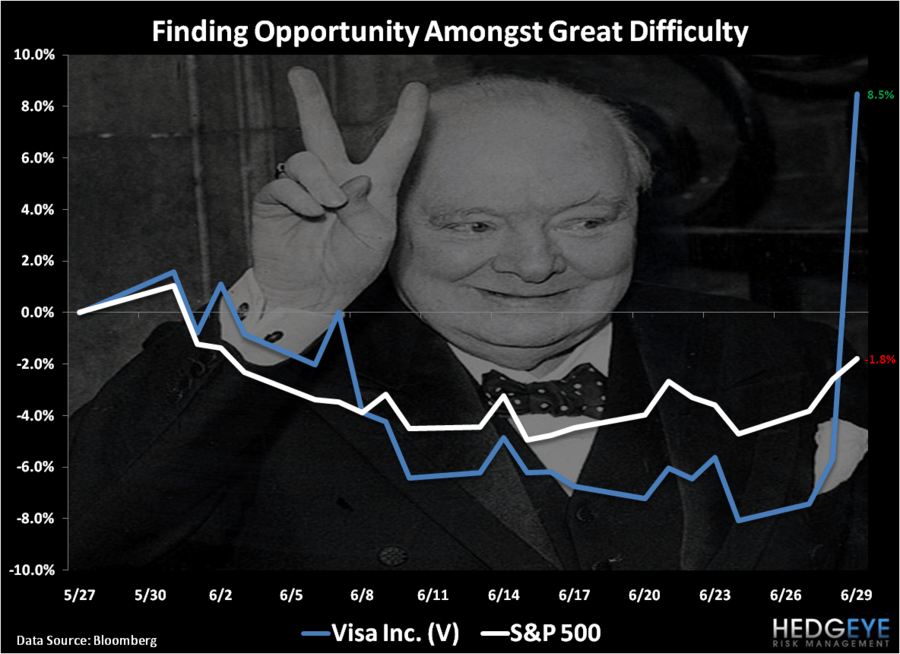

- Visa (V) – We remain strongly of the view that Durbin will be softened, and that this will remove a meaningful source of overhang on the stock. While MasterCard has already had a major run, Visa has lagged considerably behind. Update: Durbin was softened and V is up +8.5% since May 27th.

- Buffalo Wild Wings (BWLD) - The last quarter was very difficult to poke holes in and it remains one of our favorite ideas as its primary food cost, chicken wings remain suppressed. We see sales continuing to accelerate and a focus of management on deploying further cash into the business which should fuel further growth. Update: Chicken costs have remained soft and BWLD is up +5.8% since May 27th.

- Nike (NKE): Over the intermediate and longer terms this is McGough’s favorite big cap long idea. He thinks that it grows from doing $20 billion in sales to $28 billion in 3 years. Update: NKE reported strong earnings earlier this week and is up +6.1% since May 27th.

Since May 27th, the SP500 is down -1.8%, so these ideas did quite well on relative basis. Now to be fair, not all of the ideas in Hedgeye Edge fared this well (and some such as KONA fared much better), but the point is really to emphasize that even when our Macro view can sometimes be pessimistic, our research can still find interesting opportunities on the long side. If you are an institutional subscriber and would like to connect with a Sector Head on these ideas or other stock ideas, please email sales@hedgeye.com.

Today is both quarter end and month end for the investment management community. The SP500 as of the close yesterday is down -2.8% for the month and -1.4% for the quarter, which is depressing even for an Optimistic Pessimist like myself. The end of the quarter also signals the end of the Federal Reserve’s program of Quantitative Easing II, which is certainly a positive for anyone other than those still clinging to the ideology of Keynesian economics.

The key potential impact of the end of QEII is a strengthening U.S. dollar, which will perpetuate the continued deflation of commodity prices. Far be it for me to call out too many positives this morning, but commodity prices deflating will be positive for corporate earnings (eventually) and incrementally positive for consumer spending.

Now as for Standard & Poor’s warning this morning that it will cut the U.S. to its lowest rating of “D” if the government fails to increase the debt limit, I would recommend disregarding Standard & Poor’s with impunity. The 10-year yield for U.S. Treasury is trading at 3.097%, which means that the U.S. is not defaulting on its obligations any time soon. While we may not particularly like the debt ceiling resolution, a default is not imminent.

Our job as market operators is not to be pessimistic, optimistic, bearish, or bullish, but ultimately it is to be right. Trust me, even if we sometimes sound dour, the Hedgeye Research Team is always finding nuggets of optimism somewhere. As the famous Persian proverb goes:

“I had the blues because I had no shoes until upon the street, I met a man who had no feet.”

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research