TODAY’S S&P 500 SET-UP - July 1, 2011

As we look at today’s set up for the S&P 500, the range is 27 points or -2.02% downside to 1294 and 0.03% upside to 1321.

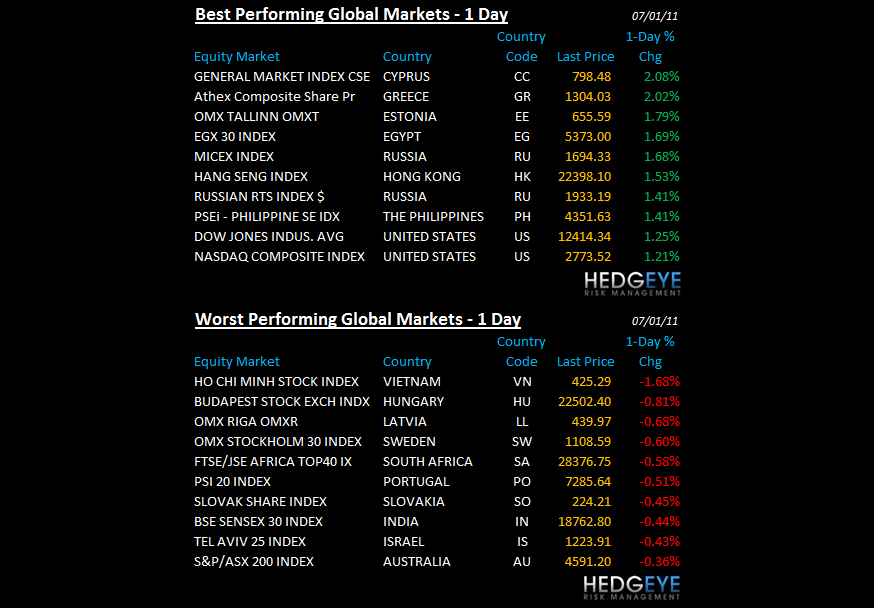

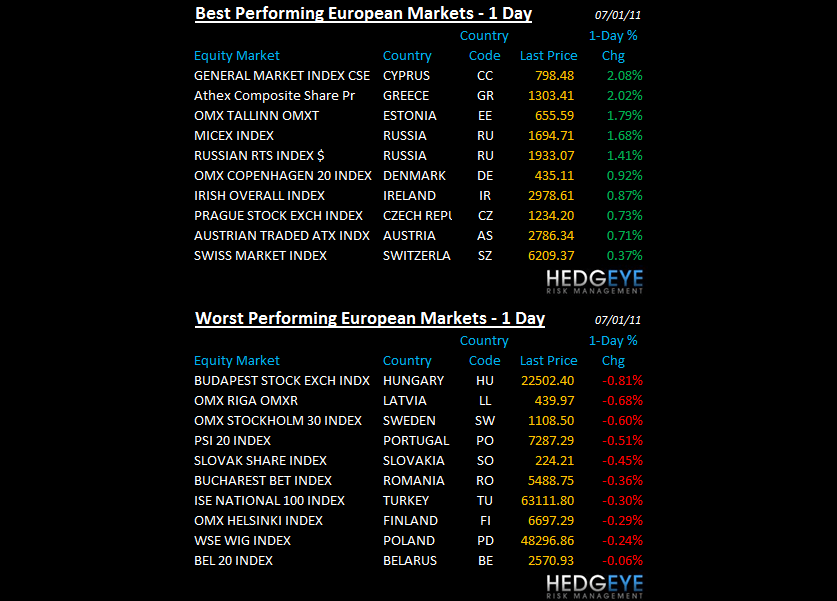

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1398 (+270)

- VOLUME: NYSE 996.05 (+9.10%)

- VIX: 16.52 -4.34% YTD PERFORMANCE: -6.93%

- SPX PUT/CALL RATIO: 1.38 from 1.40 (-1.77%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.05

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 3.18 from 3.14

- YIELD CURVE: 2.73 from 2.67

MACRO DATA POINTS:

- 9:55 a.m.: UMichigan Confidence, June F, est. 72.0, prior 71.8

- 10 a.m.: Construction spending, est. 0.1%, prior 0.4%

- 10 a.m.: ISM Manufacturing, est. 52.0, prior 53.5

- 1 p.m.: Baker Hughes Rig Count

- 2 p.m.: USDA cattle, hog slaughter

WHAT TO WATCH:

- Questions about credibility of accuser in ex-IMF chief Strauss-Kahn’s case said to place it in jeopardy

- NBA becomes second U.S. sports league to lock out players

- Treasury Secretary Geithner’s potential departure from the administration would force President Obama to assemble a new economic team as the 2012 election looms, with jobs a top voter concern.

- Senate in session, House in recess

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- China May Buy U.S. Corn as Price Slumps 11% on Acreage: Chart of the Day

- Corn Extends Worst Monthly Loss Since 2008, Wheat Drops as Food Costs Ease

- Commodity-Futures Trade in China Plunges 30% as Rules Restrain Speculation

- Oil Drops on Signs of China, U.S. Slowdown; IEA and OPEC Supplies Increase

- Gold Falls to Six-Week Low Amid Reduced Concern Greece May Default on Debt

- Coffee Falls on Signs of Limited Frost Damage in Brazil; Cocoa Retreats

- Copper Erases Drop on London Metal Exchange, Trades at $9,445 a Metric Ton

- U.K. Crop Losses Narrow as Rain Last Month Follows Driest Spring on Record

- Rice Output in Indonesia May Climb on Increased Planting, Reducing Imports

- Lead-Battery Production in China Seen Dropping by Half on Pollution Rules

- Muddy Waters Is Looking at More ‘Suspicious’ Chinese Companies, Block Says

- Brent to Recover From Decline as Supply Boost Seen Failing: Energy Markets

- Philippine Investment Push Lures Sumitomo as Aquino Plans Roads, Airports

- Gold May Gain Next Week as Slowing Economies Stoke Demand, Survey Shows

CURRENCIES

EUROPEAN MARKETS

- European equity markets trade mixed.

- Jun final Manufacturing PMI; France 52.5 vs preliminary 52.5; Germany 54.6 vs preliminary 54.9

- EuroZone 52.0 vs preliminary 52.0

- UK Jun Manufacturing PMI 51.3 vs consensus 52.1, prior revised 52.0 from 52.1

ASIAN MARKETS

- Asian market are generally higher..

MIDDLE EAST

Howard Penney

Managing Director