Positions in Europe: Long Germany (EWG); Short Spain (EWP)

The Finance Ministry in Athens is on fire, what’s next?

As we mentioned in our research earlier in the week, we believe the backing for PM Papandreou’s PASOK party in the confidence vote last Tuesday was THE critical hurdle to clear to pass the government’s newest €78 Billion austerity package. The probability of its passage was also largely confirmed by the strong performance of European equity markets over the last two days and gains in the EUR-USD cross. However, we warn that Troika’s (EU, ECB, IMF) desire to avoid a strict restructuring of Greek debt in favor of near-term bailout band-aids and debt concessions will only extend the country’s larger fiscal imbalances, and therefore downside uncertainty for those institutions and investors holding Greek debt.

Today’s vote to pass austerity opens the door widely for similar approval of a second bill tomorrow that authorizes implementation of the measures. Critically, the passage assures Greece receives its next bailout tranche of €12 Billion from the IMF on July 3rd (from its first bailout of €110 Billion in May 2010), as the Greek government has stated that it only has funds until mid-July to support government salaries, pensions, and maturing debt obligations. In the chart below we show the monthly principal and interest payments over the next months. Further, passage assures the ball will be put in motion for talks on a second bailout worth an estimated €70-120 Billion. Such discussion will take place at the next EU Finance Ministers’ Meeting on July 5-6th and 11-12th.

But to what end with these bailout and austerity packages?

We’re less than optimistic that austerity will have much impact on the country’s fiscal imbalances and that the devil is in the details. Of the planned €28 Billion of spending cuts and tax hikes and €50 billion of private assets sales through 2015, Greece may be able to reach a deal that broadly agrees with Troika’s deficit reduction demands, while specific terms of the deal are back-loaded towards 2014/15.

While this is only a hypothetical, such a tactic could be used to appease both Troika and the Greek populous. But ultimately it bodes poorly for any material change in the budget debt and deficit, but then again given Greece’s poor prospects to grow any revenue with such a deflated growth profile (GDP contracted -4.4% in 2010 and is forecast to fall -3.8% this year), using smoke and mirrors by either party to reach any form of intermediate support should come as no great surprise.

Further, subsidizing Greece extends the uncertainty of all banks, central banks and private individuals, which hold nearly half a trillion dollars (or €340 Billion) of Greek debt. France has floated the idea of French banks reinvesting 70% of their maturing debt Greek bonds, with 50% allocated to new Greek debt that would be maturing in 5 years to be rolled over to a maturity of 30 years and another 20% directed to a zero coupon fund of “high quality securities”. The Germans have also floated similar ideas in response (meetings being held today), yet clearly there are numerous unknowns surrounding this proposal, including interest rates on the debt, and ultimately where this Greek soap opera will take us over the next month, quarter, and years ahead.

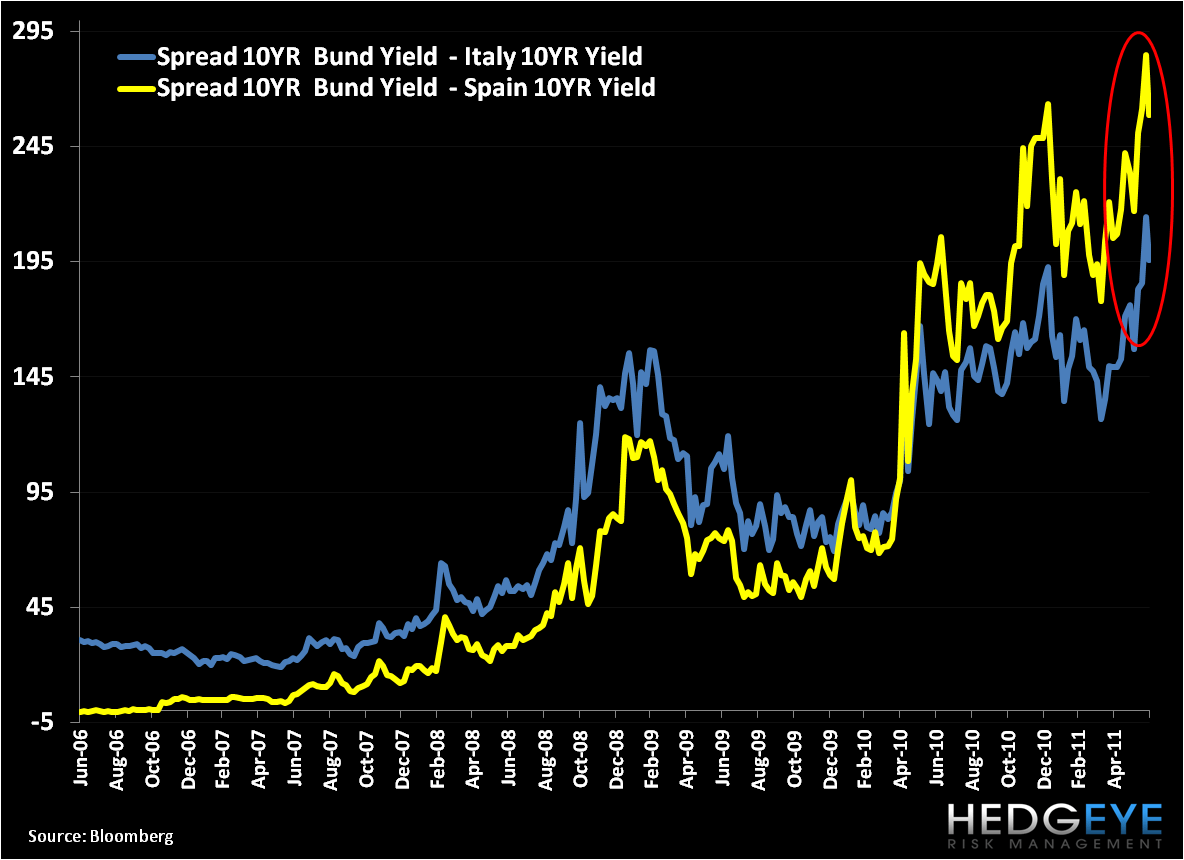

While we worry about Greece, we’re equally concerned about rising risk premiums across the rest of the periphery, especially for Italy and Spain, two countries with outsized government debts, and much larger GDPs (and exposure to throughout European institutions) than Greece, Portugal, or Ireland.

Interestingly the spread of 10 government yields from Italy and Spain over German bunds has reached record highs over the last days, a flag to monitor as the media is focused squarely on Greece.

A second chart to note is the CHF-USD cross which continues to make higher highs. Here we’ve pulled the chart back 10 years to show this serious move. We recommended a long position in the pair on 6/2/2011 and continue to support that view as the uncertainty in European sovereign debt contagion sees no end in sight.

Regarding the EUR-USD cross, we expect the pair to trade in a tight band between $1.41 and $1.45, largely supported by Troika’s backstop to prevent default of any Eurozone member nations and weakness in the USD vis-à-vis political indecision on the US debt ceiling debate.

Matthew Hedrick

Analyst