Here is a comprehensive view of top line trends in the QSR category heading into earnings season. Commodity costs are elevated; investors get that. How companies handle that and maintain comps will be the key differentiator over the balance of the year.

In the quick service space, traffic has been the prize operators have aimed for over the past number of years. Some, like CMG, have had tremendous success in driving guest counts while others, like WEN, have struggled in that regard over the last couple of years. Below, we go through several key names in the QSR space in terms of where they stand from a comparable sales growth perspective as we roll towards earnings season kicking off.

CMG

Chipotle has blown away expectations for a number of quarters now. Management struck a more cautious tone on the most recent earnings conference call of February 20th, but the company is likely to report another solid quarter of comparable restaurant sales growth on July 19th. Over the past three quarters, the company has produced double-digit comp growth. The concept has been wildly popular but, expectations surrounding top line growth have moderated somewhat. During the first quarter, CMG comparable restaurant sales grew 12.4% (11.4% excluding the impact of a BOGO promotion). This represented an acceleration in two-year average trends of 105 basis points (55 basis points excluding the impact of the BOGO promotion). Despite this robust growth, restaurant-level margins contracted in 2Q which has led management to make the decision to raise prices further. Labor pressure related to the federal immigration authorities’ probes into CMG’s hiring practices has also impacted margins.

In light of the strong performance during 1Q, management raised its guidance for comp growth from low single-digit to mid-single digit. On the February 20th earnings call, management said that it would hold off any further increase in price until the third quarter to properly assess food inflation and the reaction of its customers, particularly in California, to prior price increases. News emerged over the past few days that the company has raised prices $0.50 at its New York chains, with lines (according to the Wall Street Journal, still “out the door”) and plans to raise prices in the next few weeks at its stores in the Northeast and Southeast, with changes in other markets to follow.

While New York City’s customers may absorb the price increase with little impact on frequency of visits, it remains to be seen if the broader store base will react in a similar manner. The company needs to maintain transaction counts to meet investor expectations in the back half of the year.

Hedgeye: CMG is going to once again post a strong quarter.

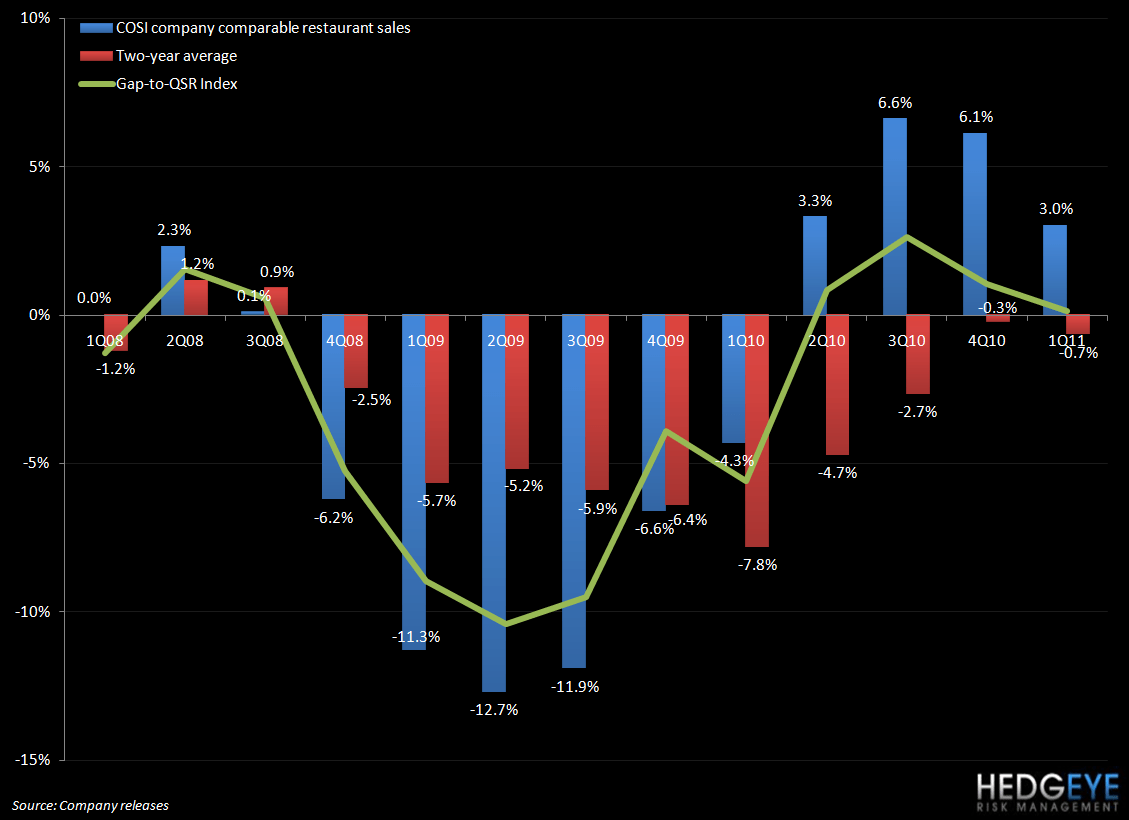

COSI

I continue to believe that the COSI turnaround story is on track, despite what the weakness in the stock, of late, might be suggesting. In 1Q11 COSI reported a 3% in same-store sales, implying that 2-year trends declined from a -0.3% to -0.7%. All of our visits and checks suggest that the company can post 3-4% same store sales in 2Q11.

Hedgeye: COSI (the stock) has struggled of late, but the sales trends are telling a different story. I believe there will be incremental positive news when the company reports the quarter.

DPZ

Domino’s Pizza’s management team has carried out an impressive turnaround over the past 18 months. The introduction of a new pizza was well-received in early 2010, with a massive increase in comparable restaurant sales growth coinciding with the new product and the accompanying advertising campaign. The company has remained focused on driving comp growth by other initiatives also. For instance, the company has rolled out an impressive online ordering system that accounted for 25% of sales in the first quarter, according to the most recent earnings call.

Hedgeye: Management is guiding to domestic company comparable-restaurant sales of +1 to +3%. The mid-point of this range implies two-year average trends of 5.2%, a sequential deceleration of 105 bps from 1Q11. All indication are that DPZ will meet or exceed current guidance.

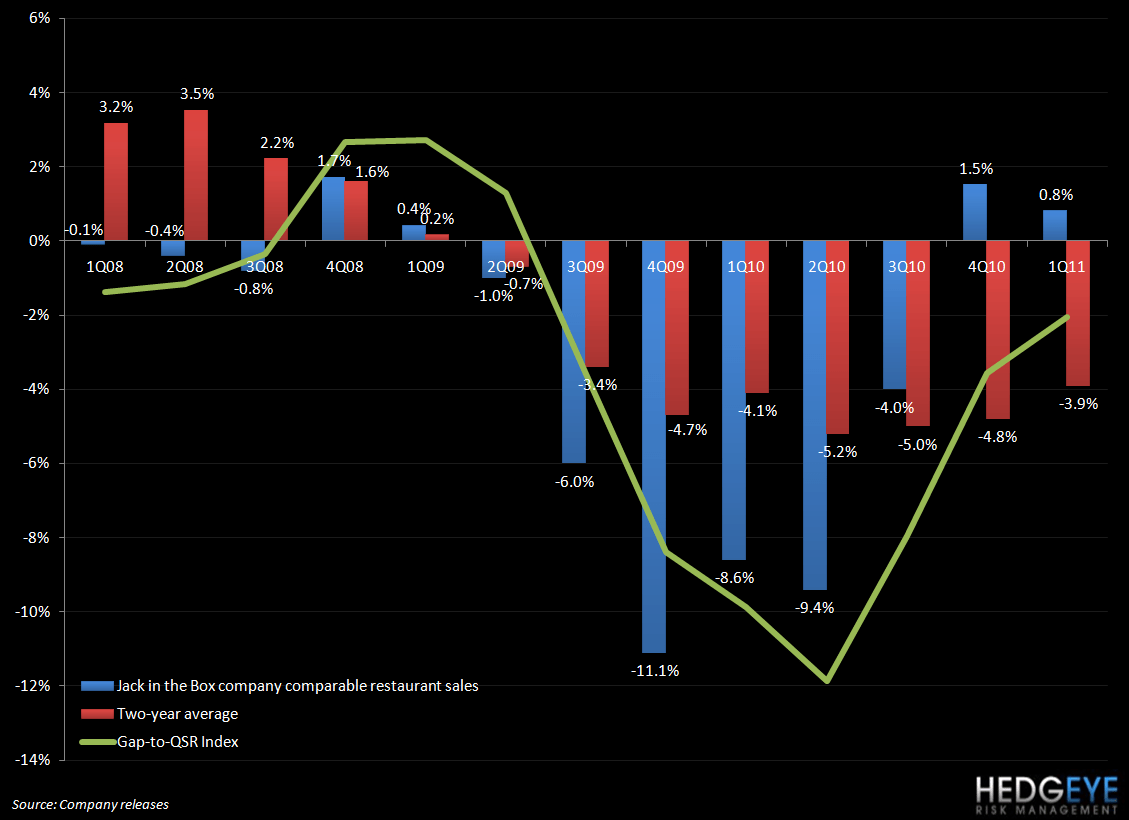

JACK

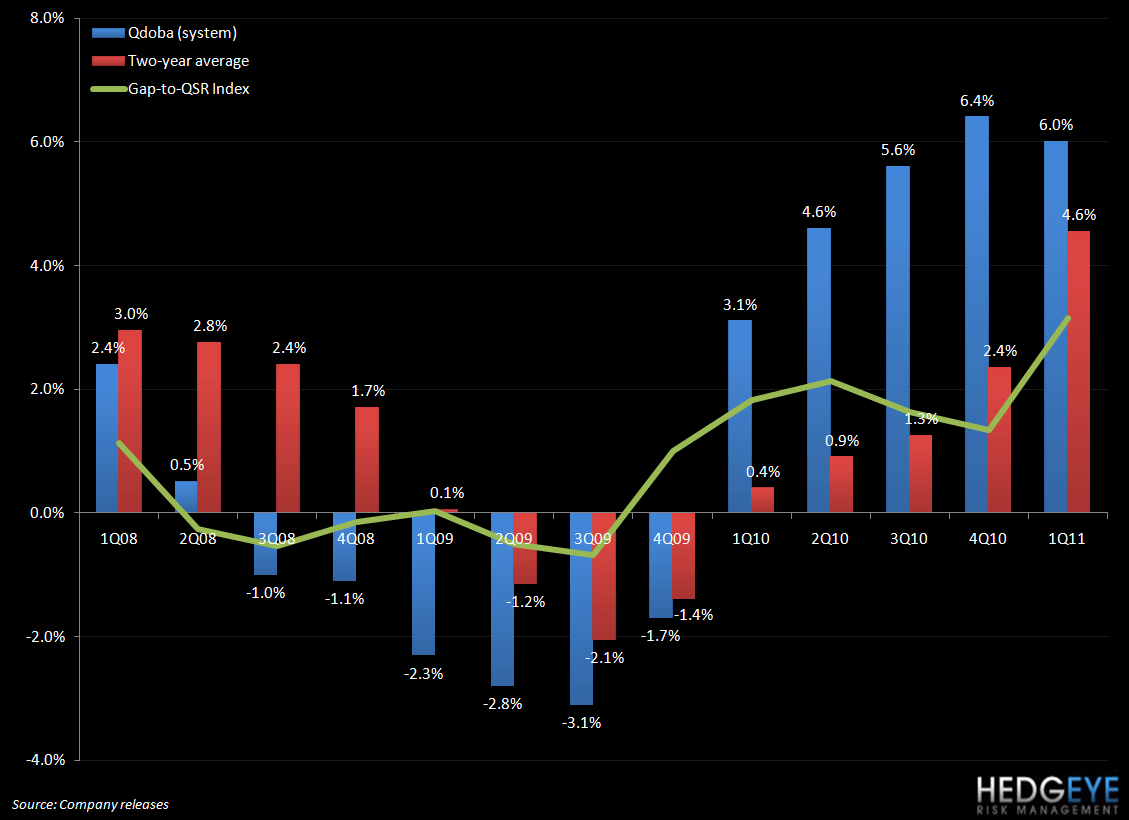

Jack in the Box has seen comparable restaurant sales recover over the last couple of quarters but lags the QSR group on this metric. Management is guiding to what I believe is an achievable range of +2 to 4% comparable restaurant sales growth during the third quarter. The mid-point of this range implies two-year average trends of -3.2%, a sequential acceleration of 70 basis points. I believe that this is within reach for Jack in the Box. The mid-point of management’s guidance range for Qdoba comparable restaurant sales, of +4 to 6%, would represent a sequential acceleration in two-year average trends of 20 basis points to +4.8%.

California and Texas have been soft markets for JACK over the past couple of years but, encouragingly, that there has been a recent bounce-back in comps in both markets. In fact, according to management commentary during the most recent earnings call, “California and Texas both continue to have positive same-store sales and California was our best performing market on a two-year basis.” Together, the Lone Star and Golden states make up 57% of the company’s total store base.

Hedgeye: Given the improving MACRO environment JACK has a chance to beat consensus environment.

MCD

MCD sales have been strong thus far this year but, as we highlighted in our “MCD – HORSESHOES AND HANDGRENADES” on June 8th, the change of tone between the April and May press releases was telling. April’s U.S. results were, according to the company, driven by McCafé, beverages, breakfast, and featured core products. May’s U.S. sales commentary, however, did not mention core products or McCafé.

The crux of my bearish thesis on MCD, that originated in the latter stages of 2010 and was published in a black book in mid-January, was that McDonald’s has become over-dependent on beverages to drive sales. The risk to this strategy, as I see it, is that it is not sustainable and I expect to see MCD struggle to match the beverage sales of 2010 this year. With any drink for $1 at MCD this summer, it seems that management is maintaining its loyalty to the idea of driving guest counts but average check is likely to suffer and my bottom line, that MCD’s core business is declining, remains intact. My view here is specific to MCD’s domestic business which accounts for ~46% of the company’s overall operating income.

Hedgeye: It appears the MCD is having a strong June in the U.S., which could imply acceleration in 2-year trends. With 2Q11 sales trends likely to will be in line with consensus, what will 3Q11 trends bring given the extremely difficult comparisons?

PNRA

Panera Bread has seen tremendous growth over the last few years, as have other fast casual concepts, and the past couple of quarters have been especially impressive. Despite weather impacting the first quarter, comparable restaurant sales grew +3.3% versus a +10% comp, implying a 40 basis point sequential acceleration in two-year average trends.

As of the date of the most recent earnings call, April 27th, reported 2Q to-date comparable restaurant sales growth was +5.3%. The guidance range provided for the same date was +5 to 6%, the mid-point of which would suggest acceleration in two-year average trends of 90 basis points.

Hedgeye: PNRA recently launched its first national advertising campaign, which should provide a lift to the current trends.

SBUX

Starbucks’ stock has been on an incredible run and, with prices rising, some investors I have spoken with are wondering when to pile in on the short side. I am certainly not there; I think the company has further avenues for growth available. Growth for Starbucks, going forward, is expected to come primarily from its CPG business and China. Unless you are bearish on the aggregate of these two factors, I think it is difficult to build a credible short thesis.

In terms of guidance, management expects revenue growth for the full year to be driven by mid single-digit comp growth. I remain positive on Starbucks’ future business prospects and believe that the company is taking the right steps to grow market share, whether it is developing mobile payment apps for Android and i-Phone smart phones or taking control of its distribution channels to protect the brand’s equity. I expect a strong quarter from Starbucks from a sales perspective, but coffee costs rising does pose a concern.

Hedgeye: Intra-quarter, our in-store analysis suggested that SSS were double digits during the Frappuccino promotion. I expect SBUX to have another strong quarter.

SONC

Sonic’s comparable restaurant sales growth has been impressive of late, with the premium six-inch hot dog promotion driving traffic across all day parts. Customer satisfaction scores have improved and the value initiatives have been resonating with consumers. On June 22nd, however, it was interesting to hear management describe a slowing in trends over “the past few weeks” during an earnings conference call. The company was reluctant to shed light on the magnitude, or any other specifics, regarding the slowdown.

Going forward, management is basing its hopes of bringing back incremental traffic on promotions including a BAJA hotdog and a new line of shakes. Despite the fact that value offerings were highlighted as being responsible for driving traffic in the third fiscal quarter, the company felt comfortable adding 0.5% of price to the menu in early June. The company now has 2% of price on the menu which will not begin to roll off until next April.

Hedgeye: SONC is relying on the “hotdog” to boost SSS from the May/June slowdown. This will be a close call.

WEN

Wendy’s is a stock that I like over the longer term but, as I highlighted in a post on June 16th, “WEN - INTERMEDIATE TERM ISSUES BUT THE LONG TERM STILL LOOKS GOOD”, there are some intermediate term issues that bear keeping in mind. Net net, I like WEN as a standalone concept, near-term issues aside.

On the positive side:

- Completed initiatives around the core products should improve consumers’ opinion of the Wendy’s brand

- Further improvements in the 2011 pipeline including new burgers will be key to driving traffic in 2H11

- Trends are improving at Wendy’s and I expect the company to take some price this year.

On the negative side:

- The company has tested four new restaurant designs and expects to begin a new rollout plan in 2012. I believe that the success of MCD’s new units in Tampa, Florida, has given pause to the WEN management team in their process.

- The current level of sales at breakfast is not supportive of a major roll-out.

Hegdeye: WEN will not see a meaningful pick up in SSS until 4Q11, at the earliest.

YUM

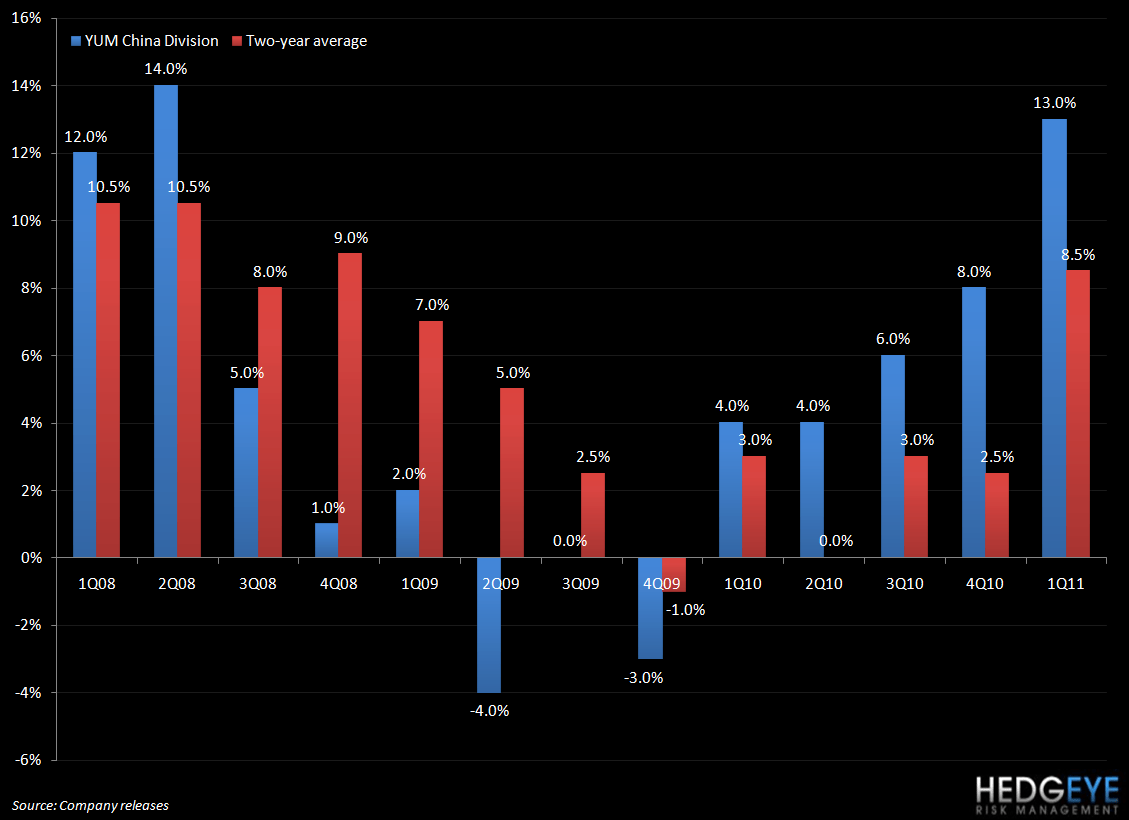

YUM’s U.S. business is stagnating and management is not forthcoming with any earth-shattering solutions. That is not to suggest they should have a “silver bullet”; their KFC, Taco Bell, and Pizza Hut concepts are in a tough place in the domestic market. However, China and YRI remain major growth engines for YUM and, as I’ve said before, without a bearish view on China, I would not advise investors to be bearish on YUM.

Hedgeye: YUM USA is a disaster, with all three concepts seeing comps down between 3-7%. YUM China is likely to post its second straight quarter of double digit SSS.

Howard Penney

Managing Director