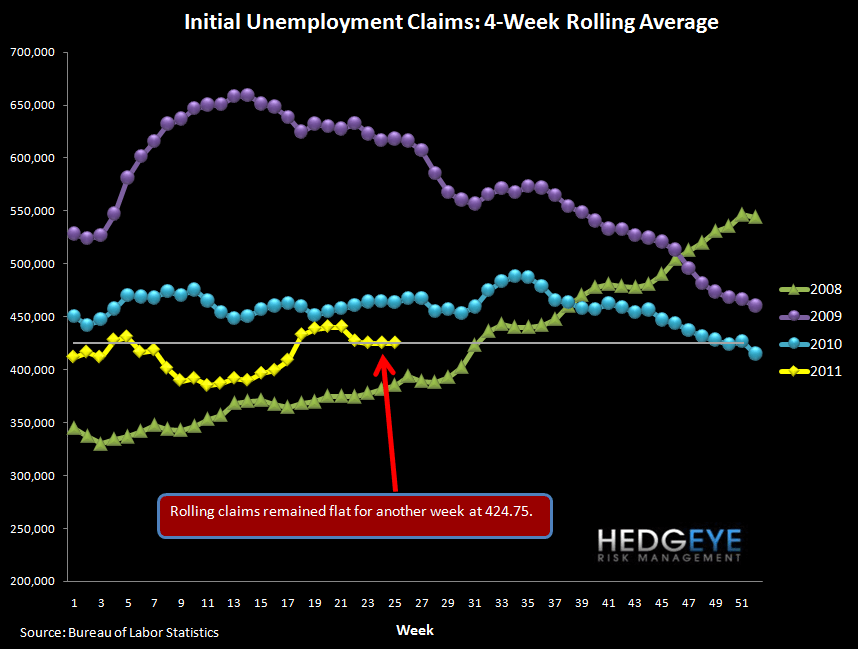

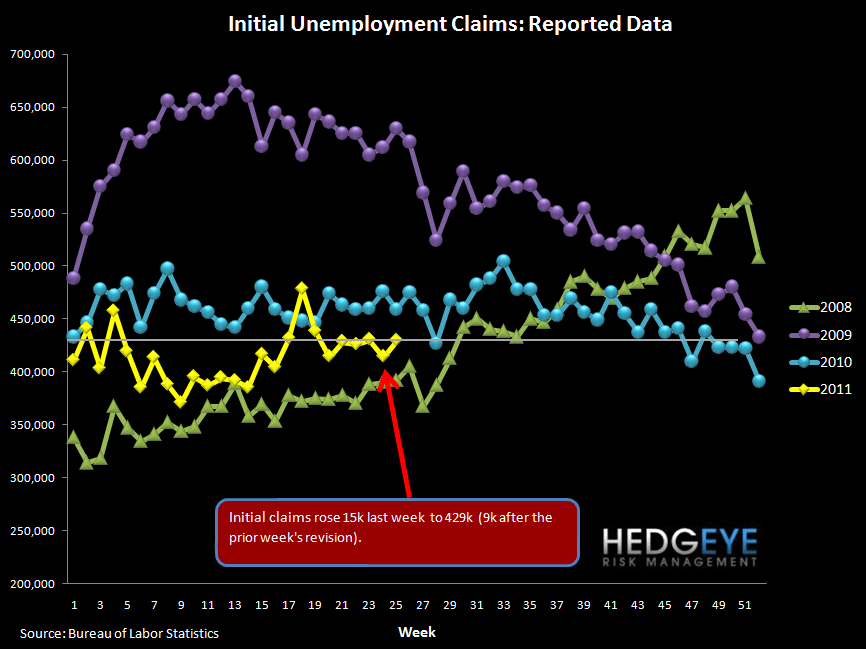

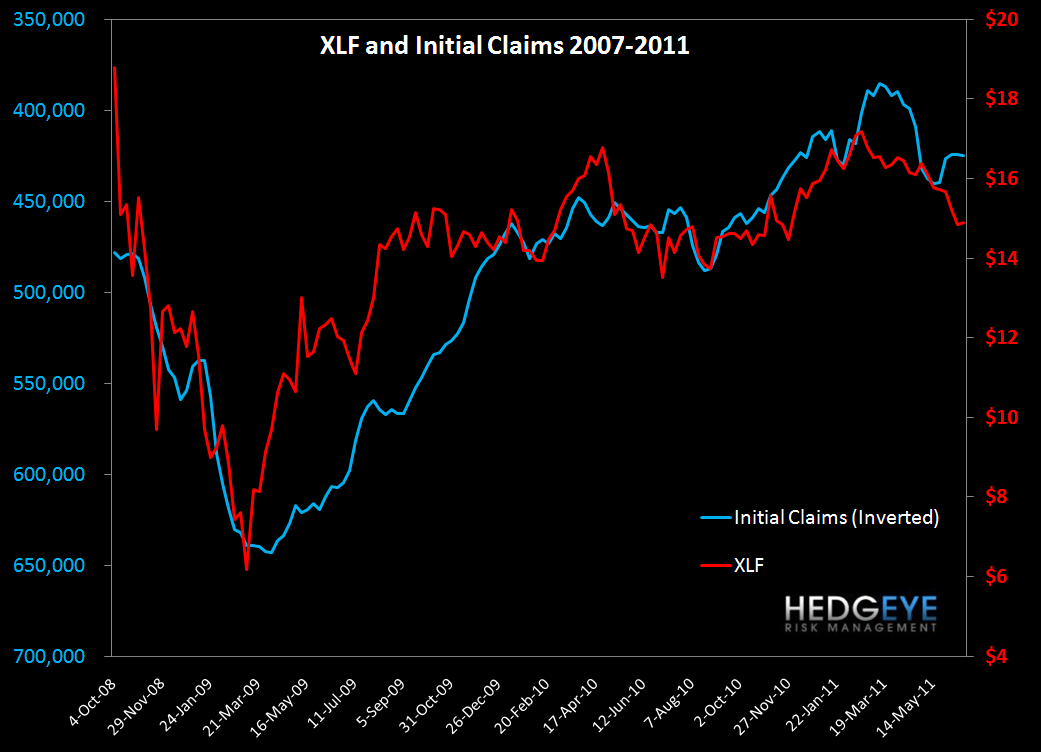

Initial Claims Still Stuck Well Above 400k

Initial Claims rose 15k last week to 429k (+9k after the revision to last week's print). The rolling 4-week average was flat for a third week in a row at 425k. Our analysis shows that initial claims need to drop below 375-400k to get an improvement in unemployment, levels that we have not achieved since February/March of this year. As the charts below show, QE has been tightly correlated with improvement in claims, suggesting that the coming weeks may see a very choppy period.

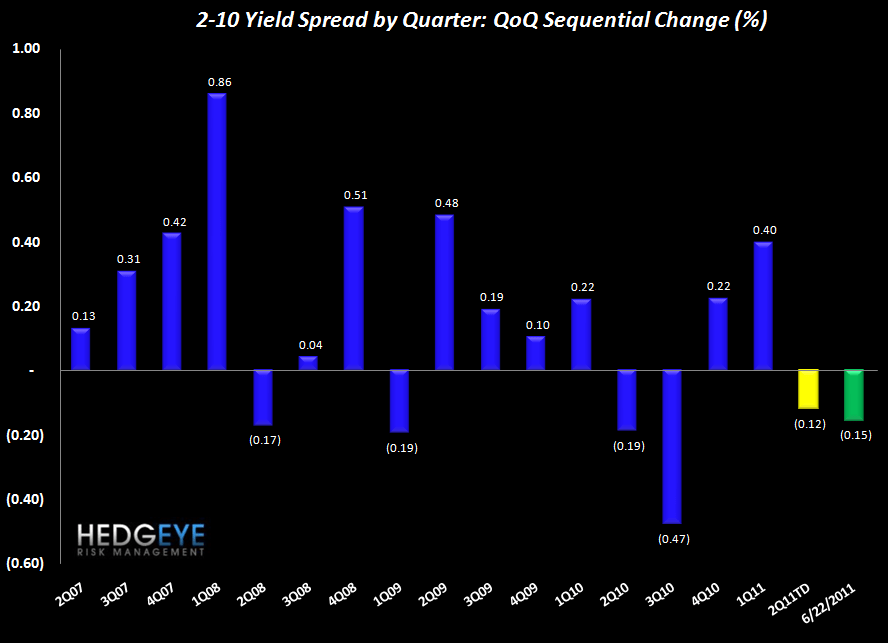

2-10 Spread Widens Slightly

We track the 2-10 spread as a proxy for NIM. This week the spread level widened by 2 bps to 261 bps from 259 last week. Thus far in 2Q, spreads are 12 bps tighter than the average of 1Q, posing something of a headwind to margin expansion in the quarter.

Financials Subsector Performance

The chart below shows the price performance of subsectors over four durations.

Joshua Steiner, CFA

Allison Kaptur