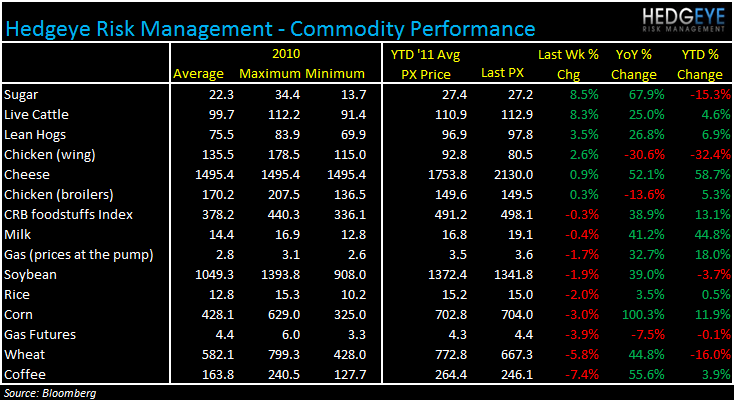

Price instability continues in commodity markets with large gains and declines seen in many commodities over the past week.

OVERVIEW

Coffee, wheat and corn prices came down considerably week-over-week while meat prices soared. Earnings kick off, in earnest, in mid-July and it will be fascinating to hear what management teams have to say about cost of sales. Cheese, in particular, is one that catches the eye. The price of cheese conveniently declined into last quarter’s earnings calls but has now shot back past the March high to a YTD high (see detail below). The USDA estimates that overall that U.S. food costs may rise 4% this year, the most since 2008.

LIVE CATTLE (RRGB, JACK, WEN, MRT, EAT, MCD)

Beef prices have risen sharply over the past week to boost the YTD figure back into positive territory after a drought in Texas, and subsequent slaughtering of livestock, has provided some relief in beef prices. Recent supply and demand metrics suggest that the elevated prices of beef may continue for some time, perhaps exceeding the expectations of some management teams.

Live cattle prices were supported by tighter supply pulling demand forward. Overseas demand for U.S. beef as also pushed prices higher.

Below are some comments from management teams on recent earnings calls regarding beef costs that we feel are important to keep in mind heading into the upcoming earnings season:

- RRGB (5/20/11): Ground beef could be higher by as much as 20% year-over-year, which has a meaningful negative impact to our margins. Hedgeye: live cattle prices are up +25% y/y

- JACK (5/19/11): Beef accounts for more than 20% of our spend and is the biggest factor driving the change in our guidance. For the full year, we are now anticipating beef cost to be up nearly 14% versus our previous expectation of 9% inflation. We expect beef cost to be up approximately 14% to 15% in the third quarter. Hedgeye: beef costs are likely going to exceed JACK’s prior guidance.

- WEN (5/10/11): We communicated to you back in March that we expected beef cost to rise approximately 10% to 15% and that we expected our total commodity costs to rise 2% to 3% in 2011. We are now forecasting that our beef cost will rise 20%. Hedgeye: there is moderate upside risk to beef price guidance for WEN.

- MRT (5/4/11):

Q: I wanted to re-visit the overall expectations for your commodities basket, and I missed the part about beef, just wanted to verify that it was up in the 20% range.

A: No. No, no. I said the low double-digits.

- EAT (4/27/11): Well, consistent with what we've talked about in the last month or so as we visited many of you, beef continues to present the most significant inflationary pressure in our commodity basket.

- MCD (4/21/11): And so if the commodity markets move significantly from here and the main ones obviously looking at beef, looking at corn, wheat, coffee, et cetera, our guidance reflects where the markets are today. If they stay around these levels, the 4% to 4.5% [commodity guidance for 2011] should be locked in. If they move dramatically up or down, then we'll have to reflect that as we move forward. Hedgeye: inflation guidance may have to be adjusted higher.

WHEAT (MCD, PNRA, DPZ)

Wheat costs declined -5.8% over the past week as temperatures, variable rainfall, and adequate soil-moisture reserves in the U.S. Midwest will promote plant growth, according to Don Roose, the president of U.S. Commodities Inc. in West Des Moines, Iowa. Ukraine’s exports of wheat will probably decline to 3.7 million metric tons for the year ended June 30 from 9.2 million tons the year prior (a 60% decline). Prices have gained over the past couple of days on speculation that the lower prices will bring in buyers.

Below are some comments from management teams on recent earnings calls regarding wheat costs that we feel are important to keep in mind heading into the upcoming earnings season:

- MCD (4/21/11): And so if the commodity markets move significantly from here and the main ones obviously looking at beef, looking at corn, wheat, coffee, et cetera, our guidance reflects where the markets are today. If they stay around these levels, the 4% to 4.5% [commodity guidance for 2011] should be locked in. If they move dramatically up or down, then we'll have to reflect that as we move forward. Hedgeye: inflation guidance may have to be adjusted higher.

- PNRA (4/27/11): In this expense line, we expect margin unfavorability to continue to grow on increased all-in cost inflation throughout the year -- and because we haven't taken and we don't currently plan to take pricing in our dough sales for franchisees this year. Hedgeye: wheat inflation could possibly subside in the back half of the year as comparisons become less unfavorable for buyers. This will be more likely, of course, if the dollar strengthens.

- DPZ (3/1/11): We’ve got wheat locked down for the year.

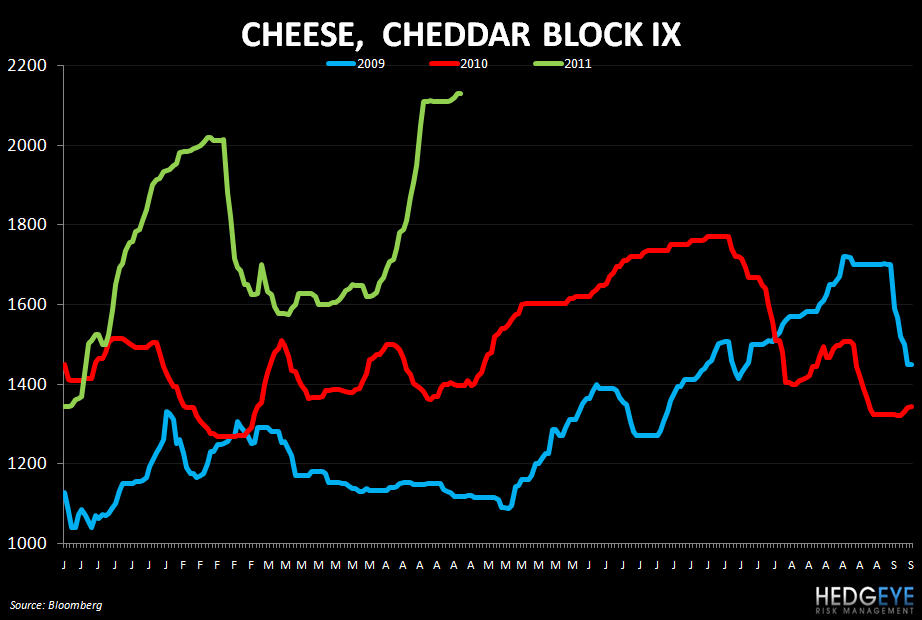

CHEESE (CAKE)

Dairy costs were relatively flat week-over-week but, pertaining to our short thesis on CAKE, the chart below tells you all you need to know about their inflation guidance for 2011 (+4.5% in 1H, +2.5% in 2H). Barring a significant drop in dairy prices, it is likely that inflation guidance for 2H will have to be raised.

CHICKEN WINGS (BWLD)

Chicken wing prices seem to be turning higher as we head into the second half of the year. This is not unusual, as the chart below shows, but on a global basis it seems that chicken prices may see more support going forward. Inflation is clearly not likely for the remainder of 2011 but, as this is almost certainly baked into the price of BWLD, the outlook into 2012 is important to monitor.

Howard Penney

Managing Director