This note was originally published June 15, 2011 at 07:55am ET.

“True, atomic bombs have made nuclear war so catastrophic that I am convinced no country wishes to resort to it. But I am equally convinced that we are at the mercy of an error of judgment or a technical breakdown, the source of which no man may ever know.”

-Jean Monnet

Jean Monnet is regarded by many as the chief architect of European integration. Following the World Wars, there was much support for political movement that would lessen the probability of the horrors and injustices that ravaged Europe for so much of the first half of the Twentieth Century being repeated. Indeed, a plaque in Washington D.C. on the front of the Willard Hotel memorializes Monnet as a man that died as a “proud citizen of the Europe he inspired and helped to create”.

The period immediately following World War II was clearly anomalous in many respects. For one, there was broad consensus on the need for closer European integration which, it was claimed, was the only way to defeat the ugly beast of Nationalism that had marred so much of the continent’s past. Every viewpoint must be understood in the context of the environment in which it is adopted. Winston Churchill, possibly the most proud of all Englishmen, was firmly in favor of European integration. In a speech at Zurich University, that came to be known as “The Tragedy of Europe”, Churchill stated plainly, “We must build a kind of United States of Europe”. His conviction in this matter was clearly derived from his experiences of war-time Europe, speaking as he was in September of 1946. Interestingly, while his use of “we” implies British participation in the process, he excluded Britain from his description of the proposed “United States of Europe”.

Given that a key initial component of the European project, as proposed by the Schuman Declaration, was to be the pooling of coal and steel production, it is astonishing to think just how economically and financially integrated the present day European Union is. Merely fifty-five years later, the labyrinthine European financial system has become so complex and interconnected that understanding the implications of policy changes or – indeed – the limits of national autonomy within Europe, has become exceedingly difficult.

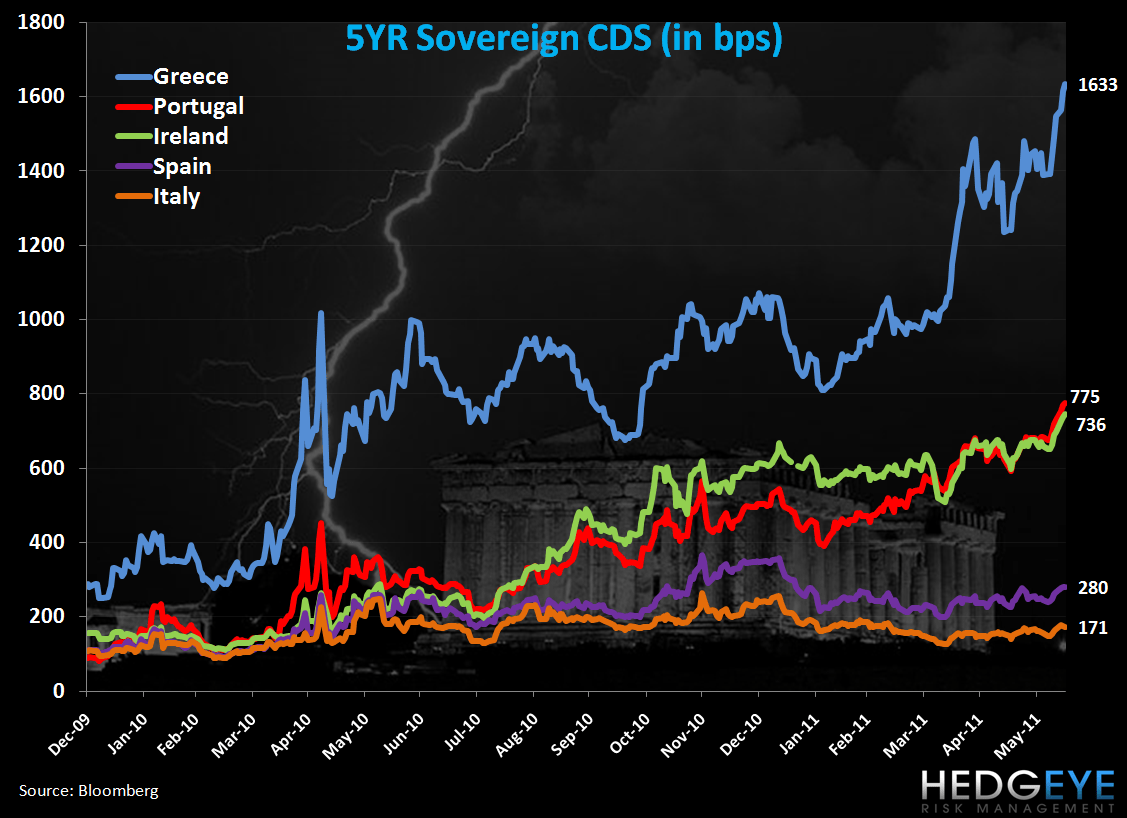

Indeed, Matt Hedrick, Hedgeye’s cerebral Europe Strategist, has recently been analyzing the nuances of the European banking system of late. The guidelines by which European money is created is quite opaque, with many standards relating to banking practices within the European Monetary Union seemingly in a constant state of flux. For example, Matt has pointed out recently, in dialogue about Greece with a Hedgeye client, that National Central Banks can decide what collateral to accept from commercial banks based on ECB guidelines. However, recent concessions mean that government debt and bank assets rated near or at junk are acceptable in some cases. In addition, the recent downgrading of Greece to a credit rating of CCC from B by Standard & Poor’s is drawing attention to the country’s ability, or lack thereof, to meet future obligations. There are innumerous potentially unexpected consequences that could arise from the current system.

It has been astonishing to hear market commentators dismiss the risk Greece poses to the broader European and global financial markets. Some television pundits have asserted that “Greece doesn’t matter”. Clearly, given the interconnected nature of risk within the European financial system and the fact that the Bundesbank has the most exposure of any European bank to the peripheral countries, Greece absolutely matters. The determination of European leaders such as Jean-Claude Trichet to assuage any and all fears of contagion within Europe – be they emanating from Greece, Ireland or elsewhere – speaks to this fact.

Of course, European leaders have been forced to choose their words increasingly carefully since, essentially, the outset of the European sovereign debt crisis began attracting attention in 2010. For instance, the viability of the single European currency has been called into question for some time. As Hyman Minksy writes in “Stabilizing an Unstable Economy”, “Money arises not only in the process of financing, but an economy has a number of different types of money: everyone can create money; the problem is to get it accepted”. This point highlights a crucial role that the European Union is assuming on a broader sense: assuming that the currency – and means by which it is created – continues to be accepted. This logic can be extended to other facets of the European Union. It is not only crucial that the common currency continues to be accepted by the people, but also that the common monetary policy, laws, policies and frameworks continue to be accepted also. As social unrest intensifies in Europe, it becomes more and more challenging to bind a continent together which, for so much of its history, has been defined by factionalism.

The “Greece doesn’t matter” attitude is typical of U.S. centric investors that, time and again, commit the sin of neglecting to realize the interconnected nature of global macroeconomic risk. It is acutely ironic that it may just be the highly integrated nature of Europe that breeds disagreement in the 21st Century after Monnet, Schuman, and so many others saw integration as key to securing the future prosperity of Europe’s people. As recently as 2005, this view was held firmly. Whether in Celtic Tiger Ireland or the booming Costa del Sol in Spain, European integration was credited as a key driver of prosperity. Many in the peripheral countries now blame a lack of monetary autonomy for sluggish growth.

What’s voted by the market as “good” today can be “bad” tomorrow. That can be correlation risk, interest rate risk, geopolitical risk or any other condition or accepted truism. Investors that dismiss this reality are repeating the mistakes of the recent past, just as we believe that policy makers in Washington are repeating mistakes made in the 1970’s that led to Jobless Stagflation. If an unfortunate turn of events did take place in Europe – George Soros recently stated his belief that the risk of this is mounting – the traditional response will take over the airwaves: “it was unforeseeable”. What is foreseeable about markets is that they are unpredictable, especially in Europe which has seen so much turmoil and conflict throughout its modern history. From a shorter-term perspective, price is telling us all we need to know as equity markets slump and CDS spreads continue to widen. While the U.S. has no shortage of its own internal problems, we know from very recent history that the global markets are closely interconnected.

Indeed, as Churchill said in “The Tragedy of Europe”, “Is it the only lesson of history that mankind is unteachable?”

Rory Green

Analyst