“He had shown himself to be … a young man who took great pride in his perseverance and steadiness of purpose.”

-Stephen Ambrose

A month or so ago I referenced researching more about the roots of Jeffersonian thought (an alternative to British Keynesianism). Being a Canadian who is constantly thirsting to be educated in American history, I often lean on my American-born colleagues for reading recommendations.

One of our analysts, Allison Kaptur, pointed me towards Stephen Ambrose’s “Undaunted Courage” – the story of Meriwether Lewis, Thomas Jefferson, and the Opening of the American West. It was easily one of the most gripping and inspirational stories I have ever read.

The way the best storytelling is told is when the author personalizes the experience and reaches in and grabs you. Many of you will be familiar with the late Stephen Ambrose for his work in “Band of Brothers.” Many of you may not be familiar with the passion Ambrose had for backpacking every step of the Lewis & Clark Trail with his family.

“Of courage undaunted” was the opening description of Thomas Jefferson’s praise for Meriwether Lewis. It’s where Ambrose’s wife, Alice, came up with the idea for the title of the book. As Ambrose acknowledges best in answering the question, “what is the secret to being a successful author?” – “Marry an English major.”

Lewis never married. He died, tragically, at the very young age of 35 years old in Hohenwald, Tennessee, shortly after being appointed by Jefferson as the Governor of Louisiana in 1806. While it would be easy to tell stories about how messed up Meriwether’s mind became in his final years, I think it’s best for Americans to celebrate the confidence and courage it took for him to change the world.

“At eighteen years old, he was on his own. He had travelled extensively across the southern part of the Unites States. He had shown himself to be a self-reliant, self contained, self confident teenager…” (Ambrose, “Undaunted Courage”, page 29)

After 6 consecutive down weeks for US stocks, I’m calling attention to this story after being inspired by a great American Olympian who I have the pleasure and privilege of working alongside at Hedgeye – Bob Brooke.

On Wednesday night, Bob, Big Alberta, Darius Dale, Kevin Kaiser, and I were having a few beverages watching Game 4 of the Stanley Cup Playoffs with our summer interns. After proudly attending his son’s graduation at a very patriotic ceremony at Notre Dame, Bob told me it was a good time to think about a way to communicate to our clients how optimistic we are about the future.

You see, Wall Street and Washington like to put people like us in boxes. When you’re always thinking inside of the box – I guess that makes sense. You’re either a Bull or a Bear, a Democrat or a Republican – and it’s easier for these group-thinkers to generalize and not take the time to understand what something new could mean.

Just because I am bearish on US Equities, old Wall Street, and Keynesian Central Planning in Washington, doesn’t mean I don’t have the confidence and courage to put my own capital at risk to build a great team in this great country.

In fact, it’s quite the opposite – everything I am pessimistic about, gives birth to my optimism.

At the Hedgeye Holiday Party this past December, I cited a very popular American country song titled “Bless the Broken Road” (recent rendition by Rascal Flatts) to better explain why it’s our industry itself that gives me reason for optimism:

Every long lost dream led me to where you are

Others who broke my heart they were like Northern stars

Pointing me on my way into your loving arms

This much I know is true

That God blessed the broken road

That led me straight to you

Without giving away Hedgeye’s strategy to continue to be the change we want to see in this profession, that’s all I have to say about that. If Wall Street and Washington don’t realize that the most simple solution to all of this is to stop what they are doing, then the rest of us will just have to keep plugging away until we’ve reached the new open frontier of American Optimism that’s as old as America itself.

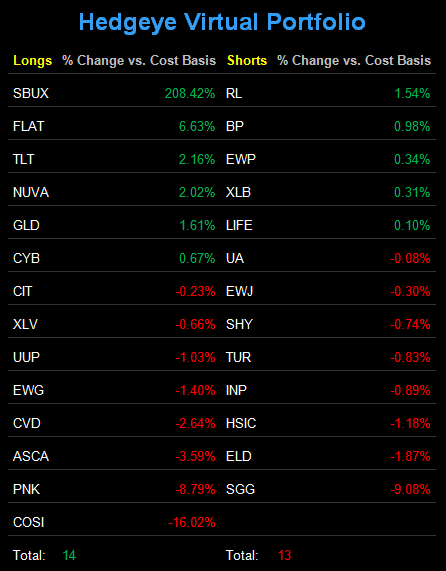

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1, $98.46-102.91, and 1, respectively.

God Bless America,

KM

Keith R. McCullough

Chief Executive Officer