This note was originally published at 8am on June 06, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“A movement whose main promise is the relief from responsibility cannot but be antimoral.”

-F.A. Hayek

It was a long, hard, weekend for the central planners of wanna-be Keynesian Kingdoms. In the US, “blue chip economists” advising President Obama were busy obfuscating the simple fact that QG2 has equated to Jobless Stagflation. In Europe, the socialists were voted off another proverbial island of responsibility – Portugal.

Where do we go from here? What broken promises does Academic Dogma have in store for us next? Fortunately, plenty of these outcomes have been proactively predictable. And those of us responsible for being responsible are well on our way to seizing the opportunity of cleaning up another mess.

The aforementioned quote comes from Hayek’s chapter titled “Material Conditions And Ideal Ends” in The Road To Serfdom (page 217). And, while it’s always dicey to talk like a Coach would about virtue and morality on Wall Street, I think the way that Hayek thought about this in 1944 is no less relevant than it is this morning:

“It is true that the virtues which are less esteemed and practiced now – independence, self-reliance, and the willingness to bear risks, the readiness to back one’s own conviction against a majority, and the willingness to voluntary cooperation with one’s neighbors – are essentially those on which the working of an individualist rests. Collectivism has nothing to put in their place.”

-F.A. Hayek (The Road to Serfdom, page 217)

It’s time for leadership. It’s time for change.

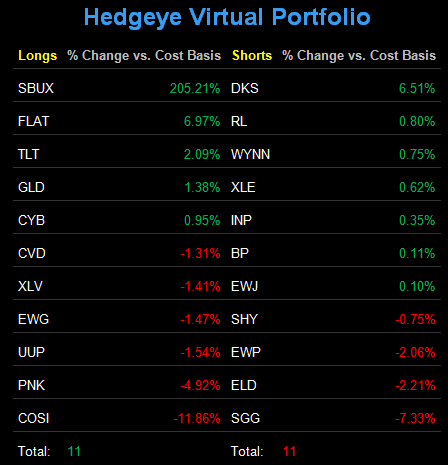

Last week, I didn’t make many changes to the Hedgeye Asset Allocation Model (our proxy risk management product for gross invested exposure). After starting the week net-short in the Hedgeye Portfolio (our proxy for expressing net exposure), I didn’t change a whole heck of a lot either (I covered a few shorts to end the week with 11 LONGS and 11 SHORTS).

The Hedgeye Asset Allocation Model’s complexion at the close last week was:

- Cash = 49% (no change week-over-week)

- International Currencies = 24% (Chinese Yuan and US Dollar – CYB and UUP)

- Fixed Income = 15% (Long-term US Treasuries and US Treasury Flattener – TLT and FLAT)

- US Equities = 6% (US Healthcare – XLV)

- International Equities = 3% (Germany – EWG)

- Commodities = 3% (Gold – GLD)

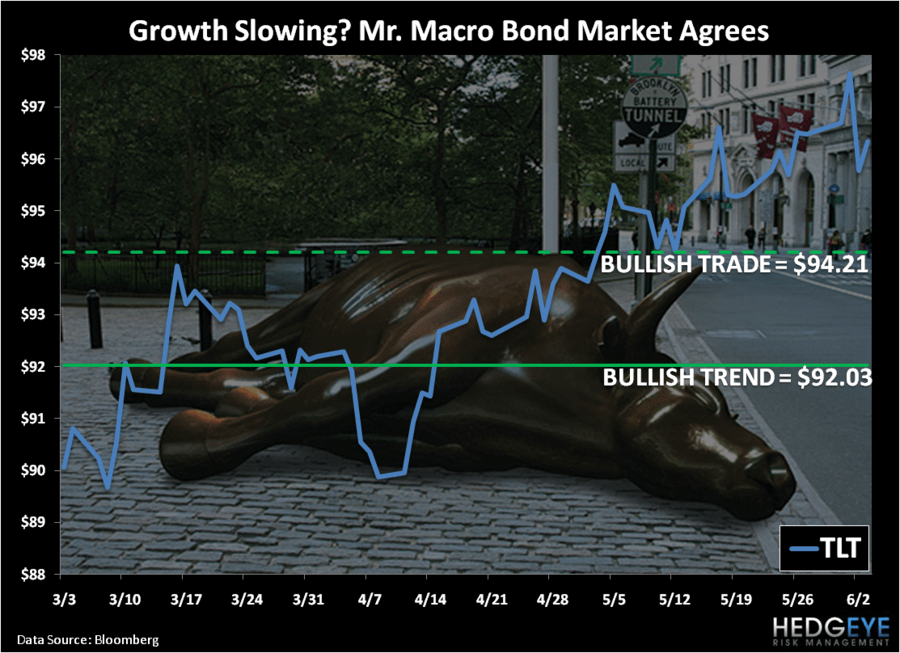

With Growth Slowing, Long-term Treasury Bonds (TLT) are putting on an impressive move to the upside. Growth Slowing is also instigating compression in the yield curve (long-term minus short-term interest rates) and we’ve also expressed our conviction in Growth Slowing with long positions in a US Treasury Flattener (FLAT) and Gold (GLD).

Did I say Growth Slowing?

“The readiness to back one’s own conviction against a majority…”

The #1 headline on Bloomberg this morning reads: “SLOWING US GROWTH PROMPTS OPTIMISTS TO QUESTION DURABILITY OF RECOVERY”

You see, without explicitly seeking Relief From Responsibility, this is how Wall Street works – seeking relief in building a consensus. The best way to perpetuate mediocrity, is to socialize responsibility.

Or at least they’ll try. Because the true art of Old Wall Street Research compensation lies not in the risk management of being right or wrong – it lies in the storytelling of collectivism.

In the Hedgeye Asset Allocation Model, where was I wrong last week?

- Long US Dollar (UUP) = down -1.0% week-over-week

- Long US Healthcare (XLV) = down -1.4% week-over-week

It doesn’t particularly matter why I was wrong with these positions. The scoreboard doesn’t care. I was wrong – and there needs to be absolute responsibility in recommendation.

“Independence, self-reliance, and the willingness to bear risks…”

That’s what we need to champion in this business. Re-think, re-learn, and re-invent. With “the willingness to voluntary cooperation with one’s neighbors”, may the best teams who are collaborating best risk management practices win.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1530-1549, $98.32-102.34, and 1296-1320, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer