On average, the up moves were stronger than the down moves in the commodity prices we track in our commodity monitor. Milk and Cheese, in particular, put on strong moves while wheat was the most notable mover to the downside (as shown in the chart below).

Dairy

Cheese and milk prices moved sharply higher last week, 12.8% and 14.1% respectively. For DPZ, PZZA, CAKE, YUM’s Pizza Hut and other restaurant companies, this is an important data point. Coming into the second quarter, dairy prices corrected sharply, allowing some respite for restaurant companies with exposure to dairy costs. This also saved the management teams from answering the questions that the charts below pose. As the charts below indicate, dairy prices are more volatile than they have been over the past couple of years. Below are some select quotes pertaining to dairy costs from management teams’ most recent earnings calls. DPZ may have been right on 1Q, but it seems that 2Q’s gain may take them by surprise. While DPZ has a contact that effectively eliminates one-third of cheese market volatility, the current trajectory and amplitude of the move in cheese prices is negative for restaurant operating margins.

JACK (5.19.11): “Cheese also accounts for about 6% of our spend and we continue to expect a 15% increase for the year.”

DPZ (5.5.11): “And really the one to watch as always is cheese and our best bet right now is that it's going to stay relatively close to where it is right now but cheese is the one that often gives the biggest surprises either up or down and that's the one to kind of watch but assuming cheese stays relatively flat from here on out then, the absolute food costs from – through the rest of the year are probably going to stay pretty consistent with where they were in Q1 which to your point means the percentage year-over-year increase will probably ease a little bit over the course of the year.”

CAKE (4.20.11): “The first half of the year, we're expecting food cost inflation of about 4.5% plus and then in the last half of the year, about 2.5% minus. And a lot of that has to do with the fact that we expect to lap a lot of high dairy costs from 2010 and the fourth quarter of 2011, but also due to the fact that we expect to have slightly lower fresh fish costs, slightly lower cheese prices, than last year as well.”

CMG (4.20.11): As we move into 2011, we’re expanding our use of cheese and sour cream made with milk from cows.

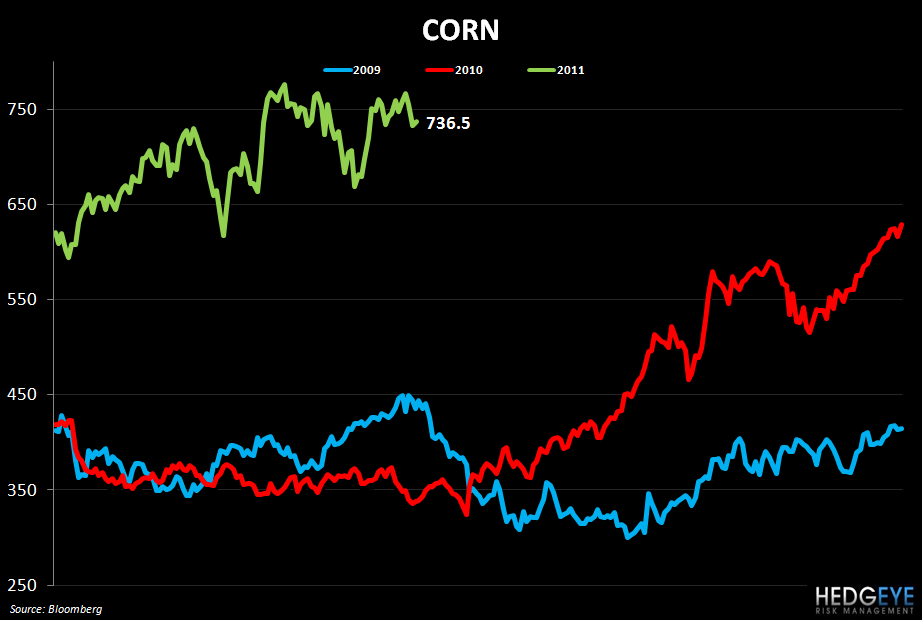

Corn

Corn prices took a dive over the last week, declining 1.5%. Nevertheless, the grain remains up 119.4% year-over-year and it can be expected that protein prices will remain supported as long as these elevated prices remain. In terms of the supply and demand data points, the preponderance of the factors seems to suggest that prices will remain high for the foreseeable future, the occasional correction notwithstanding. According to Bloomberg, wet weather-related planting delays may send global inventories to their lowest level in 37 years. More than one third of Midwest fields were planted after the mid-May target for optimal growth because of excessive rain. Below, we outline some comments from restaurant (and food) company management teams pertaining to corn.

AFCE (5.26.11): “This is up from our previous guidance of a 2% to 3% increase, primarily due to higher commodity costs in corn and soy, which impacts our bone-in chicken, as well as increases in the cost of flour and cooking oil.”

TSN (5.9.11): “There is nothing really to stop us from buying back stock other than what's in front of us that's quite uncertain. What if corn goes to $10? Those kinds of things; we really maintain a lot of liquidity. It's $1.6 billion right now. We need to maintain a lot of liquidity.”

JACK (2.24.11): “And then there are some Act of God provisions that will get us north of our contract bands, but at a reduced rate from what the current market pricing is. So I hope that that helps. And then also grain, corn, wheat and soybean impact, and there are input costs for a number of the proteins. And that's really what's driving up beef at this point."

Chicken Wings

Chicken wing prices gained week-over-week as ample supply (broiler egg sets six-week average was up +1% year-over-year) offset rising substitute demand.

Howard Penney

Managing Director