This note was originally published at 8am on June 02, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Nothing is easier than self deceit.”

-Demosthenes (circa 340 BC)

I’m borrowing that quote from Howard Marks, who borrowed it from Charlie Munger, who borrowed it from Demothesnes (Greek orator from ancient Athens). Borrowing ideas is what people in this business do.

What if I woke up every morning for the last 6 months borrowing the idea that US “growth” was “back” and that there was really nothing in this interconnected world to worry about?

Well, that idea would have been a really bad one to have borrowed. Nothing is easier than borrowing ideas – you have to do a lot less work. Nothing is going to protect your returns when those borrowed ideas turn out to be wrong either.

Howard Marks is a successful Risk Manager who runs $82 Billion (as of December 31, 2010) at Oaktree Capital Management. He borrowed that quote for his recent investment memo to Oaktree clients that was titled “How Quickly They Forget.”

Since Marks’ letter is marked “confidential”, I’ll have to stop on his ideas there, and get back to my own:

- GROWTH: US and Global Growth are slowing

- INFLATION: reported Global Inflation readings remain sticky and elevated because they are lagging indicators

- POLICY: Chinese policy (hawkish) continues to diverge from Fiat Fool policy (USA, Japan) which remains Indefinitely Dovish

Being on the road from Boston to Denver to Kansas City to New York to San Francisco in the last 4 weeks has been very interesting. The further I move in time, the more people seem to be agreeing with me on these Global Macro matters (prices going down do that). I’m in Santa Barbara, CA this morning and I’ll be in LA tonight. I don’t expect this bearish progression to lose momentum.

The #1 question Risk Managers want to know is “how do I make money with that?”

Hedgeye Risk Management’s answer remains:

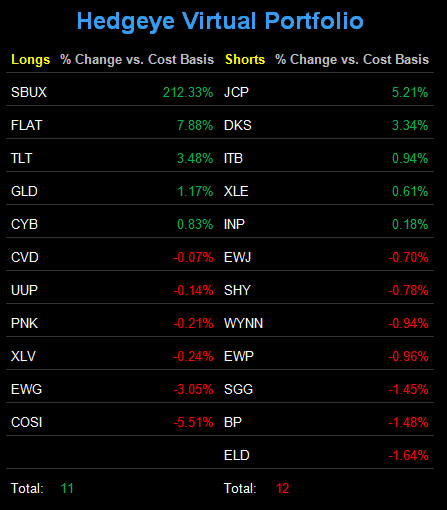

- Don’t lose money (we went into yesterday’s meltdown with 10 LONGS and 12 shorts in the Hedgeye Portfolio)

- Buy Long-term US Treasuries (TLT) and a US Treasury Flattener (FLAT)

- Buy Gold (GLD)

Oh, did I borrow the only rule Buffett and Munger have signed off on before the 2011 version of buy-the-damn-dips? I think I did. Not losing money is indeed a risk management strategy worth borrowing. Try it at home – or with your client’s money.

The #2 question Risk Managers want to know is “where could your ideas be wrong?”

Hedgeye Risk Management’s answer remains:

- The Data – if our scenario analysis on growth and/or inflation change, we will

- The Market – if TREND line prices hold, we’ll cover shorts

- The Fed – if they legitimately move to QG3, we will resort to prayer

While Borrowing Deceit from the Fed on A) full employment and B) price stability can remain fashionable – it can also become, as Le Bernank likes to say, “transitory.” If the price of your homes and portfolios start going down, that is…

Of course, nothing is easier than waking up telling yourself that earnings were “good” and Le Bernank has your back. Sounds a little too much like Q2 of 2008 for me. “How Quickly They Forget.” (Howard Marks, May 25, 2011)

As for what to do in the very immediate-term, here are some key immediate-term TRADE ranges across Global Macro that we’re rolling with this morning:

- SP500 1305-1323 (bearish)

- Russell2000 801-828 (bearish)

- Nikkei 9257-9722 (bearish)

- Shanghai Composite 2669-2811 (bearish)

- FTSE 5801-5956 (bearish)

- DAX 7067-7344 (bearish)

- VIX 16.65-19.04 (bullish)

- USD 74.41-75.80 (bullish)

- Euro 1.41-1.44 (bearish)

- Oil 97.75-102.03 (bearish)

- Gold 1522-1549 (bullish)

- Copper 4.09-4.29 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer