TODAY’S S&P 500 SET-UP - June 6, 2011

There isn’t a data point or market price across the Hedgeye Global Macro risk management model that suggests this correction is over, yet:

- Treasury Bonds – continuing higher this morning w/ 2-yr yields crashing to 0.42% (10s at 2.99%); yield curve compressing

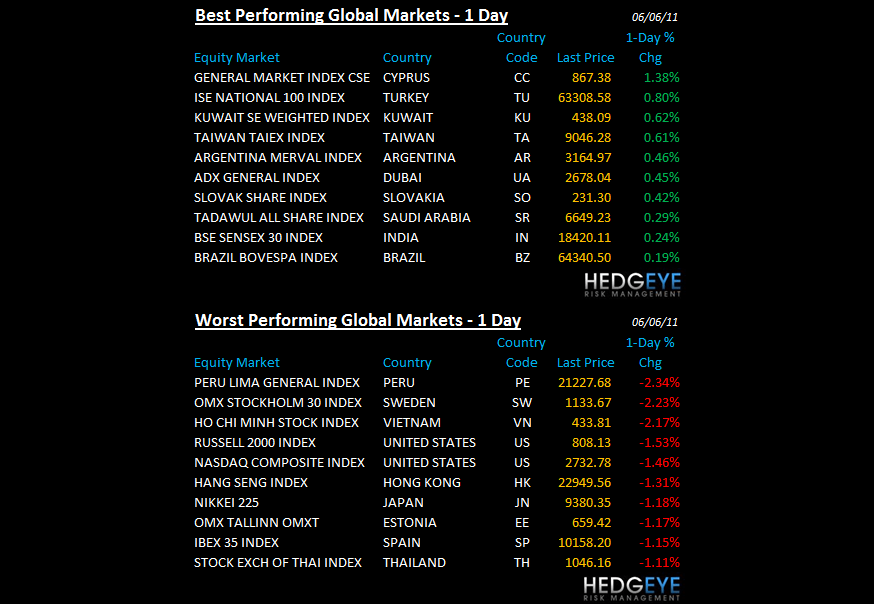

- Asian/European Stocks – Japan + Spain (2 of our short positions) down -1.2% and -0.9% this morning (Keynesianism not working)

- US Stocks – down for 5 consecutive weeks, which isn’t exactly textbook bull market (down -4.6% since April 29th high)

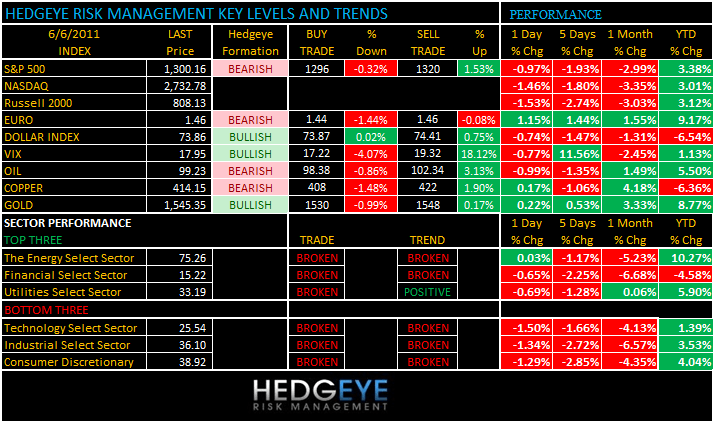

As we look at today’s set up for the S&P 500, the range is 24 points or -0.32% downside to 1296 and 1.53% upside to 1320.

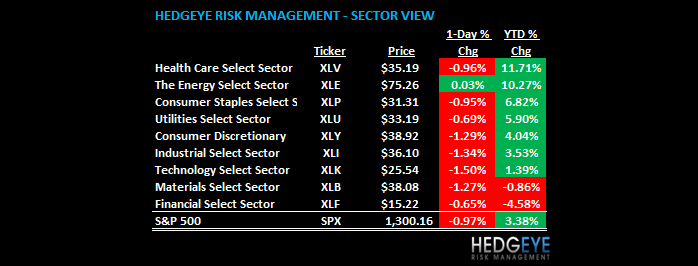

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1315 (+1135)

- VOLUME: NYSE 971.40 (-3.66%)

- VIX: 17.95 -0.77% YTD PERFORMANCE: +1.93%

- SPX PUT/CALL RATIO: 1.61 from 1.19 (-26.59%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.15

- 3-MONTH T-BILL YIELD: 0.04%

- 10-Year: 2.99 from 3.04

- YIELD CURVE: 2.57 from 2.59

MACRO DATA POINTS:

- 11 a.m.: Export inspections: corn, soybeans, wheat

- 11:30 a.m.: U.S. to sell $27b 3-mo., $24b 6-mo. bills

- 1:15 p.m.: Treasury’s Geithner speaks to bankers in Atlanta

- 4 p.m.: Crop conditions: Corn, winter wheat, cotton, soybean

- 5:30 p.m.: Fed’s Fisher speaks in NY

WHAT TO WATCH:

- Philly Fed President Charles Plosser said plan to withdraw central bank’s record monetary stimulus, “normalize” interest-rate policy would help avert confusion in financial markets

- Death toll from Germany’s E. coli outbreak rose to 22, with officials saying sprouts grown near Uelzen a “significant source of the bacteria”

- German government spokesman says expects EU/ECB/IMF report on Greece by mid week -- Reuters

- Social Democrats win Portuguese parliamentary election, removing the Socialist Party from power -- Boston Globe

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Wheat Fields Wilt in Drought as Parched Earth Spreads From China to Kansas

- Oil Falls for a Second Day on Signs Slowing U.S. Economy May Crimp Demand

- Copper Rises for Second Day as Strike at Codelco Mine Fuels Supply Concern

- Gold Advances for Second Day After U.S. Data Increases Recovery Concerns

- Wheat Climbs on Speculation USDA Is Set to Reduce Global Supply Estimate

- OPEC Overshadowed by Qaddafi in Most-Hostile Meeting Since 1990 Gulf War

- Russia’s Black Earth Grains Growing Area Faces ‘50-50’ Chance of Drought

- Rubber in Tokyo Advances for Second Day Amid Tight Supplies in Thailand

- Grain Stockpiles Worldwide May Drop, Soybeans May Increase, Survey Shows

- Commodity Bubbles Caused by Speculators Need Intervention, UN Agency Says

- Olam Said to Raise $600 Million in Share Sale to Help Fund Acquisitions

- Funds Boost Bullish Commodity Bets Amid Improving Global Growth Prospects

- E. Coli Outbreak Death Toll Rises to 22 as Blame Focuses on Bean Sprouts

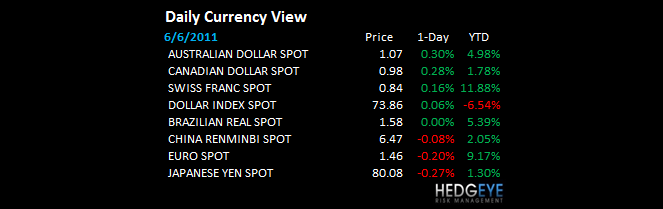

CURRENCIES

EUROPEAN MARKETS

- In Europe a wet Kleenex continues to hover over Europe Keynesian experiment; Spain down -0.8% after Portugal votes out the socialist party too

- UK new car registrations (1.7%) y/y in May - SMMT -- wires

ASIAN MARKETS

- In Asia, China closed but rest of Asia continues lower; Japan down -1.2% to -8.3% YTD (we're short $EWJ); Thailand down -1.1%; Vietnam -2.2%

- Hong Kong, China, and Taiwan were closed for Tuen Ng/Dragon Boat Festival

- South Korea was closed for Hyun Choong Il.

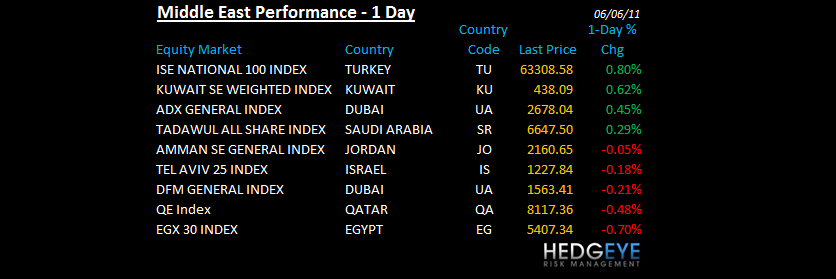

MIDDLE EAST

Howard Penney

Managing Director