Conclusion

Our bearish '4.5 Below' call for a severe cut in back half margins was bouyed by today's sales results. We remain bearish on the department stores -- in particular JCP -- and think that M and even KSS are setting up for a negative turn in the 2H. Same goes for HBI, GIL, JNY and DKS.

On the flipside we like names with asymmetric factors to drive upside, like NKE, LIZ (despite negative datapoint vis/vis JCP), FL, and despite broken near term TRADE, URBN and TGT.

Review of the Month

What started as a crack last month has turned into a clear deterioration in sales momentum for retailers in May. Recall last month, both Macy’s and Kohl’s called for pent up demand driven sales. Well, Macy’s pulled through posting solid results while KSS came in light much like the balance of retailers that still contribute to this monthly exercise. In fact, the number of companies missing expectations (14 of 22) came in higher than beats for the first time this year.

Instead of proving last month to be an aberration, May sales results lend further support to our thesis that the 2H set-up is not going to be a pleasant one. As expected, there wasn’t much in the way of adjustments to company lead expectations for the 2Q or the full-year with only a month into the quarter, however we suspect revision activity is likely to pick up in June as retailers get a closer look around the corner. Over the last month, we’ve seen increasing evidence of mounting margin pressure beginning to impact companies more significantly and sooner than expected and now we have top-line trends starting to roll as well. We saw a crack in 2-year comp trends last month for the first time since last July. Now this morning we have comps decelerating at an faster rate across all three durations (1Yr, 2Yr, & 3Yr) in May. With some retailers looking to accelerate sales in an effort to offset margin headwinds in the 2H, May results suggest that simply passing through higher costs will prove challenging in the face of slower consumer spending to say the least.

(clients that have not yet flipped through our industry overview outlining our scenario for a 4.5pt decline in industry margins this year, please contact sales at sales@hedgeye.com for a copy – we’d be happy to run through it with you).

Here are the notable callouts from May sales results:

- Higher-end products and brands continue to outperform. Within department stores, it continues to be a story of the “haves” vs. the “have nots” with JCP -1%, KSS +0.8%, SSI +0.0% underperforming the higher-end with M +7.4%, JWN +7.4%, SKS +20.2%. This continues to be positive for stronger brands like RL and GES.

- Discounters were again the strongest performing segment of retail consistent with trends since the holidays despite more difficult compares. We expect this to continue near-term as consumer’s propensity to spend on discretionary items deteriorates.

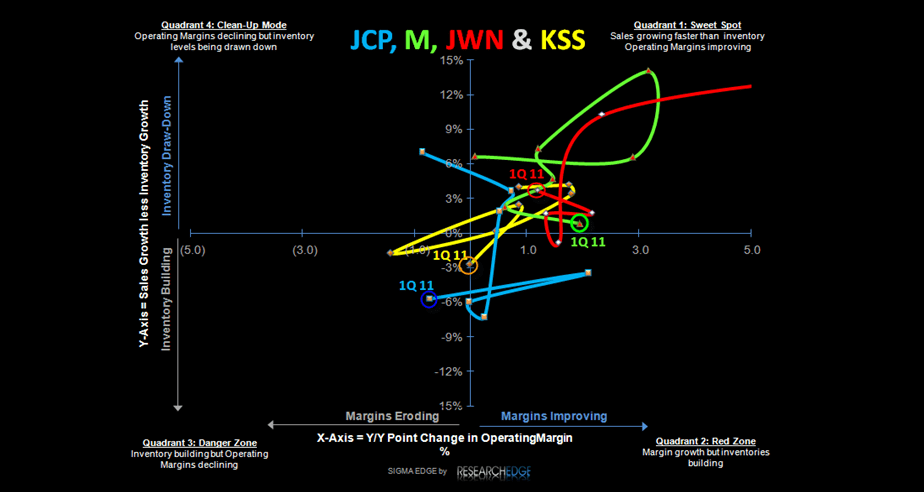

- JCP came in well below expectations citing weather for the second consecutive week as well as a shift of promotional mailers into April - a factor the company failed to mentioned as a positive driver last month. After a handful of brand highlights in April, Sephora was the only callout in May with Liz Claiborne noticeably absent. Additionally, internet sales remain underwhelming contributing only +2.8%. However, the most notable callout (and red flag) is the absence of any comment on inventories. Last month the company dropped the verbiage that inventories were “in-line with sales trends,” this month they failed to mention inventory altogether. With the least attractive sales/inventory spread among its peers (KSS, M, JWN – see chart below), it looks like JCP is likely to maintain its laggard status over the near-term.

- TGT also came in weaker than expected and again at the low end of their May comp guidance. We noted last month that grocery trends would be one of the more scrutinized items in this month’s release given that it’s a key driver of the +200-400bps in incremental comp and coming off a huge April. Posting a mid-teen increase is positive on the margin and suggests that strength in April was not an aberration. After riding this one down with a bearish view over the last several months, we have turned incrementally more positive on the name and think we’ll start to see a reacceleration in the top-line over the next 12-months.

- Category performance also supports our view that discretionary spending has indeed tightened with grocery/food highlighted as the top performing category at both COST and TGT, while home and electronics were cited as common underperformers with price deflation to the tune of 10% in TVs still present. Additional category strength was noted in accessories (JCP, SKS, KSS, ROST, ZUMZ, TGT) and women’s apparel (COST, JCP, SKS, ROST). While recent strength in men’s apparel was noticeably absent at most retailers both JWN and SKS highlighted strength in men’s during the month.

- COST again confirms our view on inflation with both fresh foods and food and sundries still up in the LSD-MSD range. In addition, gas contributed +4% and +4.4% to SSS for both COST and BJ respectively. Our view is that while this won’t be the first or second crack in the retail industry’s margin equation, it will add to the pain as the retailers choose to capture consumables inflation costs at the expense of discretionary product margins. (i.e can’t take up price on milk, eggs, and chicken – so look to extract margin in categories like underwear, shirts, toys, etc…).

- Weekly trends suggest that traffic was clearly stronger in the 1H of the month with sales strongest in week 2 and slowest in week 4. Interestingly, TJX was the only company to note that more favorable weather at the end of the month has lead to a pickup in June.

- On a regional basis, performance was more mixed than we’ve seen in quite some time. The most consistent callout was strength in the Southeast (COST, KSS, ROST, TGT, JWN) and both CA and FL at the state level while the Midwest was the most varied (positive: COST, TGT, JWN; negative: GPS and TGT). Yes even TGT straddled the fence calling out portions of the Midwest on both sides.

Casey Flavin

Director