R3: REQUIRED RETAIL READING

June 1, 2010

RESEARCH ANECDOTES

- The latest retailer to crack, JOSB not only came up shy on the top-line, but also margins with higher than expected SG&A expense driven by higher shipping costs and occupancy deleverage. The real callout here is inventories up +18% on +9% sales growth resulting in a sharp negative SIGMA turn. This isn’t the first-time JOSB has struggled with inventories and chances are it's not likely to be a one-off event with inventory compares getting even tougher next quarter.

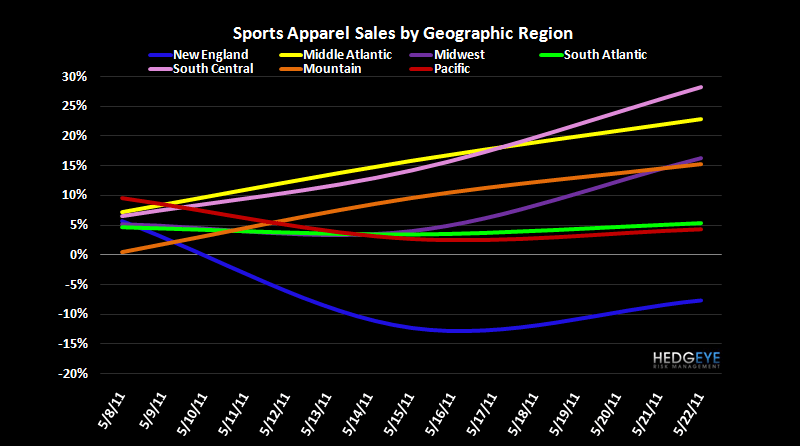

- While we aren’t going to have the regional trends for the last week in May until tomorrow, if the first three weeks are any indication, expect the Northeast to be a common negative highlight on tomorrow’s sales calls.

OUR TAKE ON OVERNIGHT NEWS

Simpson to Take on Tweens - With an assist from her younger sister Ashlee, Jessica Simpson is tapping into the tween category. The Camuto Group, which holds the master Jessica Simpson license, has signed an agreement with The Jones Group Inc. to design, develop, produce and distribute Jessica Simpson tween apparel as part of its lifestyle offering of the Jessica Simpson Collection. This agreement expands the business the two companies are already doing with Jessica Simpson Jeanswear and Jessica Simpson Sportswear, both of which are licensed to Jones. The new collection, which will be available in stores in the fourth quarter, will be geared to the fashion-forward tween, sizes 7 to 16. According to Camuto, the tween offering will include footwear (licensed to Stride Rite) and outerwear (licensed to Fleet Street), in addition to the sportswear, jeanswear and activewear. The sportswear line will be available at about 400 doors of specialty and department stores in the fourth quarter. The company has already lined up orders with Dillard’s, Lord & Taylor, Macy’s, Belk, Von Maur, Bon-Ton and The Bay in Canada. Wholesale prices are $15.50 for core jeans; $15.75 to $18.25 for fashion bottoms; $8.50 for graphic Ts; $10.75 to $14.75 for fashion knits, and $14.75 to $20.75 for sweaters, fur vests and pleather jackets. Jones launched Simpson’s jeanswear collection last June (650 doors), and will introduce sportswear at retail this fall (450 doors). Jack Gross, chief executive officer of the Jones Jeanswear Group, projected sportswear and jeanswear combined to ring up $150 million to $200 million at retail annually by next year, evenly split between the two categories. Down the road, sportswear is forecast to outpace jeanswear. The tween line is expected to generate $20 million in retail sales in 2012, said Gross. <WWD>

Hedgeye Retail’s Take: While the tween line is projected to be only a fraction of the size of Simpson’s core lines initially, the key callouts here are 1) it’s yet another line extension (which JNY desperately needs), 2) it targets an entirely untapped consumer for Simpson and one that we’d suspect she still resonates with from her pre-fashionista music days, and 3) if done right, this segment could actually challenge if not surpass the meteoric growth rate realized in the jeanswear and sportswear businesses. Given the success of previous lines, this will be one to watch in 2012.

Hilfiger to Launch Tommy Girl - The Tommy Hilfiger Group, wholly owned by Phillips-Van Heusen Corp., will launch Tommy Girl, a sportswear collection for young women. Tommy Girl, which is licensed to RVC Enterprises LLC, will be available at 150 doors of Macy’s in the U.S., beginning in July. The collection, aimed at 12- to 18-year-olds, will be housed in its own shop environment in the junior area of Macy’s and will reflect Hilfiger’s preppy with a twist heritage. The line features oxford cloth shirts, polos, peacoats and denim jeans. “Younger audiences have shown a strong demand for the brand,” said Gary Sheinbaum, chief executive officer of Tommy Hilfiger North America. “In leveraging our relationship with Macy’s to distribute Tommy Girl, we are able to offer product to this younger consumer and in more locations than we would through our retail business model.” "I am [pleased] about the new Tommy Girl collection,” said Tommy Hilfiger. “Tommy Girl is our response to consumers wanting quality clothing at affordable prices.” Tommy Girl’s retail prices will range from $32 for T-shirts to $129 for outerwear. <WWD>

Hedgeye Retail’s Take: It appears that competition within the young girls segment is heating up with Simpson and Hilfiger both announcing their respective entries into the space. While the target consumer is decidedly different with Simpson going edgy compared to Hilfiger’s classic prep style and price points at Tommy nearly 2x, both lines will be carried at Macy’s. Following the launch of Material Girl last fall, Macy’s is proving to be a key destination for the tween’ish’ demographic.

WMT South African Deal Approved - The South African Competition Tribunal on Tuesday ruled that the Wal-Mart and Massmart merger can proceed. The tribunal accepted the conditions proposed by Wal-Mart and Massmart, including a 100 million South African rand ($15 million at current exchange) supplier development fund, no merger-related staff reductions for two years and continued recognition of the South African Commercial, Catering and Allied Workers Union for three years after the merger. The tribunal also said preference should be given to hiring 503 workers that were let go prior to the merger proposal’s announcement. Wal-Mart Stores Inc. in November acquired 51 percent of the Johannesburg-based retailer for 17 billion South African rand, or $2.36 billion. The Massmart board unanimously approved the transaction and the deal in January was approved by the necessary 75 percent of shareholders. All it needed to proceed was approval by the South African competition authorities. With the last obstacle removed, Wal-Mart said it intends to provide Massmart with increased financial stability and support to continue strengthening its presence in Africa. The combined Wal-Mart-Massmart entity is planning “significant new store openings that will create thousands of union jobs in South Africa,” Wal-Mart said. In addition, the Massmart food business is expected to grow more than 50 percent over a five-year period. <WWD>

Hedgeye Retail’s Take: Completing its biggest deal in more than a decade, Wal-Mart is now truly global penetrating the last remaining continent without the leading EDLP player. While upfront investment is considerable, we suspect it will be some time before we see this deal move the needle.

KKR Acquires Academy - Academy Sports & Outdoors is under new ownership. The Katy, Texas-based retail chain announced Tuesday it was acquired by New York private equity firm Kohlberg, Kravis, Roberts & Co. in a move that Academy President Robyn Faldyn said would accelerate growth for the athletic and outdoor-focused retailer. The current owners, the Gochman family, will retain a minority stake in the 131-door chain, which operates primarily in the southeastern U.S. and saw $2.7 billion in revenue last year. Terms of the deal were not disclosed. KKR is an international private equity firm with $61 billion in assets. As part of the agreement, Faldyn also will take on the CEO role, currently held by Chairman David Gochman, when the deal closes in six to eight weeks. Faldyn said the chain plans to open 12 stores in both new and existing markets in 2011, and he expects KKR’s involvement will facilitate even more expansion. “The transaction with KKR will give the company more flexibility and access to capital to more aggressively pursue additional store growth along with our focus on upgrading our technology and distribution infrastructure,” he said. <WWD>

Hedgeye Retail’s Take: Another sporting goods retailer falls into the hands of private-equity. With only 131 stores, 12 store growth in ’11 is on the more aggressive side relative to its peers – something we’d expect to accelerate as KKR looks to drive sales ahead of an eventual IPO. With DKS having missed the opportunity to grab the Academy when it could, it will be forced to compete with KKR over real estate out west and perhaps revisit the potential for a strategic deal down the line albeit at higher prices.

Barneys Expands e-Commerce Reach - Barneys New York says the e-commerce channel is the fastest growing part of its business and wants to keep the momentum going by playing on its international recognition. The luxury retailer has ramped up shipping online orders off barneys.com to 90 countries including Canada, South Korea, the U.K., Australia and China, from just the U.S. at the beginning of the year. “We did a phase-in process beginning at the tail end of February, with 20 countries at a time, to make sure we were up and running and could handle it,” Daniela Vitale, chief merchant and executive vice president of Barneys New York, told WWD. Asked what countries are generating the most orders, Vitale replied: “Canada is very big, and we’ve had a lot of interest from Australia due to the beneficial exchange rate.” She also cited France, Germany, Italy and Mexico, which is “quite shocking considering the huge tax issues there....There’s been pretty much a great mix, but no real activity from South America aside from a little bit from Brazil but not much else yet. We haven’t done anything yet in terms of marketing. We would partner with Google to do some search-related things that apply to Brazil” and other countries. Vitale said international tourists represent one-third of Barneys’ active customer base, and that in some flagships, like Madison Avenue and Beverly Hills, it’s closer to a 50-50 split. With the increase in foreign shipping, Barneys is building up inventories but Vitale assured it’s an increase commensurate with sales projections. <WWD>

Hedgeye Retail’s Take: At some point, it becomes more economic to establish global POD to handle volume and mitigate cost, but with well over 1/3 of its business tied to tourists, Barney’s retention cost is considerable. Strong demand out of Canada and Germany are no surprise, but Mexico? Perhaps there’s some truth to ‘if you ship it, they will come.’

AFA Introduced to Senate - The Affordable Footwear Act has been introduced in the US Senate by Senator Maria Cantwell (D-WA) and Senator Roy Blunt (R-MO) in a bid to reduce costs for outdoor industry footwear makers and their customers while supporting US production of outdoor shoes and boots. The Act would create a four-year suspension of many of the disproportionately high import tariffs, some as high as 37.5 percent, that are assessed against outdoor footwear. The bill also ensures US manufacturing that is currently underway in this area remains globally competitive by excluding any product with American production and preventing tariff engineering that undermines US footwear producers. The bill is also temporary so that domestic production can be reevaluated after four years and products removed where appropriate. It is estimated that $800 million in duties on children’s and low-cost shoes will be eliminated should the bill be passed. The goal is to ease the tax burden on families hurting in the current economy. <FashionNetAsia>

Hedgeye Retail’s Take: Back for another go attempt, but this time the Affordable Footwear Act has been introduced to the Senate – a step further than it’s ever been. This would undoubtedly help the lower end footwear retailers that are more price sensitive if passed. While unlikely to result in lower prices, we suspect that retailers will be less apt to pass increasing material costs through if cost relief in the form of lower tariffs comes to fruition.