TALES OF THE TAPE

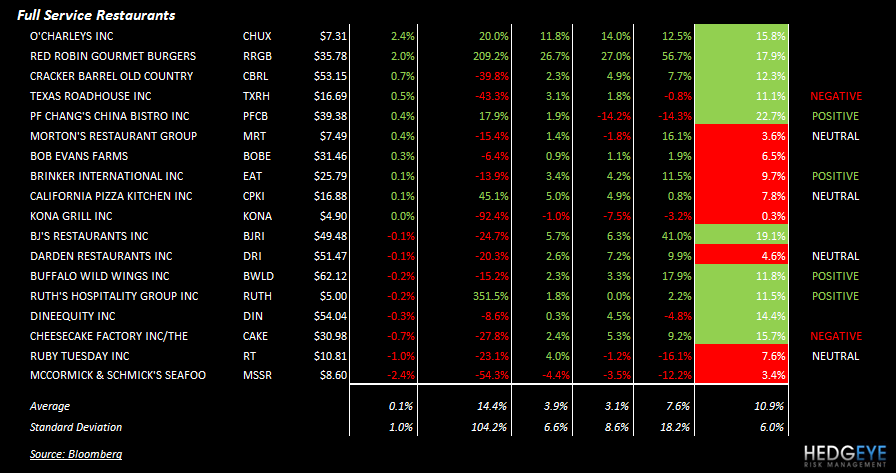

- CBRL - Q3 EPS of 58c misses by 8c. Revenue of $582.5m misses.

- BEEF PRICES - Cash cattle have fallen 13 percent since the spring highs, and the decline represents $150 reduced value in the total price of a market-ready steer. Demand for both pork and beef was called gloomy last week and lower fed cattle prices helped packers regain some margins on slaughtering and processing. The seasonal expected boost in demand has failed to materialize for beef - CattleNetwork

- Sandwich giant Subway is testing a more upscale format called Subway Café, which the company hopes will address the needs of franchisees looking to open in office buildings and other more high-end venues - NRN

- The National Restaurant Association Restaurant, Hotel-Motel Show kicks off Saturday at Chicago's McCormick Place.

- RRGB - Strong follow thru from last week performance on accelerating volume

- GMCR and PEET continue to trade higher on strong volume

- JACK - continues to struggle to gain traction

- CHUX - Strong follow thru following a better that expected quarter

Howard Penney

Managing Director