This note was originally published at 8am on May 17, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Faith is an island in the setting sun, but proof is the bottom line for everyone.”

-Paul Simon

My wife Laura and I had a wonderful time at a fundraiser in Greenwich, CT last night. Our good friends were raising money for The Bowery Mission. Founded by Albert Gleason Ruliffson in 1879, it was one of the first missions established for the homeless in America.

The United States of America is one of the most generous lands that our world has ever known. If you give Americans an opportunity to give, they often will. If you give them a chance to lead, many of them do so by example. There is a faith in this country that cannot be centrally planned out of our hearts.

Faith, accountability, and trust. While these principles may not always resonate intuitively with being “bearish” about a market price, there’s an important investment point to be made here. You have to be able to separate your patriotism, religion, and confirmation biases from the daily risk management discipline that will separate you from the flock. You either have faith in your process, or you don’t.

In his morning tweet, the Dalai Lama complimented this point by reminding us that, “reliable and genuine discipline comes not from repression, but from an understanding of all the whys and wherefores of our actions.”

The Whys and Wherefores of what gets you to buy, sell, and hold; the Whys and Wherefores of what gets you to trust, love, and give; the Whys and Wherefores of what it is that gets you out of bed every morning to do what it is that you do…

It’s all there.

No matter what we do in this profession. No matter where we go in this life. The answers to these questions define and shape not only our individual character, but our collective culture.

Back to the Global Macro Grind…

Having authored the Global Macro theme of Growth Slowing As Inflation Accelerates, I know exactly why it is that I have been taking down my gross exposure and tightening my net exposure (longs minus shorts) for the last 3 weeks.

Last week I sold all of our Oil. This week I sold all of our Gold. We now have a zero percent allocation to Commodities in the Hedgeye Asset Allocation Model.

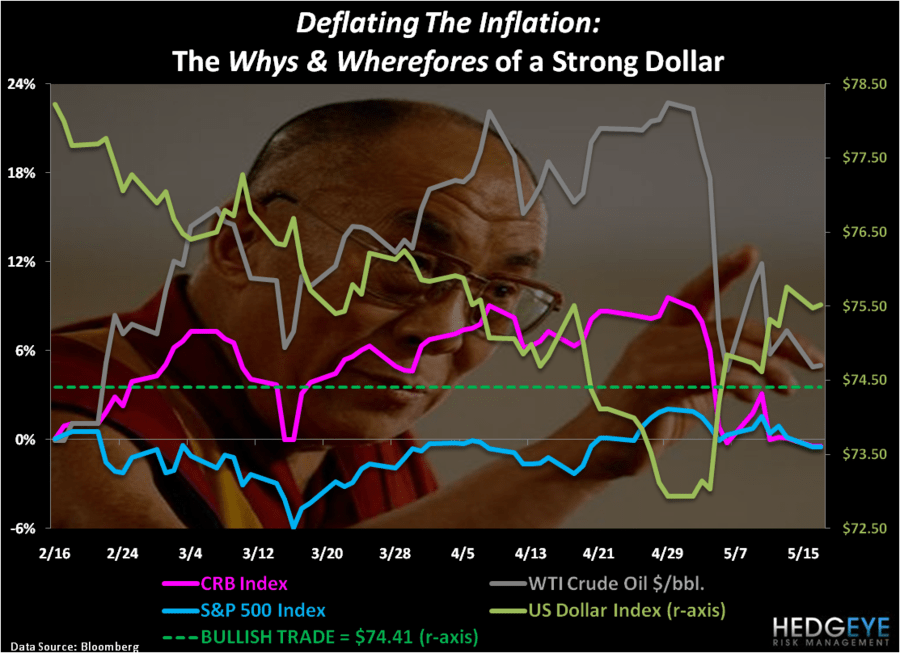

We’ve written and talked about the similarities between the US Currency Crashing to lower-lows in Q2 of 2008 and 2011 for enough time now that you know that I will not move away from my risk management discipline of respecting The Correlation Risk between US Dollars and everything that’s highly correlated to them.

If you are a Risk Manager, the month of May has reminded you of the following realities associated with a US Dollar arresting its decline (USD Index TRADE line of $74.41 resistance is now immediate-term support – do not be short the USD here):

- Stocks stop going up

- Commodities stop going up

- US Treasuries stop going down

For us, this is good. In terms of how I am positioned in May, that is.

- US and International Equity Exposure = 9%

- Commodities Exposure = 0%

- US Treasury Exposure = 15%

The Whys and Wherefores as to what got me into these positions are reconciled every day with the same repeatable mechanism that got us to make our US crash call of 2008 and the “May Showers” correction call that we made in April of 2010. Whether I am grumpy or glad, our research and risk management process stays the course.

Are the inverse correlations associated with US Dollar moves going to hold forever? Of course not – correlation risk is never perpetual. Could they matter for far longer than the biggest net long position in hedge fund history can be rationally unwound? Mr. Macro Market is going to have to tell us the answer to that – and, in the meantime, I have plenty of time to buy things back.

Why and Wherefore should I have faith in this process?

Because when it works for me, I know why – and when it doesn’t, I understand wherefore I should evolve it.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1474-1499, $93.67-$100.12, and 1327-1336, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer