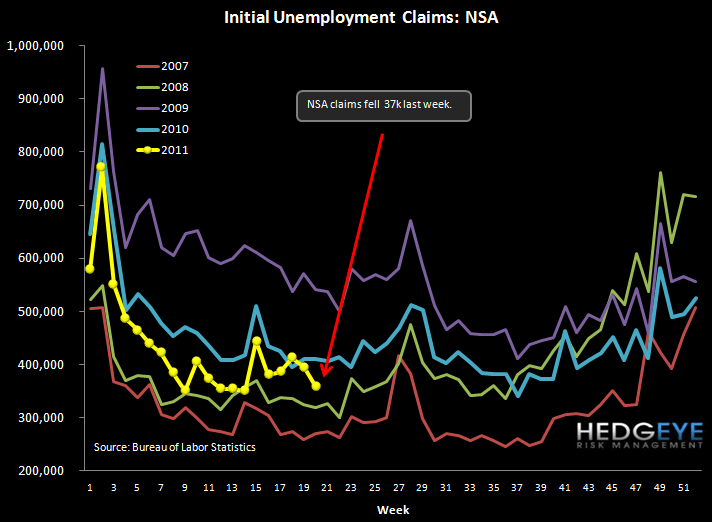

Initial Claims Drop 25k

The headline initial claims number fell 25k WoW to 409k (29k after a 4k upward revision to last week’s data). Rolling claims rose 1.25k to 439k. On a non-seasonally-adjusted basis, reported claims fell 37k WoW, an atypical seasonal move.

Despite the strong print in reported claims, rolling jobless claims are now up for the past 11 weeks, and even more importantly we remain at the YTD high in rolling claims. We use claims as our primary frequency determinant in thinking about losses for the consumer book of balance sheet dependent financials. The last time we saw such an inflection in the trend in jobless claims was summer 2010, a period in which the XLF lost roughly 20% of its value. To this end, take a look at our fifth chart showing the overlay of jobless claims with S&P 500. The current divergence is among the widest we've seen in the last few years suggesting that either the market is due for a significant correction in the near-term or claims should fall precipitously in the next few weeks.

Two relationships that we are watching closely are the tight correlation between the S&P and claims and between Fed purchases (Treasuries & MBS) and claims. With the end of QE2 looming, to the extent that this relationship is causal, it is quite concerning.

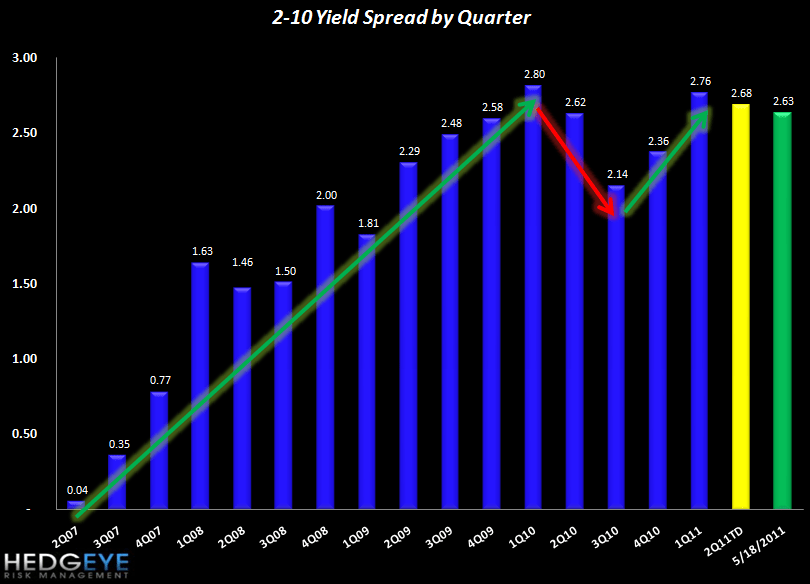

Yield Curve Remains Wide

We chart the 2-10 spread as a proxy for NIM. Thus far the spread in 2Q is tracking 8 bps tighter than 1Q. The current level of 263 bps is 1 bps wider than last week.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur