TODAY’S S&P 500 SET-UP - May 18, 2011

US stocks have been down for the last 3 days and the last 3 weeks – and after taking a good hard looking at the intermediate term TREND line of 1319 in the SP500, we should see another low-volume bounce to lower-long-term highs; resistance = 1340. As we look at today’s set up for the S&P 500, the range is 17 points or -0.75% downside to 1319 and 0.53% upside to 1336.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -483 (+584)

- VOLUME: NYSE 971.43 (+7.07%)

- VIX: 17.55 -3.78% YTD PERFORMANCE: -1.13%

- SPX PUT/CALL RATIO: 1.89 from 1.88 (+0.77%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.96

- 3-MONTH T-BILL YIELD: 0.04%

- 10-Year: 3.12 from 3.15

- YIELD CURVE: 2.57 from 2.61

MACRO DATA POINTS:

- MBA mortgage applications index up 7.8% week ended May 13; Refis up 13%, largest gain in 10 weeks; Purchases fell 3.2%; Avg. 30-yr fixed rate 4.60%, lowest since end Nov., vs 4.67% prior week

- 10:30 a.m.: DoE Inventories

- 11:30 a.m.: U.S. to sell $5b 56-day cash mgmt bills

- 2 p.m.: FOMC Minutes

- 7 p.m.: Fed’s Bullard speaks in New York

WHAT TO WATCH:

- U.S. Treasury Secretary Geithner said the IMF needs to name an interim leader because Strauss-Kahn is “obviously not in a position” to run the fund; Europe seeks to keep top position

- EU Commission completes quarterly review of EU/IMF financial assistance program to Ireland; authorizes the release of the second installment

- Bullish sentiment decreases to 45.6% from 51.1% in the latest US Investor's Intelligence poll

- Banking groups opposed to simpler mortgage forms - Bloomberg

- Fed wants to subject US banks to annual stress tests - FT

- Russian President Dmitry Medvedev says he doesn’t exclude that some oil companies are colluding to increase prices for gasoline on the domestic market.

- Google’s First Bond Sale Drew Orders Exceeding $10b: WSJ

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Milk Rally Causing Higher Prices at Wal-Mart Also Spurring Gains in Output

- Commodities Rebound on Outlook for Stronger Demand From Emerging Markets

- Oil Rises From Three-Month Low as Supplies of Cushing Crude, Gasoline Drop

- Copper Climbs to One-Week High as Commodities, Equities Rebound From Drops

- Corn Advances for Fifth Straight Day as Wet Weather May Delay U.S. Seeding

- Gold Gains for First Day in Four on Weaker Dollar, European Debt Concern

- Drought in China’s Hubei Withers Rapeseed, Wheat Crops, Delays Plantings

- Oil, Gold Will Drive Rebound in Commodities on Shortages, JPMorgan Says

- Coffee Rises on Concern About Limited Supplies; Sugar, Cocoa Prices Gain

- Silver May Slide 16% After Breaching 100-Day Average: Technical Analysis

- Drought Spells EU Power Squeeze as Nuclear Reactors Halt: Energy Markets

- Copper Demand From China’s Cable Makers May Double as Cities, Grids Expand

- Bunge Offers $138 Million for Tully Sugar, Above Louis Dreyfus-Backed Bid

- India Shipping to Gain From Japan $30 Billion Steel Bill: Freight Markets

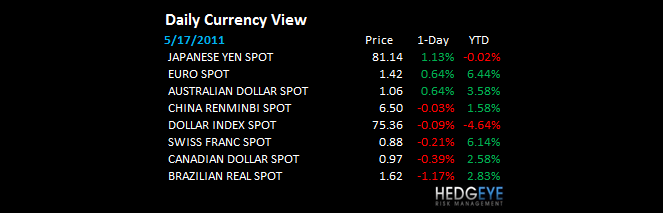

CURRENCIES

EUROPEAN MARKETS

- UK Mar ILO unemployment rate +7.7% vs consensus +7.8% and prior +7.8%; UK Apr claimant count +12.4k vs consensus unchanged

- BOE keeps 6-3 vote in May to hold rates at record low

- Greek Banks Surge as ECB Officials Rule Out Debt Restructuring

- Irish Household Wealth Rises 6% in Q4 2010 , Central Bank Says

ASIAN MARKETS

- Asia was strong overnight

- Vietnam was a negative divergence down 2.03%

- Japan March tertiary activity index (6.0%) m/m – the biggest drop in 22 years -- to 93.5.

MIDDLE EAST

Howard Penney

Managing Director