No change to HK$22-24 BN projection for May.

Macau table gaming revenues totaled HK$11.7 billion for the first 15 days of the month. The pace slowed dramatically from Golden Week with average daily table revenues falling from HK$899 million in the first 10 days down to HK$528 million. A drop off is not surprising given the Golden Week impact on the first 10 days. We still think total gaming revenues projects out in the HK$22-24 billion range for the full month (+33-45% YoY growth), including slots. Absent the Galaxy Macau contribution (opened yesterday), which is not in these numbers, we would be leaning toward the low end of the range. However, Galaxy Macau is likely to spur incremental visitation so we are sticking with our original projection.

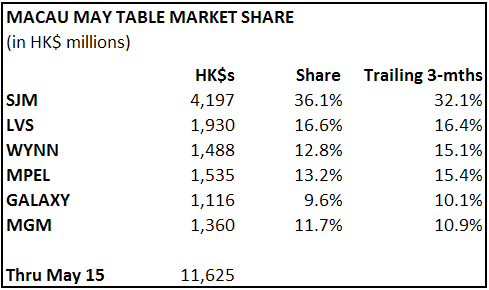

The only significant market share move from last week was Wynn, giving up significant share mainly to SJM. No doubt luck played a role but we are starting to wonder if WYNN can maintain its stock price momentum in the face of lower market share, new competition from Galaxy Macau, slowing market growth, and the later opening date of Wynn Cotai to 2015.