April more than just confirming the Feb/Mar acceleration.

While it’s not quite Macau-esque numbers, regional gaming revenues for April are coming in strong. Iowa, Indiana, and yes, even Illinois recorded impressive April results, despite the destructive flooding, tornadoes, and other forces Mother Nature threw at the states. Throw in the stubbornly high unemployment across the country and this has been an uphill battle.

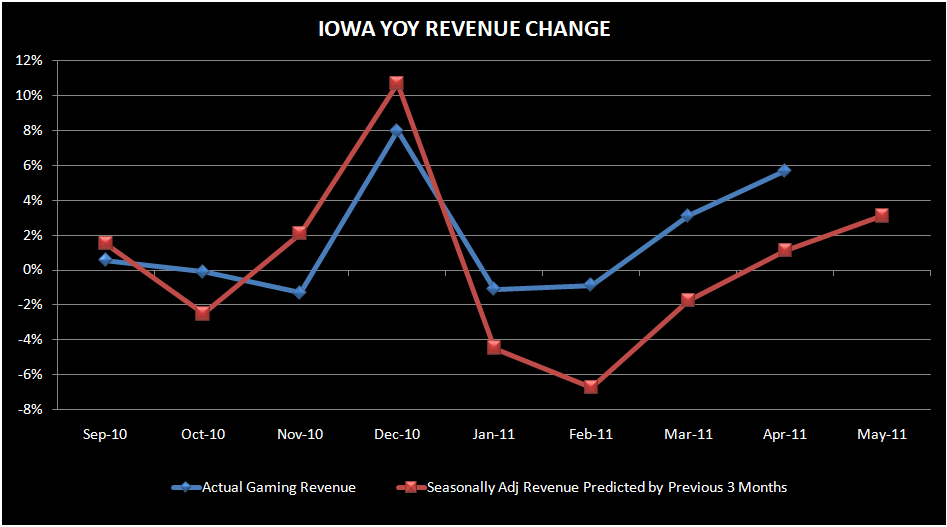

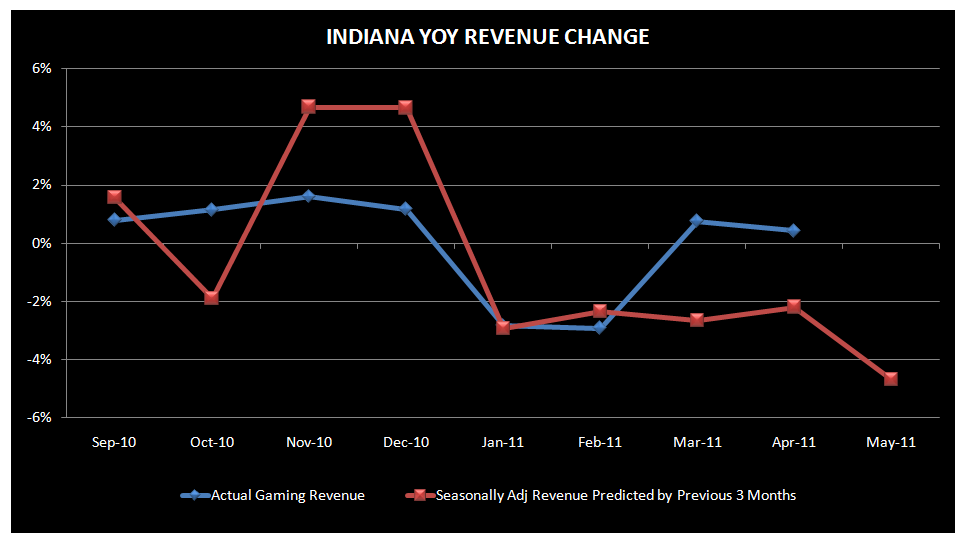

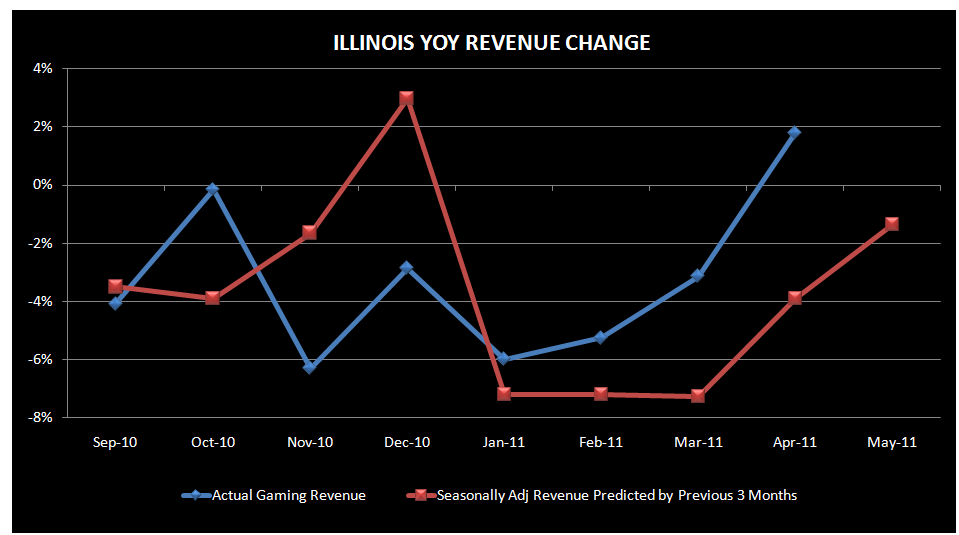

The charts below show sequential revenue for the 3 “I” riverboat markets in April compared to where revenue would’ve grown had sequential revenue levels ( for the prior 3 months adjusted for seasonality) continued. April furthered the Feb/Mar acceleration and growth accelerated relative to Q1. It’s particularly notable for Illinois which hasn’t seen YoY growth since April 2010.

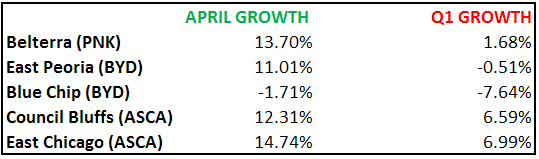

As Q2 gets under way, we continue to like the regional operators, particularly ASCA, BYD and PNK. As can be seen in the table below, in the states that have reported revenue, those companies’ properties performed much better in April than in Q1. We think there is a high probability of Q2 earnings beats.