This note was originally published at 8am on May 04, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“We are willing to accept almost any explanation of the present crisis of our civilization except one.”

-F.A. Hayek

That’s an important quote from page 65 of a chapter that Hayek wrote in “The Road To Serfdom” titled, “The Abandoned Road.” As I take a step back and think about what a tremendous opportunity our profession has had to learn about real-time risk management and the interconnectedness of Global Macro markets in the last 3 years, it’s somewhat sad to realize that consensus hasn’t been paid to learn much.

What we get paid to do is chase short-term returns. The Bernank perpetuates this performance pressure by marking the short-term “risk free” rate to model (or the ZERO bound) and, as a result, this gargantuan experiment of starving savers of returns imputes 3D Risk (3 D’s) into markets:

- The Dare – zero percent rates dare you to chase yield across asset classes where you can justify it

- The Delay – zero percent short-term financing for banks delays the financial restructurings that free market prices would impose

- The Disguise – zero percent expectations disguise the interconnected risks associated with carry trading, correlation risk, etc

The Disguise is the one that can really nip a perma-bull in the butt. That’s the one that, allegedly, “no one can see coming.” That’s the one that is being revealed real-time. In terms of making excuses for being willfully blind to it, this time is different because we have a modern day technological innovation in financial market transparency – it’s called Twitter.

Going back to Hayek’s aforementioned point, I think that’s the one thing our professional politicians do not get paid to understand. That would be called accountability. The Disguise in financial markets is The Correlation Risk – and while his original text was addressing a different kind of socialism and Big Government Intervention in 1944, I still think what Hayek goes on to say about explaining our perpetual financial “crisis” is very appropriate:

“… that the present state of the world may be the result of genuine error on our own part… and that the pursuit of some of our most cherished ideals has apparently produced results utterly different from those which we expected.”

With another 78 Billion Bailout Euros being extended to the government of Portugal this morning, Spain seeing unemployment spike to 21.3% (new all-time highs), and Americans staring down $5/gas at the pump with jobless claims re-accelerating, wasn’t that some advice our “independent central bankers” and fiscal spenders should have considered?

Independent research? Should we just never mind silly old school things like the American Constitution or what John Locke wrote On Liberty 80 years before Hayek penned his original counter-points to Keynes? Just buy-the-damn-dips, chase yield, and believe that it’s going to end well this time?

Back to The Correlation Risk and playing the game that’s in front of you…

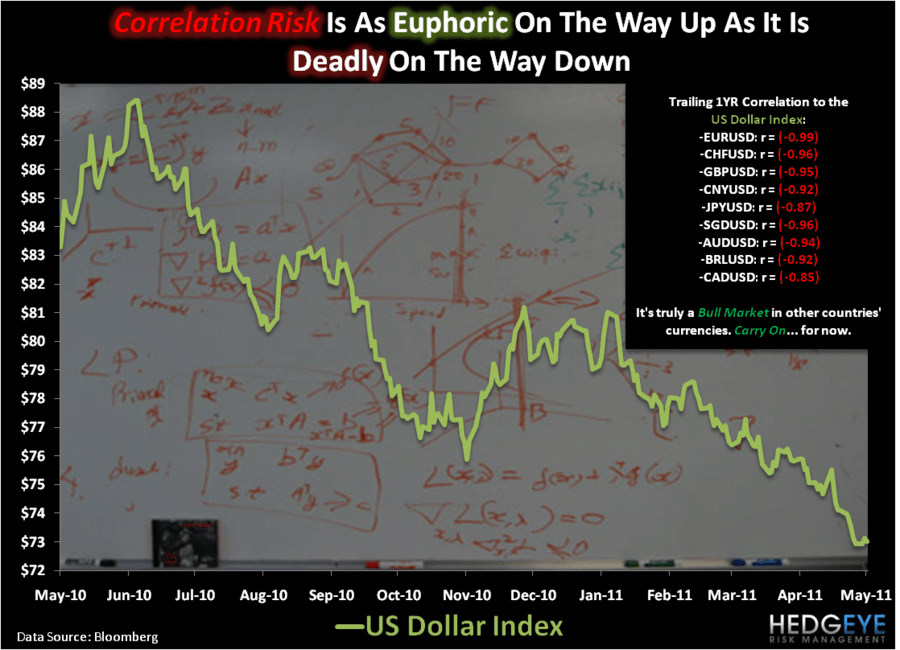

Given that the US Dollar is the #1 factor we are talking about when we say Global Macro Correlation Risk (say it central planners -“who –ho-wns de Campaigner-in-Chief?”), let’s get a real-time price check on how that looks on our intermediate-term TREND duration (3 months or more):

- Crude Oil = -0.92

- Gold = 0.94

- Silver = -0.94

- Coffee = -0.84

- Pork Bellies = -0.92

- CRB Commodities Index = -0.87

I know, I know – The Bernank calls this commodity stuff that you put in your cars, stomachs, and teeth “transitory”…

How about the intermediate-term TREND inverse-correlations between the US Dollar Index and relatively larger matters like countries?

- USA (SP500) = -0.82

- Brazil = -0.88

- Mexico = -0.82

- Germany = -0.93

- Spain = 0.94

- Russia = -0.85

- China -0.85

- South Korea = -0.90

- Australia = -0.91

How about the obvious, the intermediate-term TREND inverse correlations between the USD spot price and the world’s currencies?

- Euro = -0.99 (not a typo)

- Swiss Franc = -0.96

- British Pounds = -0.95

- Chinese Yuan = -0.92

- Japanese Yen = -0.87

- Singapore Dollar = -0.96

- Aussi Dollar = -0.94

- Brazil’s Real = -0.92

- Canadian Dollar = -0.85

Really? Yes, President Obama – really. This Correlation Risk math checks out from Hawaii to Havana. We get it. Anyone gaming Geithner and The Bernank get it. The Chinese get it.

In the Peoples Bank of China’s Q1 Monetary Policy Statement last night (published on China’s website – not to be politically pandered to on 60 Minutes this Sunday or at a US Federal Reserve Presser), this is what the Chinese had to say about all of the aforementioned real-time prices:

“Stabilizing prices and managing inflation expectations are critical… given the loose monetary policies of major economies and gradual recovery of the global economy, commodity prices and global inflation expectations are rising significantly.”

“Significantly” versus “transitory.” Academic dogma versus independent analysis. Government storytelling versus Correlation Risk. It’s all out there folks. It always has been – and, sadly, when it comes to US policy, so has Hayek’s “Abandoned Road.”

My immediate-term support and resistance lines for Gold are now 1525 and 1565, respectively. For oil I’m at $109.39 and $114.21 – and for the SP500, my immediate-term support and resistance lines are now 1349 and 1373, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer