Position: Long British Pound (FXB)

Conclusion: We continue to flag our concurrent call of Inflation Accelerating with Growth Slowing across global economies. The UK remains one economy mired in this trend, with elevated levels of inflation persisting and choking off growth. Today’s UK Producer Price Index for April shows an upward acceleration in Input costs to 17.6% Y/Y (versus 14.8% in March) and Output prices slowed 30bps to 5.3% Y/Y versus the previous month. In total, we continue to note that increasing input costs should weigh to the upside on output costs, and therefore continue to hamper consumer spending, confidence, and ultimately growth. We expect UK headline inflation, currently at 4.0% in March Y/Y, to accelerate over 2011 as we expect commodity prices to remain elevated over the medium term and due to the effect of “imported inflation”, or the impact of the weakness in the GBP-EUR over the last three years to heighten inflation pressures, especially considering that the UK imports roughly 50% of its goods from the Eurozone.

With no great surprise, energy and food prices were the largest inflationary components contributing to gains in input and output prices. Input crude oil gained 37.7% in April versus the 12 months ago period, and home food materials increased 15.4%. Output prices saw the largest gain from petroleum products (up 14.9% in April Y/Y) and food products gained 7.3%. Notably, output tobacco and alcohol prices rose 5.5% Y/Y on increased tax from the government’s budget.

Both the ECB and BoE held benchmark interest rates unchanged on Thursday despite existing inflationary pressures (Eurozone CPI = 2.7% in March Y/Y). While we’ll have to wait for the BoE Minutes for more insight on the bank’s thinking, we remain of the camp that a hike of 25bps is prudent. Trichet’s language in the press conference following the announcement was measured, indicating that monetary policy is “still accommodative” in an environment where there is “upward pressure on overall inflation, mainly owning to energy and commodity prices”. The market largely interpreted these statement as “dovish” for a hike next month in that he did not reiterate such phrases as “strong vigilance” or “prepared to act in a firm and timely manner”.

We’ve seen follow-through selling of the EUR-USD after yesterday’s announcement. In reality, the EUR-USD rose very expediently to just under $1.49 this week and was clearly disconnected with underlying fundamentals. We see immediate term support in the EUR-USD around $1.44, with upside resistance at $1.47, and expect this trade to be volatile given persistent weakness in the USD (despite a bounce yesterday) and uncertainty surrounding the sovereign debt contagion across Europe's periphery.

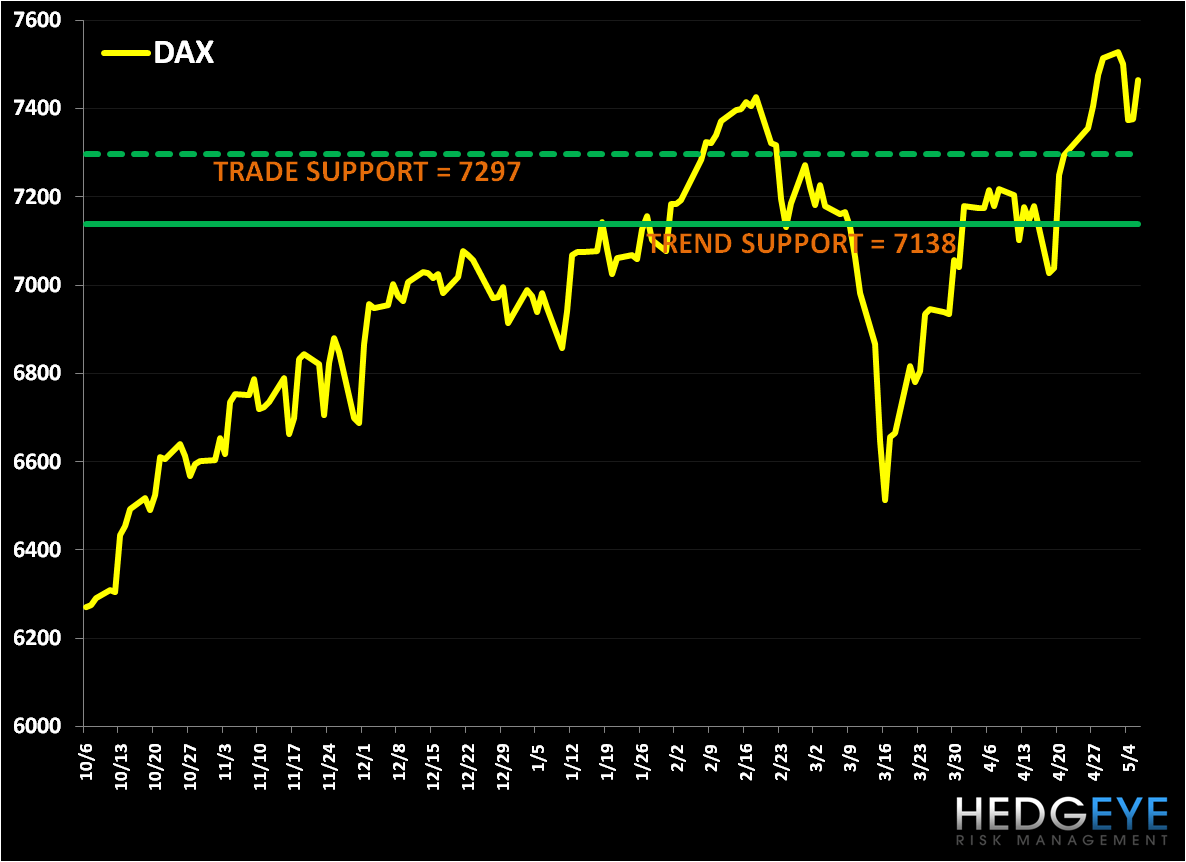

With the unwind of the huge correlation trade to commodities this week, notably Russia’s equity market (RTSI) fell 4.4% week-over-week and Norway’s market declined 3.4%, as Greece blew up (down 4.5% w/w) on debt restructuring fears, we continue to like Germany (via the eft EWG), due to its fiscal sobriety and continued strong fundamental performance. Year-to-date the DAX is up 8.3%, within the top 10 performing global equity markets ytd. Below we highlight our support levels for the DAX. On strength, we’d short Italy (EWI) or Spain (EWP).

Matthew Hedrick

Analyst