This note was originally published at 8am on May 02, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“A little knowledge is dangerous. So is a lot.”

-Albert Einstein

I have a tremendous amount of respect for what Einstein’s independent thinking did for this world, and I love that risk management quote. No matter what you do or do not know this morning, there’s this interconnected Global Macro market’s last price.

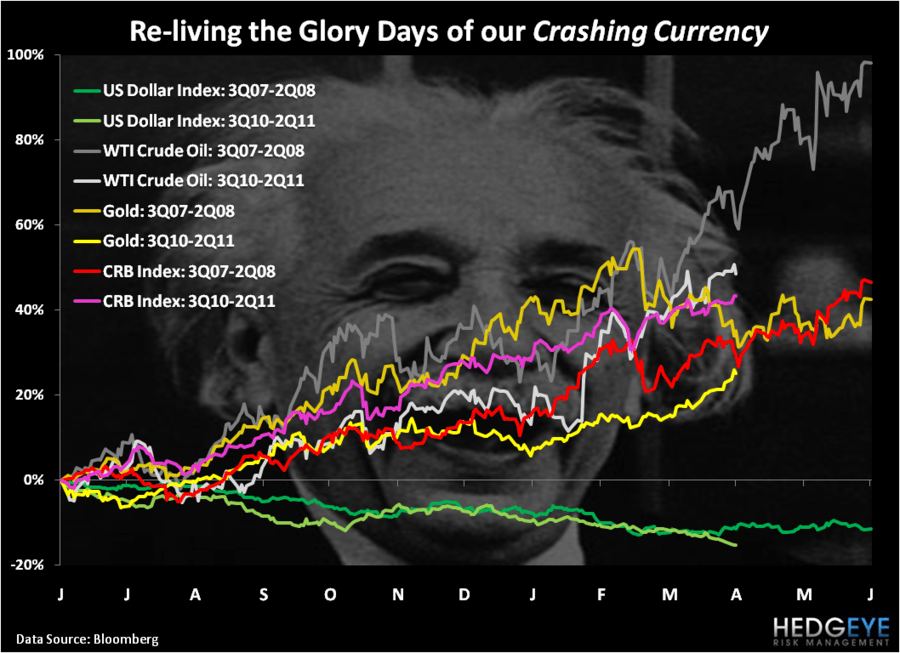

US Dollar driven correlation-risk to currency, commodity, and stocks market prices is running at its highest level since Q2 of 2008. While it’s Dangerous Knowledge to have marked-to-market models on your desktop to help you price this real-time risk, it’s doubly dangerous to summarize the uncertainty associated with this risk with partisan politics.

Since neither the Manic Media nor 90% of Washington/Wall Street got what a Crashing Currency meant in Q2 of 2008, we don’t expect consensus to provide any proactive thought leadership on the risk management topic this time. Whether it’s the US Dollar Index’s relationship to the price of Oil, Gold, or even Volatility, the similarities to the second quarter of 2008 are borderline glaring at this point.

The most market relevant mathematical learning since Einstein’s Relativity has been Chaos and Complexity Theory. It, unlike Efficient Market Theory, accepts uncertainty as a grounding principle. The Keynesian Kingdom’s top brass doesn’t do uncertainty. Allegedly, this time they know exactly what’s going on out there in this gargantuan ecosystem of colliding factors that we call the Global Economy.

What’s going on in Global Macro markets may very well be trivial. Market prices and the trailing correlations that impacted them are historical facts. What’s “not clear” (to quote The Bernank’s favorite career risk management qualifier from last week) is what can be quantified as causal over a long period of time. “Not clear” that is, to the professional politicians who are accountable to the US Dollar Debauchery math.

Here’s what the US Dollar did last week:

- Down another -1.4% week-over-week to a new YTD low

- Down -9.8% from its January, 2011 price and down for the 14th week out of the last 18

- Down -17.5% from June 2010

Wait. What does June 2010 have to do with anything other than making Groupthink Geithner’s record as a credible US Dollar stability guy anything short of a national embarrassment? June 2010 is when the US Dollar was high and prices at the US pumps were a lot lower.

38% lower, actually…

Looking ahead at our kids getting out of school and the summer driving season (hearing from my expert network that both still occurs this year), I think most Americans think a -17.5% meltdown in their Crashing Currency and a +38% tax at the gas pump is a bad trade – for them.

Have no fear however, the President is here in his weekly address (Saturday): “When oil companies are making huge profits and you’re struggling at the pump, and we’re scouring the federal budget for spending we can afford to do without, these tax giveaways aren’t right.”

Right. right…

Meanwhile, Brazil’s President had a different take than blaming Petrobras: “Guaranteeing purchasing power means playing tough on inflation. This is one of the fundamentals of our political economy, and one we’ll never let up on.”

At least there’s a healthy political bid/ask spread out there in terms of what left-leaning President knows the least about Complexity Theory. With American central planners leaning more left than even Europe and Brazil at this point – who would have thunk…

Back to the Global Scorecard – here were the big Global Macro currency and commodity moves associated with the US Currency Crashing week-over-week:

- The Euro = UP another +2.1% to $1.48

- The Chinese Yuan = UP another +0.3% to a new all-time high of $6.49

- CRB Commodities Index (19 commodities) = UP another +0.8% to a new 2-year weekly closing high of 370

- WTI Crude Oil = UP another +1.5% to a new 2-year weekly closing high of $113.93

- Gold = UP another +3.5% to a new all-time high of $1556 (all-time is a long time)

- Copper = DOWN -5.4% at $4.17/lb

Oops, one of these things is not like the other. That’s right, Dr. Copper is reminding those of us with some knowledge about real-time market signals that Global Growth Slows As Inflation Accelerates. Maybe that’s why Chinese and Brazilian stocks lost -3.3% and -1.4% last week, respectively. They no likey The Inflation from The Bernank.

US stocks had another great week, rallying like Japanese equities have for decades to lower-long-term-highs on decelerating volume and scary skew signals. But don’t worry – this Currency Crash thing is cool, like it was in Q2 of 2008, until it isn’t…

In the Hedgeye Asset Allocation Model I proved that I still know a little about learning from my many prior mistakes. I ended the week with my highest invested position of 2011, dropping my allocation to Cash to 34% (at the last immediate-term overbought peak in US Equities I had 62% in Cash, so at least this time is different in that I am riding out more of The Inflation trade’s gains).

The Hedgeye Asset Allocation Model’s week-end allocations are now as follows:

- Cash = 34% (down from 40% last week and 52% in the last week of March)

- International Currencies = 30% (Chinese Yuan, Canadian Dollar, British Pound - CYB, FCX, and FXB)

- Commodities = 12% (Gold, Oil, and Corn – GLD, OIL, and CORN)

- International Equities = 9% (China – CAF)

- Fixed Income = 9% (US Treasury Flattener – FLAT)

- US Equities = 6% (Technology – XLK)

A little knowledge of the Bin Laden takedown would have helped me be levered-long everything US Equities into this week’s start. Having Dangerous Knowledge like that though is a lot of knowledge I’ll pray to do without!

My immediate-term support and resistance lines for Gold are now $1515 and $1557, respectively. My immediate-term support and resistance lines for oil are now $111.47 and $115.61. And my immediate-term support and resistance lines for the SP500 are now 1338 and 1377, respectively.

I plan on taking down both my gross (Hedgeye Asset Allocation invested position) and net long positions (Hedgeye Portfolio: 17 LONGS, 11 SHORTS) into this morning’s newsy strength.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer