This note was originally published at 8am on April 26, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Conditions never persist. They change. Bureaucrats really hate that.”

-Jeffrey Tucker

That’s a quote from a book I read on my family vacation last week, “Bourbon for Breakfast – Living Outside of the Status Quo” (and, no I’m not taking up sipping on Canadian Club by the pool with my morning coffee). Nor do I aspire to ever be a professional politician in America.

Never mind understanding how the interconnectedness of the Global Macro market works, most professional politicians in America don’t get how a market works. Most of them still call this game of Big Government Intervention a “free market.” I call that a joke.

The good news is that a lot of people get the joke. Gaming Policy is the new hedge fund game in town – so game or be gamed. There are higher prices being paid (read: trading commissions) for “one-on-one” access to private meetings with DC bureaucrats than ever before. Sad, but true.

You don’t need inside information if you have a multi-factor, multi-duration, risk management process that flags real-time pricing of these “data points.” Anyone who has traded real-time risk capital in markets knows that someone always knows something…

We’ve titled one of our Q2 Global Macro Themes, “Indefinitely Dovish” (see yesterday’s Early Look) primarily because we think the market is pricing in Bernanke remaining dovish into and out of tomorrow’s FOMC meeting.

When we say “the market”, we mean the globally interconnected one – not just US stocks:

- Currency Market – the US Dollar Index is trading down again this week (for the 14th out of the last 18 weeks) and the Euro is making new highs by the day ($1.46 last) because, for the 1st time since Fed head Arthur Burns was attempting to monetize the US Debt and devalue the dollar (1970s), US monetary policy is more left leaning and dovish than even what the ex-Finance Minister of France is delivering. Jean-Claude Trichet’s comments overnight were explicitly hawkish: “it is extremely important to continue to solidly anchoring inflation expectations in a period which is marked by uncertainties and turbulence.”

- Bond Market – global bond yields continue to push higher as Asian and European central bankers continue to back their rhetoric with rate hike action. Meanwhile, US Treasury yields are breaking down through our intermediate-term TREND support lines of 0.71% and 3.46% for 2-year and 10-year UST yields, respectively. Indefinitely Dovish in America is as dovish does…

- Commodity Market – higher-highs on rallies and higher-lows on corrections for Gold, Silver, and Oil. This is where the US Dollar Devaluation driven monetary inflation is – not in GDP growth oriented commodity pricing (copper, sugar, etc.). With the Saudis trying to talk down oil prices at these levels (calling them “uncomfortable” overnight), WTI crude oil sold off a whopping 50 cents.

And Equities, well – we’re right back to where we were in mid-February where Asian Equities (growth markets) are starting to negatively diverge versus US Equities (the Gaming Policy market). China, India, and Indonesia are rightly worrying about The Inflation that will be perpetuated by a US Currency Crash.

Have no fear however – The Bernank and Groupthink Geithner are here. They have the world’s back on this Currency Crash thing. Having never seen an oil price (including $150/barrel oil) that they thought was inflationary, we don’t think they’re about to start calling $113/oil inflationary now. While Bernanke will acknowledge rising commodity prices tomorrow, he’ll offset that hawkish shift with an incrementally dovish one on US growth.

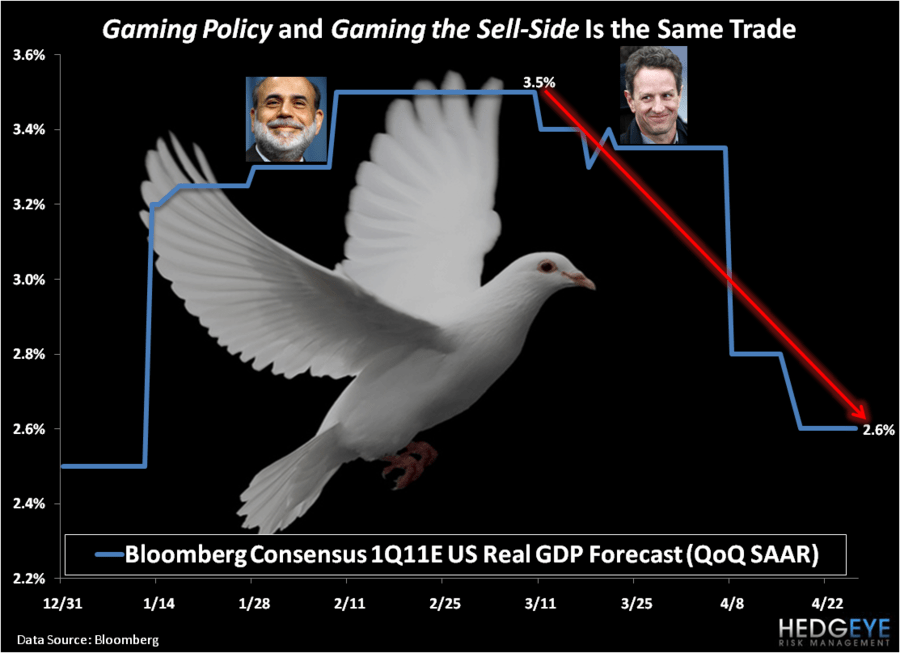

In the Chart of The Day (attached), Darius Dale calls out how super duper the sell-side has become in leading The Bernank and The Groupthinker’s Washington boys to believe that US GDP Growth was going to be all good and fine in Q1 of 2011 – then not so much.

The good news here is that Gaming The Sellside is still one of the oldest and most profitable games in town. They haven’t learned much since missing US GDP Growth Slowing in Q2 of 2008.

If you are looking for leadership on the Currency Crash thing, the President of the United States had this to say over the weekend on gas prices:

“There’s no silver bullet that can bring down gas prices right away…”

Really? If The Bernank raised rates at tomorrow’s FOMC meeting, oil prices would break $100/barrel in a day.

We’d like to remind all of our friends and foes who are still beer-bonging the Keynesian Kool-Aid that there are 3 things that burning your currency at the stake with generational levels of leverage (debt) does to an economy:

- It perpetuates The Inflation priced in US Dollars

- It structurally impairs the sustainability of long-term economic growth

- It dares institutional investors to chase “yield”

No, we’re not saying that these conditions will persist as a perpetually preferred dividend for those of us who are long of The Inflation. Neither are we saying this will end well. What we are saying is that playing the game in front of us right now is the game of Gaming Policy – and, as sad a state of a “free market” as this is, when this game changes, it will change abruptly.

The bureaucrats are going to really hate having to deal with that.

My immediate-term support and resistance lines for the SP500 are now 1320 and 1341, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer