Yesterday in his press conference, Chairman Bernanke highlighted his belief that high commodity prices are simply transitory in nature. He pegged the current rise in oil prices to both supply and demand. On the supply side of the equation, he noted unrest in the Middle East as currently constraining oil production, which is fair point, especially given the sharp decline in Libyan production (normally ~1.8MM barrels per day). On the demand side, he highlighted the continuing growth in demand from emerging markets. Interestingly, he made no mention of monetary policy, or a weak dollar, in the role of commodity price inflation.

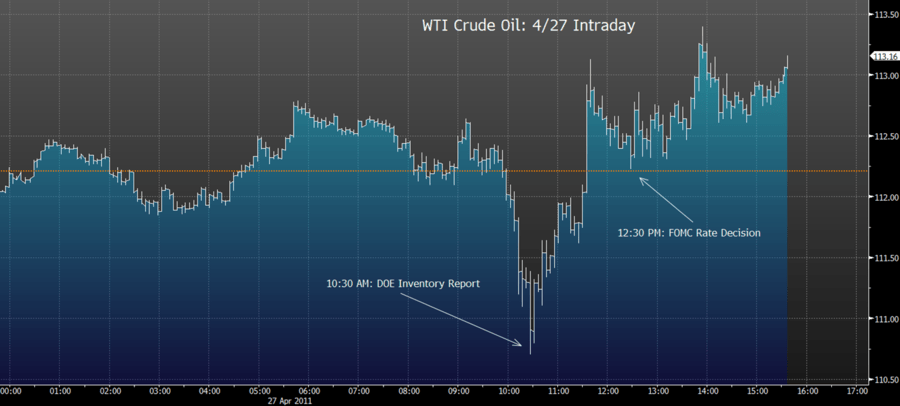

In the chart below, we highlight the intraday move in oil, represented by WTI in this analysis. At roughly 10:30 am, WTI sold off sharply based on a release from the Department of Energy that showed a much larger than expected build in crude inventories. According to the report, inventories were up 1.7% week-over-week, which was just more than 6 million barrels. On a year-over-year basis, the growth in inventories was roughly 1.5%. Clearly, this negative supply data point surprised oil investors and WTI sold off accordingly. Interestingly, two hours later, in conjunction with the release of the Federal Reserve’s statement, oil rallied and completely closed the gap on the prior sell-off related to the fundamental build in inventory.

This rally in oil following both the FOMC statement and Chairman Bernanke’s press conference is not surprising. In the FOMC statement, the Fed noted that residential housing continues to have issues, while, in their view, “measures of underlying inflation continue to be somewhat low.” Both of these points, allow Chairman Bernanke to remain Indefinitely Dovish. Clearly, in the view of the Fed, tightening policy would adversely impact both the tepid recovery of the housing market and economy at large.

In contrast to the Fed’s stance, many central bankers globally continue to either tighten or make hawkish statements. In fact, the ECB has already raised interest rates once YTD. Based on 2.7% inflation readings from the Eurozone in March, it is likely that the ECB again raises rates at their next meeting in July. This is confirmed by Euribor futures and the European interbank rate, which are pricing in an increase in rates in the July / September time frame. This continued widening in global interest rate spreads should further weaken the dollar, which will further support the price of inflationary commodities (oil, gold and silver).

On our March 23, 2011 theme call, “What’s Next For Oil?”, we highlighted three key factors that will drive the price of oil. A brief update on these factors is below:

- Geopolitical – In late March our key takeaway was that civil unrest was set to accelerate in the Middle East and it has done so. Currently, the key hot spots are Libya, Egypt, Syria and Bahrain, with long term outcomes still difficult to determine. Since the March call, this factor has become even more prevalent.

- Supply & Demand – In the United States, which consumes roughly 20% of the world’s oil production, demand is clearly starting to slow as indicated by the most recent data points from the Department of Energy, which showed a much larger than expected build in oil inventory. Conversely, Chinese demand was up 11% year-over-year, which suggest continues strong growth of oil demand out of the world’s second largest consumer, albeit this was a (-300bps) slowdown from February. Of our three factorss, this is the one that is marginally less positive from our long oil call on March 23rd.

- Monetary Policy – Based on Chairman Bernanke’s comments from yesterday, it seems unlikely that the Federal Reserve will raise rates over the intermediate term TREND. In that period, it is likely that most other major economies raise rates at least once, if not more than once. Thus global monetary policy will, over the course of the next few months, move even further away from U.S. monetary policy, which is negative for the U.S. dollar and positive of the inversely correlated price of oil.

In the chart below, we’ve highlighted our quantitative levels on oil, and it remains in a bullish formation. This bullish formation was underscored by yesterday’s price action, which verified our view that the Fed’s dovish monetary policy continues to lag the world and lend support to higher oil prices.

In reality, commodity inflation is about as transitory as our Chairman Bernanke’s Keynesian economic policies. When they change, so too will the price of oil.

Daryl G. Jones

Managing Director