TODAY’S S&P 500 SET-UP - April 28, 2011

As advertised, the Bernanke did exactly what we thought he’d do yesterday: (1) Raised his inflation forecast; (1) Cut his GDP forecast and (3) Burned the Buck. As we look at today’s set up for the S&P 500, the range is 32 points or -2.04% downside to 1328 and 0.32% upside to 1360.

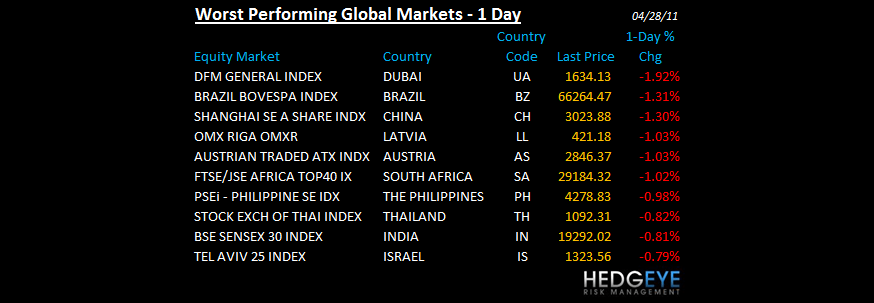

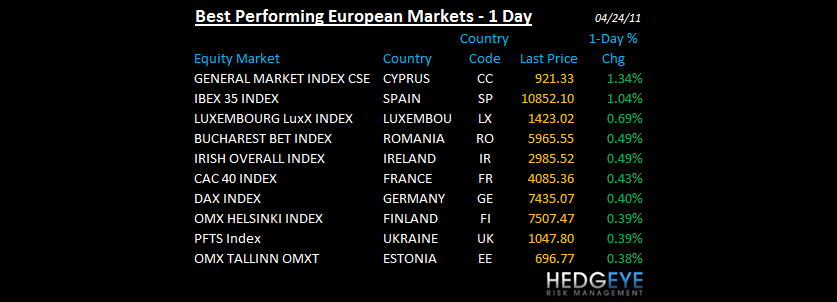

SECTOR AND GLOBAL PERFORMANCE

The Financials remain the only sector broken on both TRADE and TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 832 (-530)

- VOLUME: NYSE 960.95 (+5.67%)

- VIX: 15.35 -1.73% YTD PERFORMANCE: -13.52%

- SPX PUT/CALL RATIO: 1.21 from 1.15 (+5.28%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.25

- 3-MONTH T-BILL YIELD: 0.06% -0.01%

- 10-Year: 3.39 from 3.34

- YIELD CURVE: 2.72 from 2.74

MACRO DATA POINTS:

- 8:30 a.m.: GDP 1Q advance, est. 2.0% (annualized), prior 3.1%

- 8:30 a.m.: Initial jobless claims, est. 395k, prior 403k

- 8:30 a.m.: Fed’s Duke, Williams speak at Community Affairs Conference in Virginia

- 9:45 a.m.: Bloomberg Consumer Comfort, est. (-43.0), prior (-42.6)

- 10 a.m.: Pending home sales, est. 1.5% M/m, prior 2.1%

- 10 a.m.: Freddie Mac mortgage rates

- 10:30 a.m.: EIA Natural Gas Change

- 1 p.m.: U.S. to sell $29b 7-yr notes

WHAT TO WATCH:

- New Zealand’s central bank kept its benchmark interest rate at a record low and called the local currency’s rise “unwelcome.”

- Most emerging-market stocks fell on concern China will raise interest rates as early as next week.

- U.S. ‘Disappointed’ by India Rejection of U.S. Aircraft - Bloomberg

- Google May Overtake Apple in App Sales: All Things Digital

- Deutsche bank profit exceeds estimates as money management reaches record

- SAP reports 4.1% gain in first-quarter profit, missing analyst estimate

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Sugar Seen Capped by Record Thai Production, Curbing Nestle, Kraft Costs

- Gold Climbs to Record as Bernanke Maintains Stimulus, Dollar Extends Drop

- Copper Climbs for First Day in Three

- Aluminum Advances to 32-Month High

- Crude Oil Futures Retreat From 31-Month High

- Corn Futures Advance in Chicago as U.S. Midwest May Face ‘Severe Flooding’

- Sugar Falls as Thai Production May Cap Price Gains; Coffee, Cocoa Advance

- Rubber Futures Advance for First Day in Four as Fed to Maintain Stimulus

- Abu Dhabi Oil Surges to Three-Year High on Chinese Demand

- Copper May Drop Next Week as Stocks Gain, China Demand Slows, Survey Shows

CURRENCIES

EUROPEAN MARKETS

- German unemployment declines to 19-year low as export boom drives demand

- German unemployment -37K, est. -37k (prior -55k)

- German unemployment rate 7.1%, est. 7.0% (prior 7.1%)

- Italian business confidence , est. 103.5 (prior 103.8)

- European stocks climb as deutsche bank beats analysts’ earnings estimates

- AstraZeneca first-quarter profit beats analyst estimates after tax accord

- Spain’s local elections may expose wider deficits in risk for bond markets

- UK consumer confidence declines to lowest since depth of 2009 recession

- France Mar consumer spending (0.7%) m/m vs consensus +0.2%

ASIA PACIFIC MARKTES:

- Japan quake takes bigger-than-estimated economic toll; BOJ lowers forecast

- Japanese earnings push the Nikkei 225 to the highest level since the March 11 quake.

- Asian stocks were mixed

- Nomura profit falls 35% as investment banking fees, trading income decline

- Panasonic plans to cut 17,000 jobs on Sanyo acquisition, television losses

- China economic growth faces risks from property ‘shocks,’ world bank says; China declined for the 5th straight day.

- China telecom net income climbs 8.1% on increase in mobile-phone customers

- Grantham sees one-in-four chance of china stumbling over excess spending

- RBA faces rate pressure as CPI outweighs record currency

MIDDLE EAST

Howard Penney

Managing Director