Positions in Europe: Long British Pound (FXB)

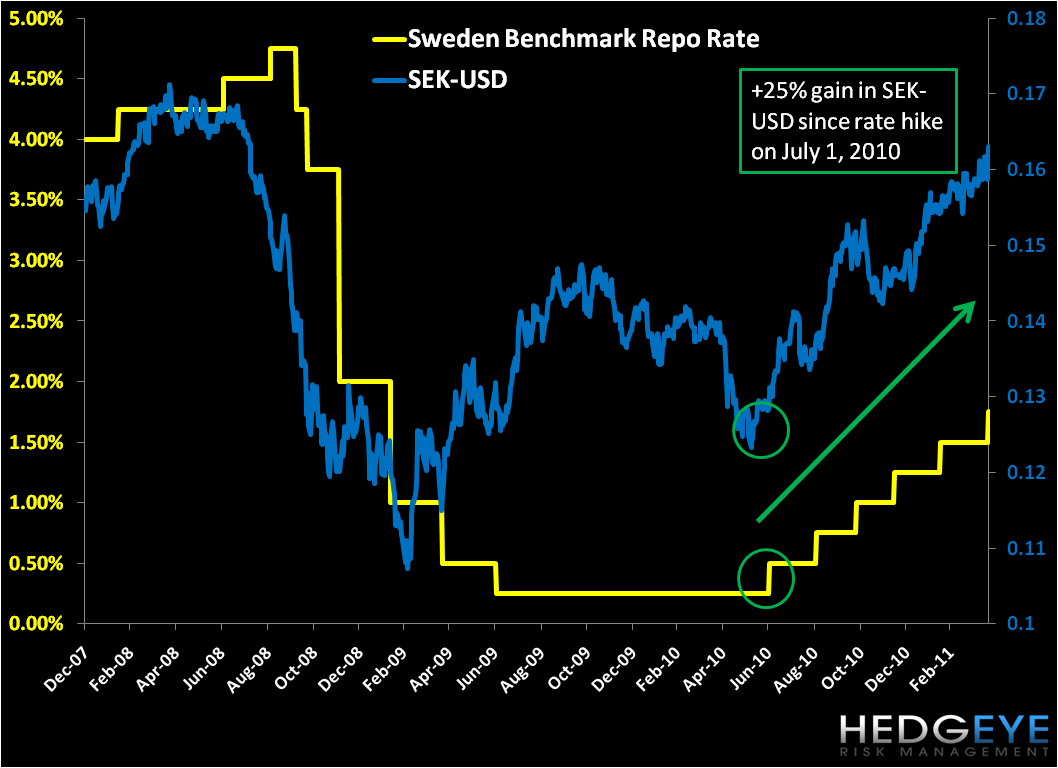

Sweden raised its benchmark repo rate 25bps today to 1.75%, the sixth time since July 2010. Today’s hike further confirms the proactive policy measures taken by Sweden’s central bank (Riksbank) and government to in particular control inflation and spur investment. (Please see our note on 4/15 titled “Sweden in the Sweet Spot” for our fundamental take on the country). The Swedish Krona reacted favorably to the hike, rallying against all major currencies this morning and to its strongest level against the USD since August ‘08! As the chart below presents, we’ve seen associated strength in the Krona vs the USD with every rate hike since July 2010, a trend we’d largely expect to continue throughout the year.

-We continue to express the severe turn we’ve seen in the capital markets of Europe’s peripheral countries while also noting a slight negative inflection in the data from Europe’s larger (and fiscally sober) countries like Germany, France, and the Netherlands.

Yields Ramp for PIIGS

Today both Spain and Portugal issued debt. Recent weeks have shown a strong reversal in the trend we saw in early 2011 of PIIGS issuing debt at lower yields than previous auctions, largely a response to the commitment from China and Japan to buy European debt.

Spain sold €3.4 billion of treasury bonds at auction today and the 10YR yield jumped to 5.472% versus 5.162% in March. Interestingly, Portugal issued €320 million of six-month bills today at nearly the same yield as Spain’s 10YR, or 5.529% versus 5.117% on April 6.

The clear take-away here is the risk premium imbedded in owning Portugal’s debt, which should continue to heighten as the size and structure of an EU/IMF-led bailout of Portugal remains at large, and given the election results in Finland that saw the euro skeptic/anti-bailout parties take voting share (for more see our post on 4/18 “European Risk Monitor: Peripheral Risk Pops as Finnish Elections Inflect”). As a calendar catalyst to monitor, the expectation is for a bailout of Portugal in mid-May, ahead of the June 5 election date set by the current interim government.

A familiar chart of 10YR bond yields of the PIIGS (below) continues to be telling of the debt refinancing headwinds these countries are bumping against. Greece’s 10YR hockey stick yield is now at 14.65%!

Data Drag

Yesterday Reuters issued its initial April reading of Manufacturing and Services PMI for Germany, France and the Eurozone. A notable call-out is the inflection in the German Services PMI number, registering 57.7 in April versus 60.1 in March. We called for the German Services number to mean revert in a post titled “Germany’s Marginal Turn” on 4/12, with the tag-line that the 60 line is a historically heavy resistance level. Eurozone Services also declined month-over-month, falling to 56.9 in April versus 57.2 in March.

We think the inflection in some of the high frequency data is a reflection of the marginal slowing in European growth expectations (especially in Germany) and that the slight dip or deceleration in consumer and business confidence reflects inflationary pressures and continued macro volatility, including sovereign debt contagion in Europe, instability in MENA and around Japan’s nuclear reactor(s) and rebuild, and US political indecision regarding its debt and weak USD policy.

Of note, tomorrow we get German business expectations from the IFO survey. The March figure turned down to 106.5 vs 107.9 in February. We think we’re likely to get a lower April figure.

Currency Positioning

We have a positive bias on both the EUR and GBP versus the USD due primarily to USD weakness. Due to the strong daily push/pull headline risk in Europe on the common currency, we view the EUR-USD as a trade to monitor on a daily basis. That said, we have a bullish immediate term outlook on the EUR-USD, with TRADE levels at $1.42 - $1.45, and think that Portugal, like Greece and Ireland, will be bailed out by the EU/IMF, which is increasingly being priced in.

The Bank of England continues to signal a hawkish stance on interest rates, however has not come off its 0.50% benchmark rate. The most recent BoE minutes show 6 votes against to 3 votes for a rate hike. Importantly, BoE head King recognizes inflationary threats to the economy, a position ignored by Ben Bernanke at the Fed, and in our opinion a major dislocating factor feeding USD weakness.

Besides our long position in the British Pound (FXB), we have no other current European country or currency position in the Hedgeye Virtual Portfolio. We covered our short position in Spain (EWP) on weakness on 4/18 for a TRADE, but remain bearish on the country’s outlook over the long-term TAIL.

Matthew Hedrick

Analyst