MCD will announce sales numbers for March, along with their earnings for 1Q, on Thursday morning before the market open.

There was no difference between the number of weekdays and weekend days in March 2011 versus March 2010. March 2011 had one less Monday, and one additional Thursday, compared to March 2010.

As a reminder, February’s U.S. result was in line with my neutral range of 2-3% and well below the Street’s expectation of 3.6%. I have been bearish on MCD since the latter stages of 2010, and published a Black Book detailing my thesis in January. For some time, I have been cognizant of the significance of MCD’s sales results in March. March represents a significant step-up in the difficulty of the compare for U.S. same-store sales; March 2010 comparable restaurant sales came in at 4.2% versus February 2010 at 0.6%. While MCD is a global company and it is crucial to monitor trends in all geographies, results from the U.S. division remain the primary driver of the share prices. As I stressed in the MCD Black Book, the U.S. market still represents about 45% of operating income. A comparable restaurant sales number below consensus in March would mark the sixth consecutive month of disappointing top-line results in the U.S.

Below I go through my take on what numbers will be received by investors as GOOD, BAD, and NEUTRAL, for MCD comps by region. For comparison purposes, I have adjusted for calendar and trading day impacts.

U.S. - Facing a difficult +4.2% compare (including a calendar shift which impacted results by -1.5% to +0.2%, varying by area of the world):

GOOD: A print above 1% would be perceived as a good result, implying that two-year average trends accelerated significantly in March on a sequential basis. Two-year average trends declined sequentially in December, and were roughly flat in January and February. I believe that a strong acceleration in two-year trends, as would be implied by a comparable sales print of +1% or higher, will be necessary to fully reassure investors of the strength of the core business in the U.S. It is important to note that, at this juncture last year, frappes and smoothies had been rolled out to 90% and 20% of the system, respectively.

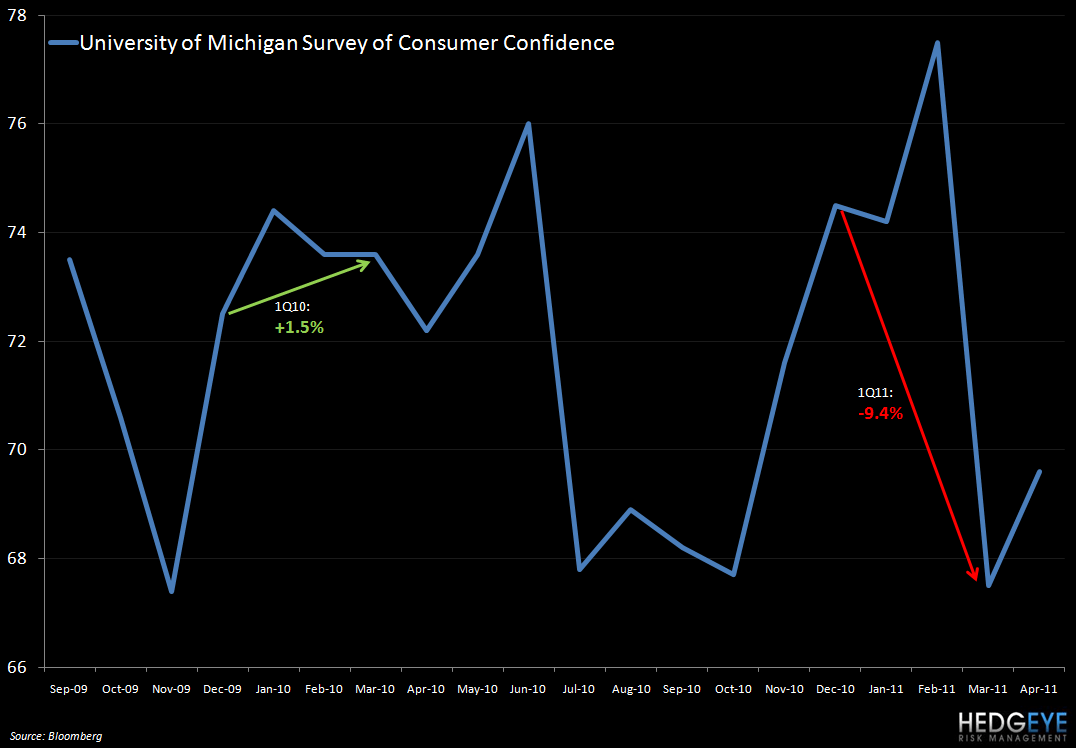

Last year consumer confidence was trending higher through 1Q10 and management cited consumer confidence “getting better over the last couple of months” as a key factor (along with more company-specific drivers) for top-line growth in the quarter. Looking at the University of Michigan Survey of Consumer Confidence chart, one can see that sentiment improved by 1.52% in 1Q10 but declined by 9.4% during the first quarter of 1Q11.

NEUTRAL: A print between 0% and 1% would be perceived as a neutral result. While the low end of this range would still imply sequential growth on a two-year basis, it would be a concern if anything less than a significant step-up were achieved following three disappointing months. I believe that a print in the neutral range is most likely, with a bias toward the lower end of the range. The street is currently forecasting 1.7% comp growth.

BAD: A comparable restaurant sales result less than 0% would clearly be a great disappointment to investors and would demand a dramatic revision of sell-side sentiment on this name (which would be long-overdue, in my opinion). I believe that a negative number is far more likely than most appreciate but, again, anticipate a comparable restaurant sales number in the neutral range detailed above. It is important to remember that a sequentially flat two-year average trend would imply a negative result in March.

Europe – Facing a difficult +5.9% compare (including a calendar shift which impacted results by -1.5% to +0.2%, varying by area of the world):

GOOD: A comparable restaurant sales number of 4% or higher for the Europe division would be received by investors as a good result. A print at this level would imply two-year average trends approximately 30 basis points (at most) below those seen in February, which was a particularly strong month for MCD’s European business. While the U.K. was mentioned as a strong market during the 1Q10 earnings call, along with Germany and Spain, it is important to note that Retail Sales in the U.K. during March showed the worst fall in sales for any month in at least 16 years.

NEUTRAL: A print between 3% and 4% would be received as neutral by investors as it would imply roughly flat-to-slightly-down two-year average trends which, I believe, would be in some ways expected given the fragility of the European consumer and the difficult comparison from a year ago. I believe a print toward the lower end of this range is most likely.

BAD: A print below 3% would imply two-year average trends significantly below those seen in February. Given the impact of austerity measures and the softness of retail sales across much of the Eurozone, not just in the U.K., there is a possibility that comparable restaurant sales come in below 3%. StreetAccount consensus is calling for a print of 3%.

APMEA – Facing a 2.8% compare (including a calendar shift which impacted results by -1.5% to +0.2%, varying by area of the world):

GOOD: A result of 3% or higher would be received as a positive result for APMEA. The earthquake/tsunami in Japan as well as, to a lesser extent, the knock-on effects of the flooding in Australia, is likely to depress results this month. MCD Japan reported results of -7.3% for March.

NEUTRAL: A result between 2% and 3% would be perceived as neutral by investors.

BAD: A result of less than 2% would be poorly received by investors. Not only would it imply a sharp drop in two-year average trends, but the number would also fall short of the street’s 2.0% estimate, which is allowing for the tragic events in Japan.

Howard Penney

Managing Director